TODAY’S S&P 500 SET-UP – October 20, 2014

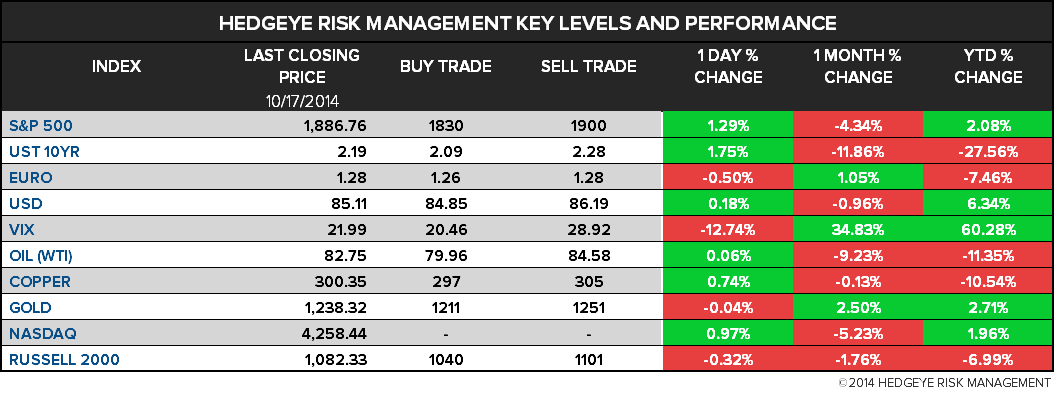

As we look at today's setup for the S&P 500, the range is 70 points or 3.01% downside to 1830 and 0.70% upside to 1900.

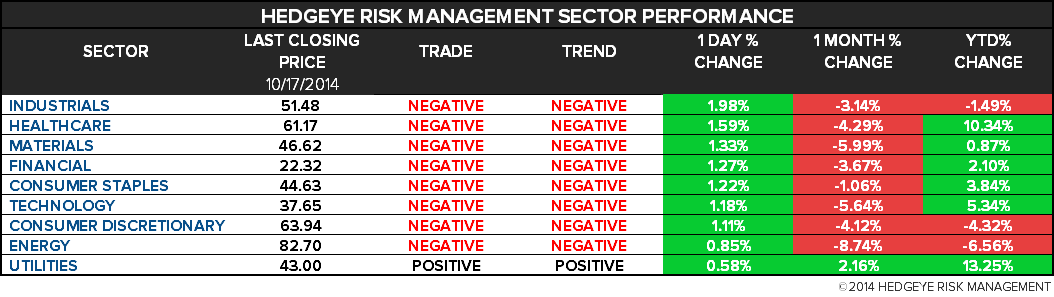

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.83 from 1.82

- VIX closed at 21.99 1 day percent change of -12.74%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Fed Governor Jerome Powell speaks on community banking in online forum

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $24b 3M bills, $30b 6M bills

GOVERNMENT:

- Senate, House out of session

- FEC filing deadline for candidates, some Pacs, parties for Sept

- 8am: NY Fed meeting on reforming culture, behavior in financial services; speakers include Sir David Walker at Barclays, UBS’s Axel Weber, JPMorgan’s Lee Raymond, Fed’s Daniel Tarullo, Morgan Stanley’s James Gorman

- 1pm: Financial Services Roundtable, FBI, Secret Service conf. on cybersecurity

- 2pm: FHFA Director Melvin Watt, HUD Secretary Julian Castro speak at Mortgage Bankers Assn conf.

- 4:30pm: Freddie CEO Donald Layton, Fannie CEO Timothy Mayopoulos speak

WHAT TO WATCH:

- IBM Agrees to Pay Globalfoundries $1.5 Billion to Take Chip Unit

- Investors Plan $2.2b Bid for Adidas’s Reebok, WSJ Reports

- Yahoo’s Mayer Faces Crucial Earnings Call Amid Investor Pressure

- CEO Mayer Said to Refresh Turnaround Plan; Seek M&A: WSJ

- Texas Ebola Cases Had Possible Contact With 300 People in U.S.

- Spain Ebola Patient May Be Free of Virus After Negative Test

- Cleco: Investor Group to Buy Cleco for $55.37/Shr in Cash

- Fed to End Bond Buys This Month as Planned, Rosengren Says: WSJ

- Obama May Seek an Iran Nuclear Deal Without Congress: NYT

- Tesoro Acquires QEP Pipeline Assets in $2.5b Deal

- McDonald’s Says Russia Inspecting More Than 200 Restaurants

- Boeing Seeks Revised Schedule for $51b U.S. Aerial Tanker

- Nutreco Agrees to Be Bought by SHV for About $3.4b

- Sprint Job Reductions Will Include 452 at Kansas Headquarters

- Marc Andreessen Resigns From EBay Board as PayPal Is Spun Off

- Banks’ Range of Libor Calculation Methods May Be Standardized

- Danone Hasn’t Yet Decided on Priorities for External Growth

AM EARNS:

