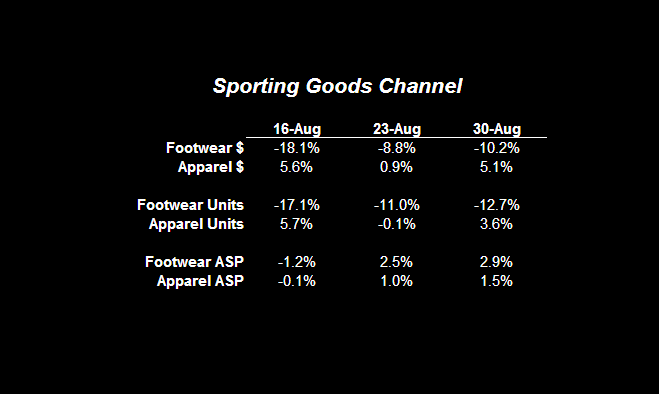

With the exception of UA and Jordan, footwear sales are not keeping track with the stronger numbers we are seeing in apparel. The charts enclosed tell all. The good news is that ASPs remain strong. But with rising inventories in the athletic channel, price point strength might be short lived. For the first time in a while, we prefer the family footwear channel.