RETAIL FIRST LOOK: THE SIGMA: WHERE DO WE GO NOW

AUGUST 4, 2009

TODAY’S CALL OUT

Note: Zach Brown takes the conch from McGough this fine morning.

I don’t want to dwell on Axl Rose this morning given the severe lack of relevance to retail (other than when he popped Tommy Hilfiger at a NY club in May ’06). But his quote from Sweet Child ‘O Mine rings very true today. “Where do we go now?”. The only way to answer that is with a process.

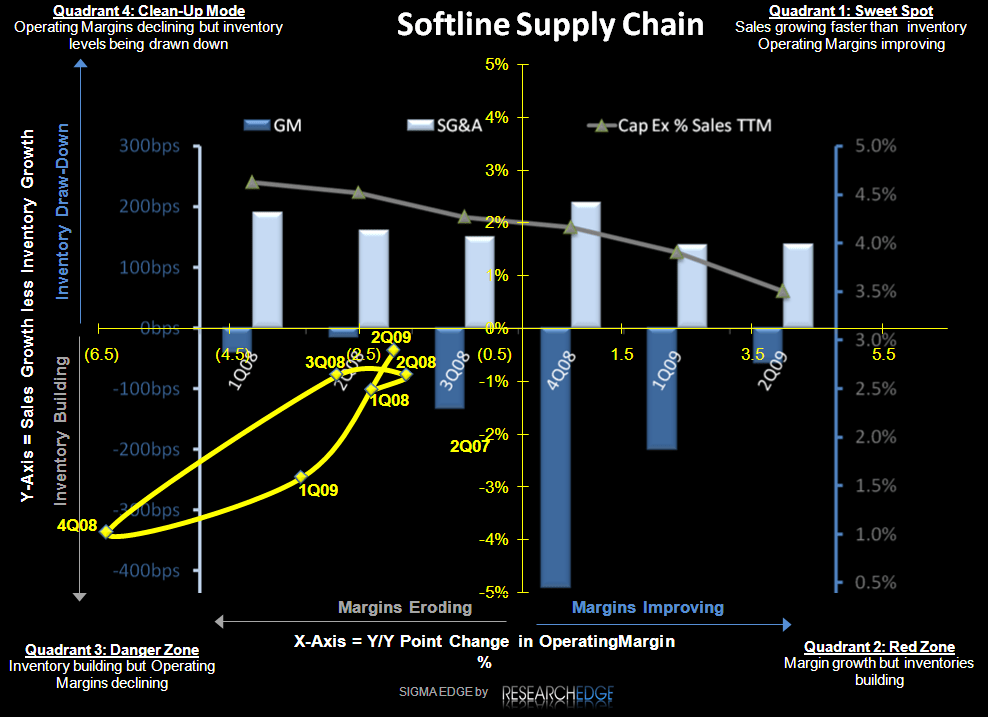

One of the cornerstones of our analytical process is our SIGMA (Sales Inventory Gross Margin Analysis). There’s no shortage of people we’ve confused by the imposing visual in the chart below. But once you take the time to understand it, you see that it is not only a strong financial analytics tool, but also a way to monitor the behavioral changes in how a management team (or group of them) trades one line of the P&L or balance sheet against another in the face of changes in the Macro environment.

Here is a quick overview of how to read the chart: the vertical axis illustrates the difference between sales growth and inventory growth, while the horizontal axis represents the year to year change in the operating margin. We then plot the past 8 quarters of data to track the trend in where a company has been. The punchline is that companies should always strive to be headed to the upper right hand quadrant (sales outpace inventories and margins up). The background to the SIGMA chart has the year to year changes in the gross margin and the SG&A margin along with a line representing capex as a percent of sales on a trailing twelve month trend. This allows us to track what kind of margin and cash flow compares we’re looking at on a quarter-to-quarter basis.

Do you want to know why Retail has outperformed the S&P so meaningfully since the March 9th lows? Check out the swing in the SIGMA trajectory from 4Q08 to 2Q09.

We have a SIGMA book with 107 companies, which helps our team (and our exclusive Retail vertical) focus on which companies are interesting and at what time do these companies of interest become actionable. Let us know if you’re interested. I’ll be around all day ().

The second image below has the location of where each of the 107 companies ended up on the SIGMA chart after reporting Q2 results (* except for those that will report in the next 2 weeks). The sequential improvement from Q1 to Q2 is impressive: at the end of Q4 63% of the companies were in the danger zone, Q1 had 44%, and Q2 had 37%.

