RETAIL FIRST LOOK: GOODBYE HAMPTONS, HELLO REALITY

SEPTEMBER 8, 2009

TODAY’S CALL OUT

Here’s the post-Labor Day setup.

Now that the masses are back from the Hamptons and en route to the Goldman retail conference, let’s take a quick look at the setup. On the margin, it reinforces the point we’ve been making over the past 2 weeks that the pendulum is shifting to the downside, and if you want to own a name in this space, you’ve gotta be super confident in meaningful earnings beats or takeout potential. Here are some notables…

- Earnings revision factor flattened out for retail last week. It is still a healthy +25%, but marks the first time since June that it did not go up week on week.

- In looking at earnings trajectory for the 1462 companies in the S&P 1500 composite that have reported 2Q, the major call out is the rate of change in earnings expectations. Consumer Discretionary EPS growth expectations have gone from -16.7% to -3.4% for CY09 from March 1 through today. That delta is 2x the next closest group, which is Tech.

- Retail is trading at 15.5x those expectations. Not egregious, but absolutely not cheap by any means.

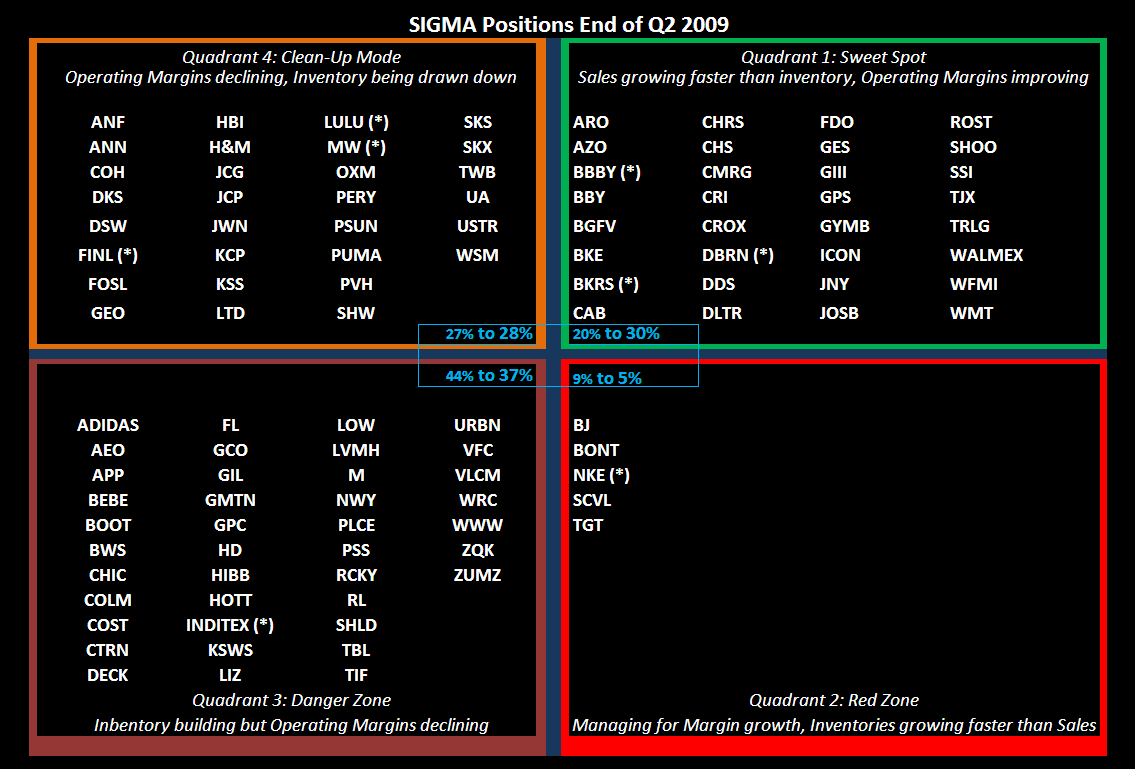

- As Zach elaborated on in Friday’s First Look, our SIGMA is headed in the right direction. Inventory/sales ratio looking good for the industry, and the margin setup for next two quarters is in check. But I struggle to find anyone that doesn’t know this and is positioned accordingly.

- Note that 30% of retail is in the “Sweet Spot” meaning that sales are outpacing inventories and margin delta is positive. We have to look back to early 2007 to find such a high percentage of companies in this zone.

LEVINE’S LOW DOWN

Some Notable Call Outs

- Despite having many years of growth ahead, the total ecommerce channel is now expected to post its first decline ever in 2009. According to interactive firm eMarketer, the ecommerce sector will decline by 3.1% this year (excluding online travel and ticket sales). However, the same study suggests growth will resume to 5.5% in 2010 and at a double digit rate in 2011.

