TODAY’S S&P 500 SET-UP – October 15, 2014

As we look at today's setup for the S&P 500, the range is 68 points or 0.94% downside to 1860 and 2.68% upside to 1928.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.82 from 1.83

- VIX closed at 22.79 1 day percent change of -7.51%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Oct. 10 (prior 3.8%)

- 8:30am: Empire Manufacturing, Oct., est. 20.25 (prior 27.54)

- 8:30am: Retail Sales Advance m/m, Sept., est. -0.1% (pr 0.6%)

- 8:30am: PPI Final Demand m/m, Sept., est. 0.1% (prior 0.0%)

- 10am: Business Inventories, Aug., est. 0.4% (prior 0.4%)

- 10:30am: DOE Energy Inventories

- 11am: Treasury Budget Statement, Sept., est. +$90b (pr +$75.1b)

- 11:30am: U.S. to sell $33b 4W bills, $25b 1Y bills

- 2pm: Federal Reserve releases Beige Book

- 2pm: ECB’s Draghi speaks in Frankfurt

GOVERNMENT:

- Senate, House out of session

- Sec. of State Kerry travels to Vienna for meeting with EU High Rep. Catherine Ashton, Iranian Foreign Minister Javad Zarif on nuclear negotiations

- 8:30am: PepsiCo CEO Indra Nooyi announces nutrition project hosted by Inter-American Development Bank

- 10am: Supreme Court hears arguments in patent case over generic competition to Teva’s multiple-sclerosis drug Copaxone

- U.S. ELECTION WRAP: Colo. Races; HRC on Trail; Money Reports Due

WHAT TO WATCH:

- AbbVie Weighing Shire Breakup Sends Inversion Target Shares Down

- Toyota Recalls 1.75m Autos to Fix Brakes, Fuel Leaks

- Qualcomm Agrees to Buy U.K. Chipmaker CSR for $2.5b

- Carnival to Help Build China’s First Cruise Ship as Demand Rises

- Second Health-Care Worker Tests Positive for Ebola in Texas

- Lenovo ‘Confident’ of Closing Motorola Mobility Deal This Year

- Obama Pushes Allies as Doubts Grow on Islamic State Strategy

- U.K. Unemployment Falls More Than Forecast as Wages Improve

- ASML Forecasts Quarterly Sales Beating Estimates on Memory Chips

- BofA Said Hired by Buyout Firms to Sell Turkey Memorial Stake

- Broker Lobby Group Sees Conflicts in Nasdaq SIP Upgrade Process

- Trump Casino’s Fate, Union Fight to Be Decided by End of Week

AM EARNS:

- Bank of America (BAC) 7am, $0.32 - Preview

- BlackRock (BLK) 6:30am, $4.66

- Charles Schwab (SCHW) 8:45am, $0.24

- Commerce Bancshares (CBSH) 7am, $0.71

- IGate (IGTE) 6:09am, $0.52

- KeyCorp (KEY) 6:30am, $0.26

- MGIC Investment (MTG) 7am, $0.11 - Preview

- PNC Financial (PNC) 6:30am, $1.70

- St Jude Medical (STJ) 7:30am, $0.96 - Preview

PM EARNS:

- American Express (AXP) 4:05pm, $1.37

- Boston Private Finl (BPFH) 4:05pm, $0.21

- eBay (EBAY) 4:15pm, $0.67 - Preview

- El Paso Pipeline (EPB) 4:07pm, $0.39

- Kinder Morgan (KMI) 4:05pm, $0.32

- Kinder Morgan Mgmt (KMR) Aft-Mkt, $0.56

- Las Vegas Sands (LVS) 4:01pm, $0.82

- Netflix (NFLX) 4:05pm, $0.91 - Preview

- Platinum Underwriters (PTP) 4pm, $1.32

- RLI (RLI) 4pm, $0.59

- Umpqua (UMPQ) 4:05pm, $0.29

- United Rentals (URI) 4:15pm, $2.08

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Extends Biggest Plunge Since ’11 on Glut; WTI Nears $80