The big question is, as the Guns N’ Roses singer Axl Rose so eloquently asks, ”Where do we go now?” I think the answer is up. Looking at the background in the SIGMA, the gross margin and SG&A margin compares look very easy in the back half of the year. Our call for some time has been that we will see growth again in the back half of the year, especially in the 4th quarter. I think we will see the yellow SIGMA line make two meaningful steps upwards to the right and finish 2009 in the sweet spot. Brian has commented recently how the market is discounting much of this, with a 39% improvement in the consensus NTM EPS growth rate over just the last 3 months. As such, we like to stick with the big earnings outliers, M&A targets, or names that will do well in a stagflationary environment (cap, liquidity, solid balance sheet, and growth).

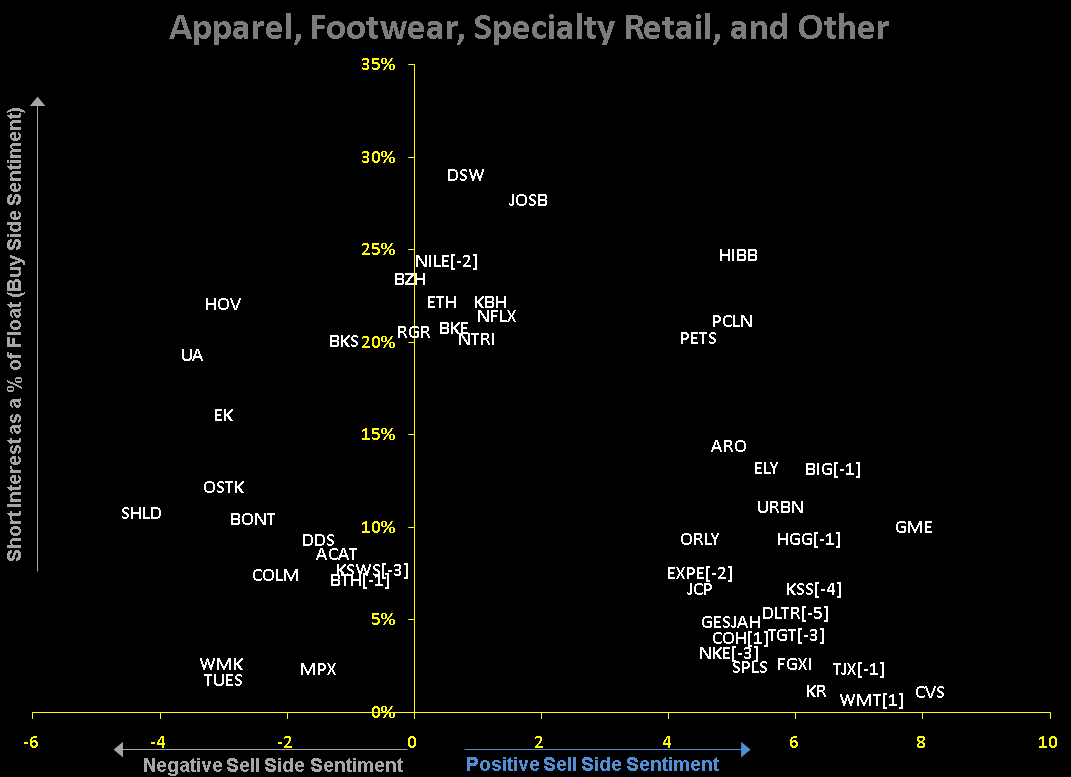

Another factor that is so important to us in this market is sentiment. Chart 3 shows the sell side sentiment on the x-axis, the buy side’s on the y-axis, and the insider transaction movement next to each company’s ticker. The chart captures the outliers with those hated in the upper left and those loved in the bottom right.

- There are some meaningful outliers where the consensus bears better be right on earnings, or we’re set to see squeezy the shark show his gnarly-looking teeth and bite the shorts. Good examples there are UA, OSTK, SHLD, DSW and PSS.

- On the flip side we’ve got KR, CVS, NKE, COH, TJX and SPLS. Yes, some quality in there. But with short interest so uniformly low, and sell-side sentiment so positive, we need some big beats to keep these names afloat.

So keep your head in the game, and your eyes on the prize as we make some progress in 2H towards the sweet spot of the SIGMA. And call us if you want detail on specific companies.

LEVINE’S LOW DOWN

Some Notable Call Outs

- According to several news sources, LIZ has hired turnaround firm Alvarez & Marsal to assist in collections and inventories. While the firm is known for prepping companies for bankruptcy, a managing director at the firm was quoted saying that they were helping LIZ to improve working capital not to prepare for a bankruptcy filing. There are those who could interpret this as a sign of desperation, we absolutely do not believe this to be the case. This “all hands on deck” approach and input from a leading turnaround firm should help accelerate LIZ’s key cost initiatives and could even result in a few introductions to potential buyers should the company decide to sell brands.

