Below are Hedgeye analysts’ latest updates on our five current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*Please note that we removed Legg Mason (LM) and Owens Corning (OC) this week from our Investing Ideas list.

We also feature two institutional research notes which offer valuable insight into the markets and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

Beware the Bounce

Be wary of Friday's bounce in the stock market.

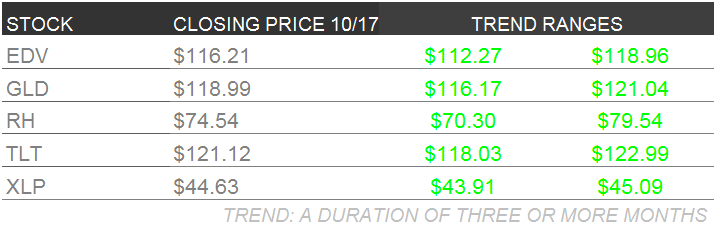

IDEAS UPDATES

TLT | EDV | XLP

THE DATA KEEPS ON COMING OUR WAY

The week ending October 17th, 2014 was another supportive week for the slow-growth, yield-chasing trade we continue to recommend.

Domestically speaking, the data continues to come our way as we continue to anticipate a reactionary dovish policy response out of the Federal Reserve – particularly amid collapsing inflation expectations and a breakdown in commodity prices.

- Food, energy and gas led the -0.1% MoM decline in PPI-FD in September with both core and headline decelerating -20bps sequentially to +1.6% YoY.

- In the face of aggregate income growth and strong initial claims, Retail Sales unexpectedly dropped MoM for the first time since JAN, showcasing broad deceleration across 11 of 13 industries.

- U.S. housing data slowed as we watched Homebuilder Confidence, measured by NAHB’s HMI, decline to 55 in October, a drop of -5 points vs. the 9 year high reading of 59 recorded in SEPT. To be more clear, there has been a MoM decline across all three sub-indices in both current sales and current traffic, along with regional homebuilder confidence declining across all regions for the time since FEB.

Internationally speaking, in our 10/15 note titled, “Macro Medley: 0 for (Quad#4)” we highlighted how our global macro monitor is currently showcasing a near-universal negative trend of estimate revisions for both growth and inflation over the last quarter across both developed and EM markets.

With #EuropeSlowing, Japan slowing and China slowing simultaneously, we continue to expect slowing global growth to weigh on both business and investor confidence and reflexively perpetuate a negative feedback look in the domestic economy over the intermediate term.

In brief, you want to be long/overweight the asset classes and style factors that have weathered recent financial market volatility (i.e. Treasuries, munis, cash, and large-cap/high-yield/liquid equities), while remaining short/underweight its inverse (high beta, small cap illiquidity and early cycle leverage). That means remaining long of TLT, EDV, and XLP.

GLD

We added gold (GLD) to investing ideas on the long-side back in May when the outlook for U.S. economic growth was in what we call a QUAD#3 set-up in our GROWTH, INLFATION, POLICY model. The extensive swath of economic data input was collectively signaling that growth was slowing with inflation accelerating. Commodities (and any commodity-linked asset classes), treasuries, and fixed assets inflate in this set-up.

With the turn now into QUAD#4, growth is still slowing and the slope of inflation is now DECELERATING. A QUAD#4 set-up does not (and will not) bode well for commodities, but we’re safe to say gold markets are driven by additional factors given its currency-like negative correlation to the dollar and U.S. treasury bonds.

With growth slowing in Europe as well, we have to keep an eye on further devaluation from ECB President Mario Draghi, but with the current set-up in the domestic economy, we would like to front-run the next Federal Reserve Policy move, and stick with our gold position.

- GOLD vs. USD: Our GIP model is still front-running a full-year 2014 GDP print below consensus and fed estimates, and we expect downwardly revised growth estimates echoed with a more dovish tone from the Fed which will be BEARISH for the USD, and thus BULLISH for GOLD.

To exemplify the importance of front-running the Federal Reserve policy chatter, observe to the follow-through market moves after Janet Yellen’s commentary last Wednesday on the minutes release from the September 16-17th meeting:

“FURTHER GAINS IN THE DOLLAR COULD HURT EXPORTS AND DAMP INFLATION.”

a.k.a “we are not hawkish, and we’re not reverting on engrained beliefs on how monetary policy should intervene in the marketplace.”

Since her commentary, the market moves, and thus our reason for staying long of gold are self-explanatory:

- GLD: +1.18%

- UST 10-year yield: -5.0% to 2.19%

- USD Index: -0.39%

- CRB Index: -1.4% (divergence with Gold)

RH

Earlier this week, we were reviewing a true comparable for Restoration Hardware. It's so hard to find a comp for RH. People look at West Elm, or Williams-Sonoma, but they're really different customers looking for a different aesthetic at a different price point.

But take a look at Arhaus (pronounced Our-House). It is by far and away the closest we've ever come to seeing the “Resto look” in a place that's not Resto.

Granted, the prices are higher, the quality is lower, and the design is a 7 to RH's 10. It also lacks the size and scale to compete with RH's prices. But this is one to watch.

* * * * * * * * * *

Click on each title below to unlock the content.

Oil Has Further Downside Before The Bottom

The expectation for a supply/demand floor is not a catalyst for volatility-induced real-time market moves.

Taxable Bond Bleeding Continues - BlackRock Puts Up Soft Equity Results

Dislocation at PIMCO continued last week with BlackRock signaling weak retail and institutional equity trends in yesterday's earnings.