- OPEC Finding U.S. Shale Harder to Crack as Rout Deepens: Energy

- Brent Slump Seen Stalling Near $80 as Bear-Market Oil Oversold

- Gold Imports by India Seen Rising More Than Fourfold Last Month

- Bugs Join Robots to Overcome Global Copper Shortage: Commodities

- Bloomberg Commodities Index Falls to Lowest Since July 2009

- Palm Imports by India Surge for Third Month on Tax-Free Sales

- Australia, Brazil Seen Taking 90% of Worldwide Iron Ore Trade

- Copper Falls From Three-Week High on Chinese Inflation Figures

- Palm Tumbles to Three-Week Low as Crude Oil Slump Reduces Demand

- Gold Drops a Second Day on Dollar to Lower Demand After Advance

- Corn Drops From Five-Week High as Drier Weather May Help Harvest

- Palm Declines to Two-Week Low as Crude Oil Slump Reduces Demand

- Rio Says Don’t Panic on Iron Ore And Won’t Halt Returns

- Rubber Drops From Two-Week High as China Data Signal Weak Demand

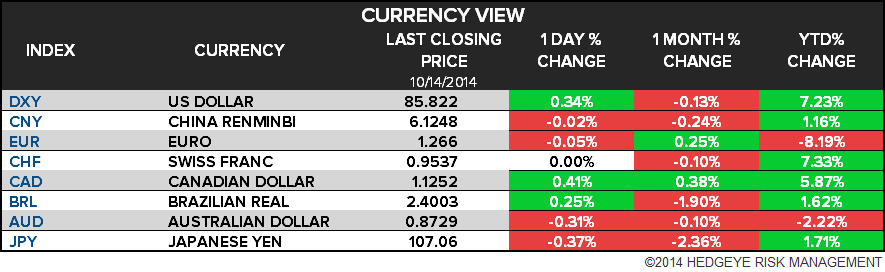

CURRENCIES

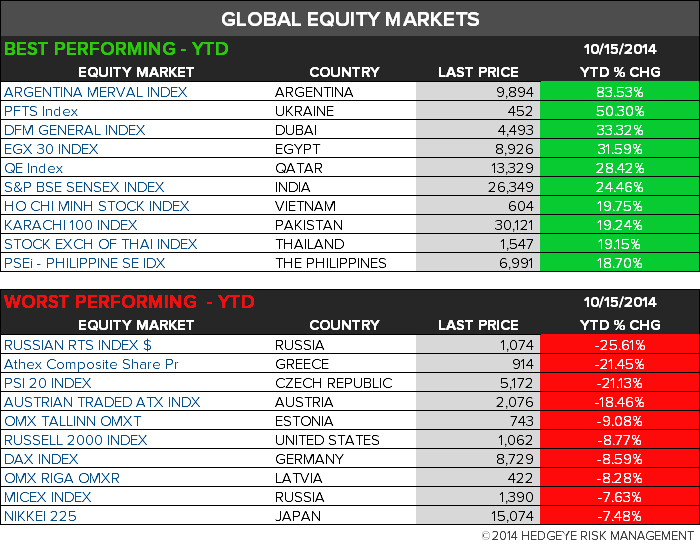

GLOBAL PERFORMANCE

EUROPEAN MARKETS

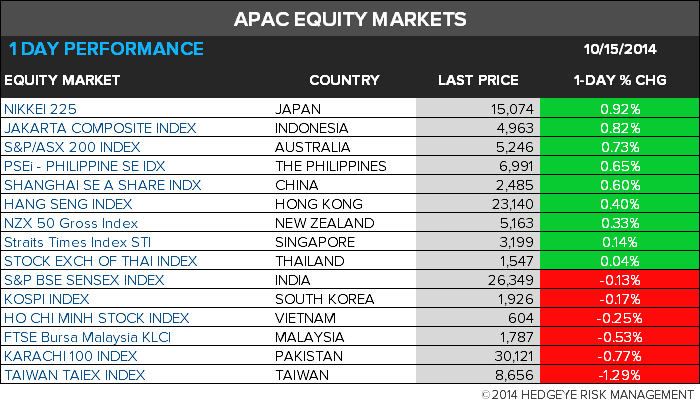

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team