- On the company’s quarterly conference call, ZQK highlighted recent softening in their footwear business relative to apparel. As it turns out, major footwear retailers are delaying the shipment of product that is typically taken in Q4 in an effort to keep inventory levels clean. One look at the family footwear SIGMA (see yesterday’s First Look Call Out) and it is evident which retailer might be concerned about inventory levels. Interestingly, BWS mentioned DC as one of their key growth drivers on their call last week.

- As noted by several retailers this week, women's dresses continue to be one of the few bright spots in apparel. It is also one of only two categories in which G-III is investing in growth (sportswear is the other) given the sizeable opportunity the company sees over the long term. G-III’s current portfolio includes labels such as Calvin Klein, Jessica Howard, and the new Jessica Simpson line that is slated for a holiday release.

MORNING NEWS

-Vietnam footwear exports expected to decline - Vietnam is estimated to see its footwear exports reaching $5.3 billion in 2010 despite the current drop due to the global economic downturn, according to the General Statistics Office. The sector is down 11% in first eight months of this year. In August alone, footwear exports are estimated to be down 3.31% sequentially to July and 10.71% compared to the same period last year. The Leather and Footwear Association (Lefaso) forecast that this year's export turnover of leather and footwear products would be 10% lower than the full-year target of $5.1 billion. Meanwhile, the EU's term-end check on the anti-dumping suit against Vietnam's leather cap shoes and the European Commission's decision to exclude Vietnamese leather shoe exports to the EU from the list of products eligible for the Generalized System of Preferences (GSP) from January 2009 have undermined the competitiveness of Vietnamese footwear products. <fashionnetasia.com>

-Pakistan's announced a ‘Mark-up Rate Support’ order for textile manufactures - Pakistan's Ministry of Textiles has announced a ‘Mark-up Rate Support’ order for textile manufactures that will be admissible to the extent of 2.5% or the difference in mark- up rate between floating rate loan and Long Term Financing Facility rate, whichever is lower. This order will be effective from September 1, 2009 and Mark-up support can be taken on outstanding running balances of principal amount of floating rate long terms loans availed by the textiles industry and disbursed up to August 31, 2009, to finance import and purchase of textile machinery. <fashionnetasia.com>

-Back-to-school failed to get consumers back into stores in August - Retailers reporting comparable-store sales on Thursday in many cases registered smaller declines last month than in July, and a few more were able to put up gains as state tax holidays moved to the more recent month. With Labor Day, and the opening of many schools, later this year than last and consumers shopping closer to need than ever, there was also the expectation that some b-t-s business would move into September. Even without the calendar shifts, this month is expected to pose a lesser challenge for stores as their results will be weighed against the full-blown arrival of the credit crisis a year ago. Weaker comparisons also are expected to buoy year-on-year results as retailers move, somewhat tentatively, into the third quarter and on to the fourth. While higher-priced stores again took a drubbing, August’s winners included off-price retailers and others offering hefty value propositions to attract consumers. <wwd.com/business-news>

-Sheepskin footwear company acquires slipper brand - Lamo Sheepskin Inc., of Chino, Calif., known for its sheepskin footwear has acquired slipper brand Oomphies from Spain-based Menorca 1820 Inc. Oomphies is best known for its classic leather mules in pastel and metallic colors. While the brand has had limited distribution more recently, it has maintained a following among more mature customers through its presence with online retailers. According to Lamo CEO Joseph Li, because there remains a loyal customer base, Lamo will continue to produce both vintage styles such as the Granda mule and Laurie open-toe wedge while introducing looks to appeal to a younger consumer base. While the shoes have been produced in Spain, Lamo will manufacture the new line in Asia with its first collection scheduled to hit stores later this month. Set to retail at $50 to $60, distribution will be focused on department and specialty stores, independents and e-tailers. <wwd.com/footwear-news>

-Toys "R" Us acquires KB Toys - Toys "R" Us continues to reinforce its status as "The World's Greatest Kids' Brand" with the acquisition of the KB Toys brand which includes its URL, KBToys.com, its trademarks and other intellectual property rights. Over the past few months, Toys "R" Us has secured its place as a dominant force in the toy world, most notably through the acquisitions of FAO Schwarz and eToys.com. While too early to tell what role KB Toys will play in its growing portfolio of brands over the long term, it will provide the retailer with the buying power and distribution channel diversity it needs as it heads into the fourth quarter. At present, visitors to KBToys.com will be invited to shop Toys.com, where they will find exclusive savings and daily deals offered by the chain's other e-commerce sites. <brandweek.com>

-Burberry May Speed U.S. Growth Amid Deals on NYC, Indiana Space, CFO Says - Burberry Group Plc, Britain’s largest luxury-goods company, may accelerate plans to open U.S. stores as premium shop space becomes available at cheaper prices, Chief Financial Officer Stacey Cartwright said. <bloomberg.com>

-LVMH-Richemont Merger Would Be `Master Stroke,' Bernstein Analyst Says - A merger between LVMH Moet Hennessy Louis Vuitton SA and Cie. Financiere Richemont SA, the two biggest luxury-goods makers, would be a “strategic master stroke,” according to Sanford C. Bernstein analyst Luca Solca. <bloomberg.com>

-Bulgari is restructuring its U.S. executive team - Veronica McMahon Trenk has been appointed managing director of Bulgari in the U.S. Trenk was formerly managing director of the Roman jewelry house’s fragrance and skin care division in the U.S. She takes on the added responsibilities of François Kress, former managing director of Bulgari’s jewelry, watch and accessories division, who exited the firm nearly a month ago. Last month, WWD reported rumblings in Bulgari’s U.S. business with the closing of boutiques in three key markets: Palm Beach, Fla.; Aspen, Colo., and New York’s Madison Avenue. The jeweler revealed plans to open stores in San Francisco, Las Vegas and Dallas this year. Bulgari has 15 company-owned boutiques in the U.S., including stores in Atlanta, Honolulu and a 13,590-square-foot flagship on Fifth Avenue in New York. <wwd.com/business-news>

-Everywhere you turn these days, Puma is there - The athletic brand landed valuable airtime (again) last month, when its sponsored running star Usain Bolt raced across the track in Berlin and into thousands of news headlines. Then, Puma deepened its commitment to the motor sports market by signing a deal with Microsoft for prime branding placement in the upcoming “Forza Motorsport 3” racing game, set for release on Oct. 27. In addition to a spot in the game, Puma will also host Forza preview nights at its concept stores, release a Forza limited-edition shoe and post exclusive content about the game on Pumamotorsport.com. And further exposure will come through its sponsored driver, Natacha Gachnang, who was chosen by Xbox to be the face of Forza in its pan-European PR tour. Puma, based in Herzogenaurach, Germany, already outfits Gachnang in her FIA Formula Two races and will now provide apparel and accessories to the driver — and all Microsoft staffers — during trade events and conferences promoting the video game. <wwd.com/footwear-news>

-J.C. Penney joins a small group of retailers blazing the mobile apps trail - J.C. Penney has become No. 30 on a list of retailers that have created a downloadable mobile application for smartphones. It has launched JCPenney Weekly Deals, a mobile app for Apple’s iPhone and iPod Touch. <internetretailer.com>

-Lee Jeans unveils a retooled e-commerce site - Lee Jeans has taken the wraps off a redesigned site that features custom fitting tools and streamlined navigation. The newly retooled web site includes a revamped Fit Finder, which allows shoppers to find a pair of jeans that fit as if they were custom. <internetretailer.com>

-Fragrance line overshot projections by 25% - In its first week on counter, Tom Ford Grey Vetiver overshot its sales projections by 25 percent, according to industry sources. The fragrance, the designer’s third specifically concocted for men, bowed on Aug. 27 in Bloomingdale’s. It will roll out to specialty stores, including Saks Fifth Avenue, Neiman Marcus and Nordstrom later this month, and internationally starting in November. “The fragrance has started off quite well, and we’re confident it will be one of our top launches this fall,” said a spokeswoman for Bloomingdale’s. According to industry sources, Grey Vetiver will outstrip combined sales of Tom Ford for Men and Tom Ford Extreme and generate first-year global retail sales of $15 million to $25 million. <wwd.com/menswear-news>

-Foot Locker is ready for its online TV close-up - The New York-based retailer will launch an ad-supported Internet television channel, created in partnership with Gen2Media Corp, on its Website this fall. FootLockerOnlineTV will showcase custom video and digital advertising targeted to the company’s specific demographic. Bob Stephan, director of partner marketing at Footlocker.com, said in a statement, “We expect that the diverse and flexible ad serving opportunities ... will be an exciting opportunity for potential advertisers who my be interested in messaging our large and loyal following of athletic footwear and apparel enthusiasts.” <wwd.com/footwear-news>

-Style.com today is launching SHOP THE LOOKS - Just in time for New York Fashion Week, Style.com today is launching SHOP THE LOOKS, a custom e-commerce initiative that taps into the audience's existing passion for the latest runway trends. Users can now shop from more than 30 trends or "looks," which have been curated in collaboration with the editors of Style.com. SHOP THE LOOKS draws on the power and scale of the fashion shows on Style.com, 1 billion page views annually, as a purchase funnel for what's in stores now. Each runway slide will be tagged to correspond with one of the trends available in the SHOP THE LOOKS section, such as metallic, boho, or red carpet. In those sections, users can choose among dozens of currently available items that fit each trend. This represents the first time the Style.com user can use photos from the runway as inspiration for what to buy in stores now. Once in the SHOP THE LOOKS section users can also browse by seven main categories: clothing, bags, shoes, jewelry, beauty, accessories and sale. <prnewswire.com>