- Gannett (GCI) 8:30am, $0.55

- Genuine Parts (GPC) 8:52am, $1.24

- Halliburton (HAL) 7am, $1.10 - Preview

- Hasbro (HAS) 6:30am, $1.45 - Preview

- IBM (IBM) 7am, $4.32

- Lennox Intl (LII) 8am, $1.41

- Peabody Energy (BTU) 8am, $(0.66) - Preview

- Valeant Pharma (VRX CN) 6am, $1.99 - Preview

- VF Corp (VFC) 7am, $1.10 - Preview

PM EARNS:

- Apple (AAPL) 4:30pm, $1.30 - Preview

- BancorpSouth (BXS) 6:43pm, $0.33

- Brookfield Canada (BOX-U CN) Aft-Mkt, C$0.41

- Cadence Design Systems (CDNS) 4:05pm, $0.24

- Celanese (CE) 5pm, $1.44

- Chipotle Mexican Grill (CMG) 4:02pm, $3.83

- CYS Investments (CYS) 4:05pm, $0.32

- East West Bancorp (EWBC) 5:16pm, $0.60

- Helix Energy Solutions (HLX) 5:30pm, $0.50

- Hexcel (HXL) 4:05pm, $0.54

- IDEX (IEX) 4:05pm, $0.84

- Illumina (ILMN) 4:05pm, $0.56

- Packaging Corp of America (PKG) 5pm, $1.26

- Rambus (RMBS) 4:05pm, $0.13

- Rent-A-Center (RCII) 4:25pm, $0.47

- Steel Dynamics (STLD) 6pm, $0.44

- Texas Instruments (TXN) 4:30pm, $0.71

- Zions Bancorp (ZION) 4:10pm, $0.44

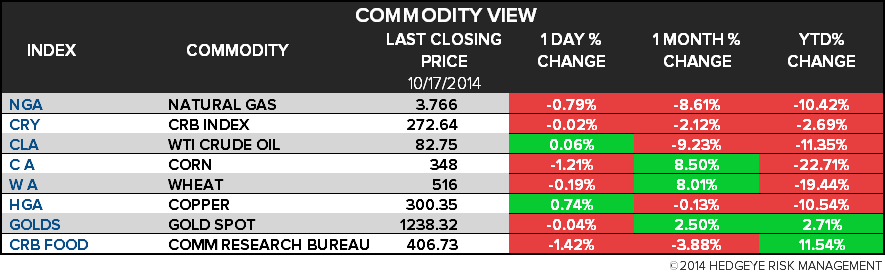

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Advances in New York on Dollar Weakness to Falling Stocks

- Brent Crude Oil Trades Near Level Seen as OPEC Test; WTI Steady

- Gold Bulls Lured Back for First Time in Two Months: Commodities

- Copper Declines With Other Industrial Metals on China’s Slowdown

- Hedge Funds Cut Bullish Bets on Crude as Prices Tumble: Energy

- Sumitomo’s $1.55 Billion Loss Shows Shale Isn’t Booming for All

- Citrine’s Hommert Sees ‘Good Upside’ for Nickel Next Year

- Sugar Millers See Thai Cane Output Dropping Below 100 Mln Tons

- Rubber Reaches 1-Month High as Malaysia Sees 10% Drop in Output

- Fire Shuts U.K.’s Didcot B Power Station; No Risk Seen to Supply

- Iron Ore Risks Extending Collapse as Supply Jumps, Moody’s Says

- Modi Uses Oil Slump to Ease Curbs Deterring Exxon, Chevron

- Deeper Oil Slump Seen as ‘Disaster’ Risk for Australian LNG

- Goldman Sees Copper Underperforming Most Base Metals in 2015

CURRENCIES

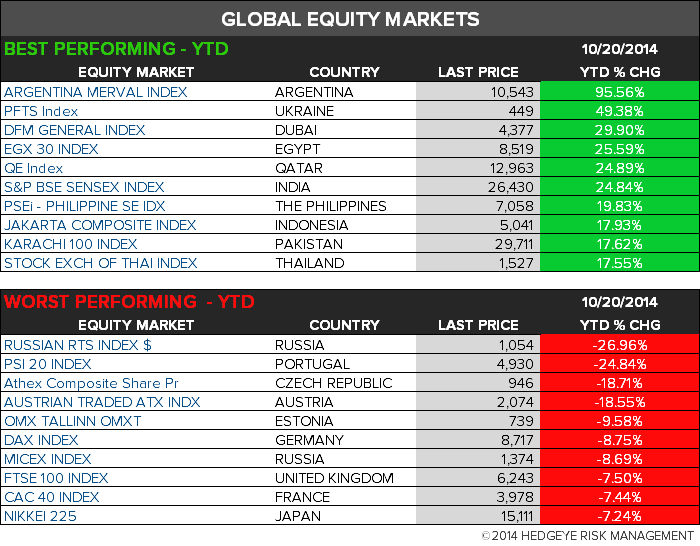

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team