- We don’t often think about Toys R Us much anymore given it’s now in private hands and is no longer the largest toy seller. However, the company has been on mini-acquisition spree lately, acquiring trademarks and IP that have long been icons in the industry. Toys R Us is now the owner of: FAO Schwartz, eToys.com, babyuniverse.com, ePregnancy.com, Toys.com and KB Toys. With all these brands now in-house, it will be interesting to see how the company markets each of them over the holiday period.

- As the eco-friendly trend in textiles and apparel continues to grow, the FTC is cracking down on environmental claims made by “green focused” manufacturers. The FTC recently charged four sellers of eco-apparel with deceptively labeling products. These manufacturers claimed their goods were made of bamboo, when in fact they were made of rayon. Given this recent crackdown, it is likely retailers will also need to be more diligent in substantiating the claims of their wholesalers before putting environmentally friendly products on their shelves.

MORNING NEWS

-Three creditors of Signature Apparel Group last week sought to force the Rocawear licensee into bankruptcy - The petitioning creditors, representing about $14.9 million in debt past due, filed an involuntary Chapter 7 petition in a Manhattan bankruptcy court on Friday. New York-based Signature manufactures apparel largely for the urban market. It holds licenses for Rocawear in the junior category as well as Artful Dodger, another urban brand. Signature also owns the Fetish trademark, which it relaunched with the rapper Eve for holiday 2008, after the line had separate unsuccessful stints with Marc Ecko Enterprises and Innovo Group. According to court documents, the petitioners are: Hitch & Trail Inc., New York, owed $3.6 million; Talful Ltd., Kwai Chung, New Territories, Hong Kong, $4.8 million, and Harvestway China Ltd., Kowloon, Hong Kong, $6.5 million. The company has 20 days to respond to the petition. <wwd.com/business-news>

-UK comp sales values fell 0.1% - UK retail sales values fell 0.1% on a like-for-like basis from August 2008, when sales had fallen, hit by very wet weather. On a total basis, sales rose 2.2% against a 1.4% gain in August 2008. This August, food sales continued to do better than non-food. Food sales growth edged up only slightly from July's low. Clothing and footwear weakened further. Homewares and furniture sales fell back below year-earlier levels after July's weather- and clearance-driven growth. Non-food non-store sales (internet, mail-order and phone sales) in August were 7.9% higher than a year ago, the weakest since May. <brc.org.uk>

-Home furnishing retailers reap rewards as home purchases start to ramp up - The news on the home front has been a steady increase in home sales for the past few months. Now an e-commerce systems provider reports that heightened interest in home investments may be reflected in increased sales at home furnishings sites. While admittedly unscientific because the data represent sales at only three sites—ArtPassions.com, BathtubStore.com and Foamiture.com—Avid Commerce LLC reports that sales at the three sites in June were 5.2% higher than sales in May; 33.9% higher in July from June; and 81.1% higher in August from July. The U.S. Department of Commerce reports that new home sales in May were up 4.9% from the prior month; in June, they were up 9.1% from May; and in July, 9.6% from June. <internetretailer.com>

-Goal is for India to turn into a global manufacturing hub of textile accessories by increasing the turnover - Indian Textile Accessories & Machinery Manufacturers' Association (ITAMMA) aims to turn India into a global manufacturing hub of textile accessories by increasing the turnover from this textile sub-segment from the current Rs 65 billion to Rs 200 billion by the end of the next decade. The Association is also in the process of transforming itself from a government liaison body to a new role of tying up for technology upgrade n and conducting market research for its members. It is also projecting an increase in exports from Rs 6.5 billion to Rs 10 billion in the next five years, since most of its exporting members have already started focusing on new regions and existing buyer countries like Bangladesh, Vietnam, Indonesia, Pakistan, Uzbekistan and Far-east countries. <fashionnetasia.com>

-Bangladesh asks for a stimulus package for the apparel industry - A member delegation from the Bangladesh Knitwear Manufacturers and Exporters Association (BKMEA) has met the Finance Minister AMA Muhith to ask for a stimulus package for the industry. While giving out the details of demands requested by the Finance Minister, the President of BKMEA demanded for a 5% stimulus incentive on FOB value of exports. He said, they had also requested that banks not to increase interest rates higher than 10%. Muhith assured the delegation that the garment sector problems and demands will come up for discussion at the second meeting of the taskforce on recession due on September 15-16. <fashionnetasia.com>

-Japan’s Renown Inc. to sell Aquascutum Group Limited to U.K.-based Broadwick Group Limited - Japan’s Renown Inc. said Tuesday it has struck a deal to sell Aquascutum Group Limited to U.K.-based Broadwick Group Limited, a company owned by retail tycoon Harold Tillman and Jaeger ceo Belinda Earl, for an undisclosed price. Renown also said it will sell the Aquascutum trademark for China and the rest of Asia to Hong Kong-based YGM Mart Limited, which had been the brand’s licensee in China. Renown said it will continue to manufacture and distribute the British brand’s products in Japan through a long-term master-licensing agreement with YGM. Renown is in the process of restructuring its business as it grapples with ongoing financial difficulties and weak macroeconomic conditions in its home market of Japan. Last year it put the British brand up for sale. <wwd.com/business-news>

-Department stores added jobs for the first time since May - Department stores added 5,800 jobs last month to employ 1.53 million, but specialty stores cut 9,500 to employ 1.4 million, the Labor Department said Friday. Despite the higher department store jobs figure, the overall landscape for retailers was not bright, economists said. <wwd.com/business-news>

-U.S. discount, grocery and restaurant chains are hiring a larger percentage of job applicants than seven months ago - In July, 2.99 of every 100 applications resulted in a hire, compared with 2.75 in January, a three-year low. The pace of hiring of cashiers, merchandise stockers and other frontline workers in July was less than half that of October 2006, Kronos said. U.S. unemployment rose to a 26-year high of 9.7 percent in August, according to the Labor Department. Retailers fired 10,000 people last month while all U.S. employers trimmed payrolls by 216,000 after slashing 276,000 jobs in July. <bloomberg.com>

-The Action Sports Retail Show will hit the San Diego Convention Center September 10th -12th - ASR will showcase the latest apparel, footwear, swimwear, accessories and hardgood products from over 700 surf, skate, swim, snow, moto, wake, lifestyle and streetwear brands. Retailers, buyers, brands and athletes will all get a chance to converge and find out about the latest trends in action sports equipment and apparel. The event takes place at the San Diego Convention Center this Thursday thru Saturday. <examiner.com>

-The skate business may be headed for slower times, as the youth market feels the sting of the down economy - The economic downturn and a sharp reduction in discretionary spending among teens has impacted the market. The rapid expansion in the skate arena over the past few years may be unsustainable and slowing is to be expected. August is the most important month of the year for skate. To see a slowdown this dramatic in the biggest month of the year does not bode well. According to NPD data, for the 12 months ending June 2009, sales of skate shoes declined 13.3% in terms of dollars spent, largely due to a lower average selling price of $31.95, down from $33.30. By contrast, the total athletic footwear market declined 3%, while the average unit price increased to $37.70, from $35.05. <wwd.com/footwear-news>

-Many retailers are upbeat that fall’s footwear arrival will give them a much-needed boost after a lackluster spring - With inventories at extremely low levels, a number of key department stores and independents were optimistic last week about early reads on the season and said several key boot styles were already registering strong sales. Larger retailers were also hopeful about their prospects for the coming months — and said shoppers were already starting to snap up fall styles. <wwd.com/footwear-news>

-An official at the Collegiate Licensing Co. predicted that retail sales of college fan merchandise could be down 7% this year - All the leagues have definitely seen declines this year.The North American college sports segment continues to be a major licensing player. <sportsonesource.com>

-Under Armour launches new ad campaign - Under Armour will be debuting its "Under Armour is Football" advertising campaign this coming weekend in spots that will include Founder and CEO Kevin Plank making a cameo appearance from his days playing youth football. <sportsonesource.com>

-New York Fashion week kicks off this Thursday with "Fashion's Night Out," a global event spearheaded by Vogue to stimulate store sales - Retailers in eight cities around the world, from Paris and Milan to New Delhi and Beijing, will stay open late to offer a special night of shopping jazzed up with celebrity and designer appearances, musical performances and special events. More than 800 stores in New York, from Payless to Louis Vuitton, are participating in the five-borough event, which is being produced through collaboration among the City of New York, its marketing arm NYC & Company, American Vogue and the Council of Fashion Designers of America. While the event is designed to boost sales, deep discounts won't be part of the night's offerings. To help promote the event, advertising is running on city media assets, including outdoor on bus shelters and kiosks and in New York City's 6,500 taxis. A celebrity-studded PSA created by Laird + Partners has been playing in cab monitors, as well as on TV, online and spread virally through social networks such as Facebook and Twitter. <brandweek.com>

-Walmart dwarfs Target in size, yet it loses out to its rival when it comes to consumer discussions online - Target consumers are much more likely to speak about their shopping experience, according to online buzz monitor Crimson Hexagon, while chatter about Walmart often veered into discussion of the social implications of the retailing giant when it comes to labor practices and local retailers. It examined online chatter on blogs, Twitter, social networks and message boards for a one-month period beginning in mid-July. Overall, Target enjoys mostly positive chatter. About 75% of conversations were positive, according to Crimson Hexagon. Walmart, on the other hand, is discussed in a negative light 61% of the time. One in five shopping conversations touched on low prices. <brandweek.com>

INSIDER TRANSACTION ACTIVITY:

SCVL: Timothy Baker, Exec. VP – Store Operations, sold 6,028shs (~$90k) upon exercising the right to purchase 6,028 shares roughly 10% of common holdings.

ZUMZ: Lynn Kilbourne, President & GMM, sold 9,074 ($127k) or roughly 15% of common holdings.