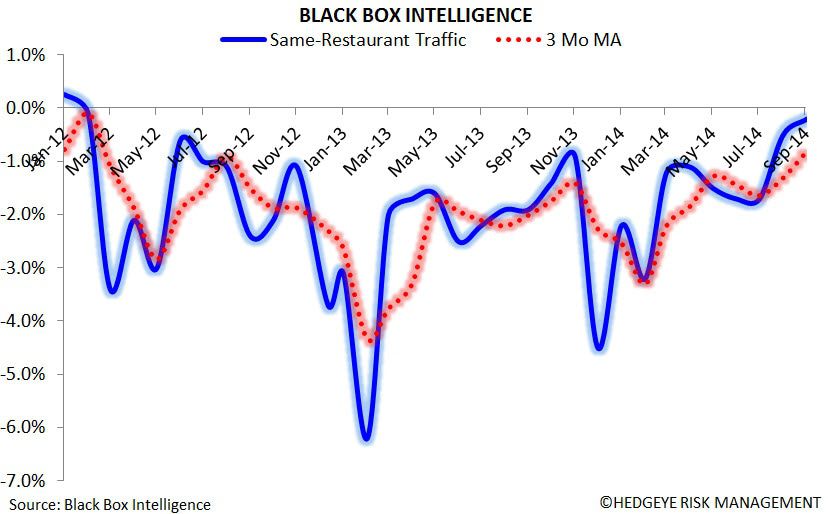

Black Box numbers indicate same-store sales increased +2.2% in September, in what was yet another bullish release for the restaurant industry. This same-store sales gain represents a 10 bps sequential improvement over a strong August. Traffic declined -0.2%, representing a 30 bps improvement over August. All told, these are the best monthly, and quarterly, numbers we've seen since 1Q12.

Although we're not insinuating this is the defining turning point in the industry, particularly in regards to casual diners, we'd be remiss not to respect the data. Easy comparisons in 4Q14 set the industry up for continued momentum heading into what looks to be a strong finish to the year. Importantly, this recovery is not geographically constrained. Black Box reported September sales improved in 159 markets, while only declining in 29. This is the best up/down ratio we have seen since we started tracking the data back in 2011.

With that being said, we're confident that a vast majority of restaurant companies will have same-store sales estimates revised upward in the coming months. As it stands, estimates for both 3Q and 4Q appear conservative. Below, we take a look back at what consensus same-store sales estimates were at the beginning of 3Q and compare them to current estimates.

system-wide SAME-STORE SALES ESTIMATES

As you can see, despite three months of sequential improvements in industry sales numbers, the majority of estimates have been revised down since the nascent days of July. This signals to us that there is currently a disconnect between estimates and reality. We expect this gap to close over the coming weeks, but all indications suggest we will see a fair amount of upside surprises as earnings season progresses. We covered our two remaining casual dining shorts (DFRG, EAT) for this reason in a note yesterday.

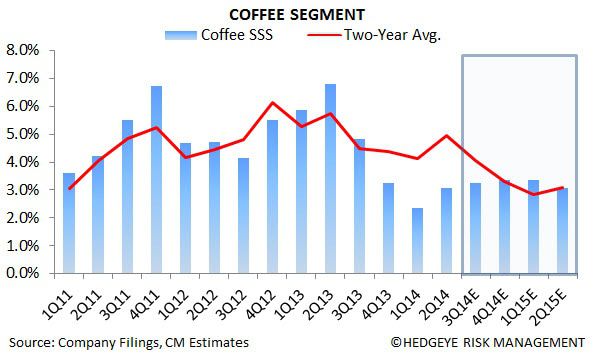

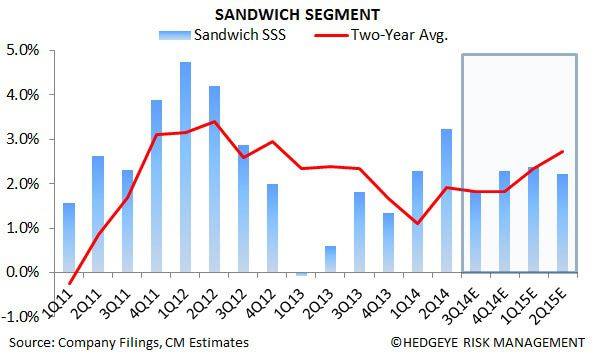

Current estimates across many sub-sectors of the restaurant industry suggest a sequential decelerations in two-year trends in 3Q14, clearly inconsistent with recent data points. Lower gas prices, lower food away from home prices, increasing disposable income, strong employment trends and improving consumer confidence are all current tailwinds to the industry. Stocks should rise simultaneously with increasing estimates. We've been very active on the short side throughout 2014, but believe it is prudent to cover and look for better entry opportunities in a month or two. We continue to have a healthy short bench that we will begin picking from when we feel the time is right.

Sub-Sector Same-Store Sales Estimates

3Q and 4Q numbers must, and will, be revised upward. Current estimates are too low across nearly all sub-sectors.

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst