“Some day, following the example of the United States of America, there will be a United States of Europe.”

-George Washington

Well, if Washington is right, “some day” is still a long ways off.

In fact, over the intermediate to longer term we expect the culture clash that is the Eurozone to continue transpiring – from the top (Brussels and the ECB) right on down to the bottom (individual member states).

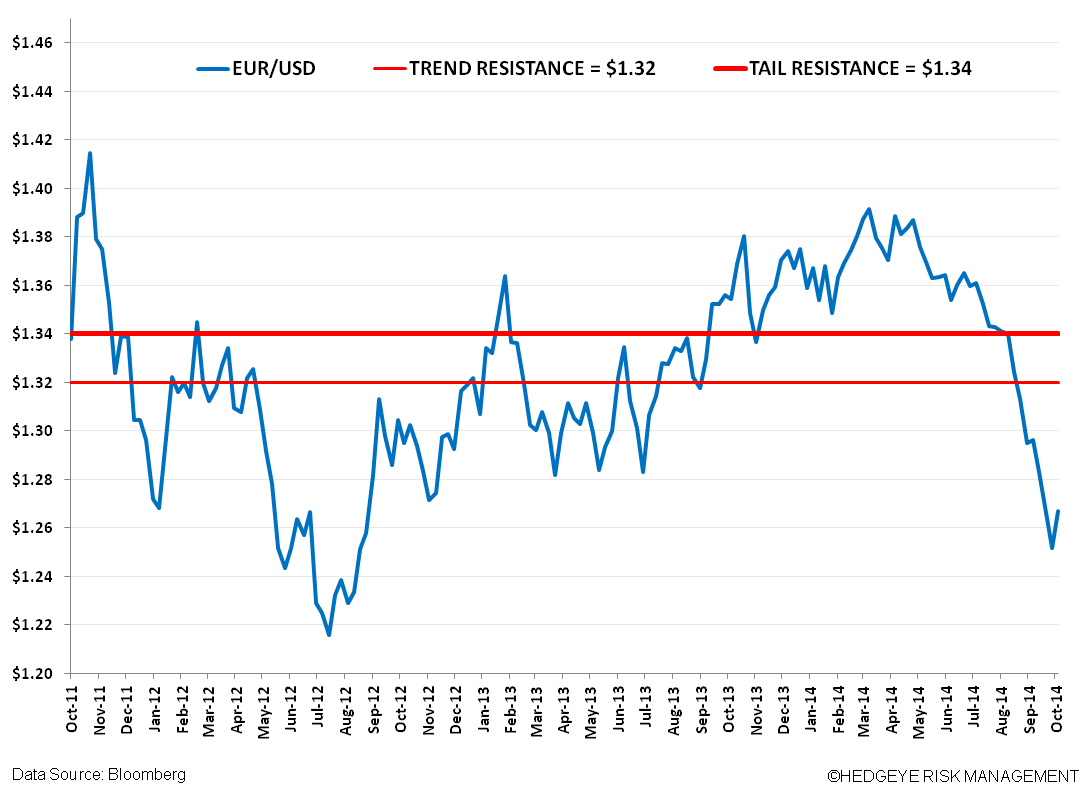

Our macro playbook continues pointing to a Euro with potential downside from here (it’s down around -9% since May and is broken across TREND and TAIL durations in our quantitative models). Despite ECB President Mario’s Draghi’s pledge “to do whatever it takes” (and lever up the balance sheet by €1 Trillion) to support growth and inflation, we’re not buying the promise of Draghi’s Drugs producing sustainable economic growth.

Why? Because we expect some member states to be very slow in passing the necessary fiscal and labor market reforms to improve their competitiveness.

Back to the Global Macro Grind…

And so the culture clash took another turn this week when the French government announced that austerity is dead and that it would not meet its original deficit reduction target. This shot across the bow stands to reignite tension with the fiscally conservative member states (Germany in particular) and may influence the policy stance of other members (like Italy) that have A) long questioned the merit of austerity, B) have yet to deliver on a full package of reforms, and C) like France, are looking to push out their own deficit timetable.

Specifically, France in its 2015 budget stipulated that it would adapt a pace of deficit reduction parallel to the economic situation of the country. Therefore, instead of meeting the original target of 3% deficit by 2015, the country would push out that target by an additional two years.

And so for the first time in history, the European Commission may exercise its power to reject France’s budget and ask for a new one. A resolution could come at the end of the month.

In follow-up remarks, French Finance Minister Michel Sapin has said that the EU must shift its policy to avert the threat of prolonged low growth and low inflation (along with boosting investment), if Europe was to prevent being stuck in Japanese-style stagnation.

Here’s the rub playing out from Top to Bottom:

- The European Commission (EC) and ECB: (pointing the finger at a select group of member states): “You guys need to reform (more).”

- The Member States Being Accused: (pointing the finger back) “We just issued loads of “austerity” to minimize the public sector, reduce our borrowing costs and improve our credit rating, yet in doing so we’ve choked off growth, are saddled with record high unemployment rates, and have zero ability to manipulate policy to make ourselves more competitive than our European peers. We’re done with this course of action, so be your expectations for deficit and debt consolidation!”

- The EC and ECB: “But if you don’t reform at the state level, there’s no chance our newest programs (ABS & covered bond buying programs and TLTROs) will have any chance of success!”

The problem is that countries like France haven’t done enough. For proof of the shortfall, France’s government spending still stands at a monster 55% of GDP. And as an anecdote, the Magic Kingdom a la France (Disneyland Paris) reported this week that it needs a bailout to the tune of $1.25 Billion. The company cited French labor laws and planning regulations making it difficult to replicate the success of the other Disney enterprises, and called-out in particular the high cost of employing French workers.

Similar structural shortfalls could be identified in Italy, which just this Wednesday happened to host an EU Summit in Milan to discuss job creation.

And so as the “rub” between the Top and Bottom plays out, Eurozone growth stands to suffer as there’s no clear action plan on how to fix it. This week the IMF (a classic lagging indicator) revised down its global GDP forecast and specifically took the Eurozone GDP outlook to 0.8% in 2014 (vs a prior estimate of 1.1% July) and 1.3% in 2015 (vs prior 1.5%).

A quick look at key Eurozone data metrics over the last two weeks shows a similar trend downward:

- Eurozone PMI Services fell to 52.4 SEPT (exp. 52.8)

- Eurozone PMI Manufacturing fell to 50.3 SEPT (exp. 50.5)

- Eurozone PMI Retail Sales 44.8 SEPT vs 45.8 AUG

- Eurozone Sentix Investor Confidence -13.7 OCT (exp. -11) and -9.8 SEPT

- Eurozone Business Climate 0.07 SEPT (exp. 0.10) vs 0.16 AUG

- Eurozone Economic Confidence 99.9 SEPT (inline) vs 100.6 AUG

- Eurozone Industrial Confidence -5.5 SEPT (exp. -5.8) vs -5.3 AUG

- Eurozone Consumer Confidence -11.4 SEPT vs -10 AUG

- Eurozone Unemployment Rate UNCH at 11.5% AUG

- Eurozone CPI fell 10bps to 0.3% Y/Y in SEPT

Our bottom-up, qualitative analysis (e.g. our Growth/Inflation/Policy framework) indicates that the Eurozone is setting up to enter the ugly Quad4 in Q4 (equating to growth decelerates and inflation decelerates). We discussed this point in depth on our Q4 2014 Macro Themes Call on 10/2 (email if you’d like access) in our theme #EuropeSlowing (one of three).

Our key conclusions include:

- We do not believe Draghi will be able to turn the tide of deflation (see chart below) and growth through his policy tools alone. German Finance Minister Wolfgang Schaeuble has repeatedly said the ECB has “run out of tools” and that “cheap money can’t force growth”

- We expect the recent package of “supportive” measures (ABS and covered bond purchasing program and TLTRO) to come up short of expectations. Recall as an initial read-through that demand was light for the first round of TLTRO at €83 Billion vs estimates of €150-300 Billion

- Should Sovereign QE become a reality, expect push back from member states (think uproar over OMT and hearings from the German Constitutional Court)

- We believe it’s still largely unlikely that a sovereign QE program can support sustained economic growth (witness years of shortcoming on this front from the Japanese).

- From an investment position, we are recommending shorting French (EWQ) and Italian (EWI) equities and the EUR/USD (FXE).

The former President of France Jacques Chirac once said: “The construction of Europe is an art. It is the art of the possible”. Indeed, if the Eurozone is to become a functioning United States of Europe, it’s just in the initial sketch stage.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1

DAX 8

USD 84.89-86.63

EUR/USD 1.25-1.27

WTI Oil 84.02-89.82

Gold 1195-1230

Matthew Hedrick

Associate