From a policy calculus perspective, the existent labor & macro market dynamics can be sufficient summarized by the following duality:

ROW Growth Slowing + Global Disinflation Predominating + Domestic Wage Growth Decelerating + LFPR declining vs. Strong Initial Claims + Solid NFP Gains + Declining Unemployment Rate + Accelerating Aggregate Income Growth

Hilsy says rate hikes could come earlier than expected, inflation target’istas see lower-for-longer, the futures market is still (very slightly) leaning towards June.

On balance, we think the current labor and manufacturing market data support the expected cessation of QE in October while leaving the internal committee consensus largely unchanged with respect the prospective tightening timeline.

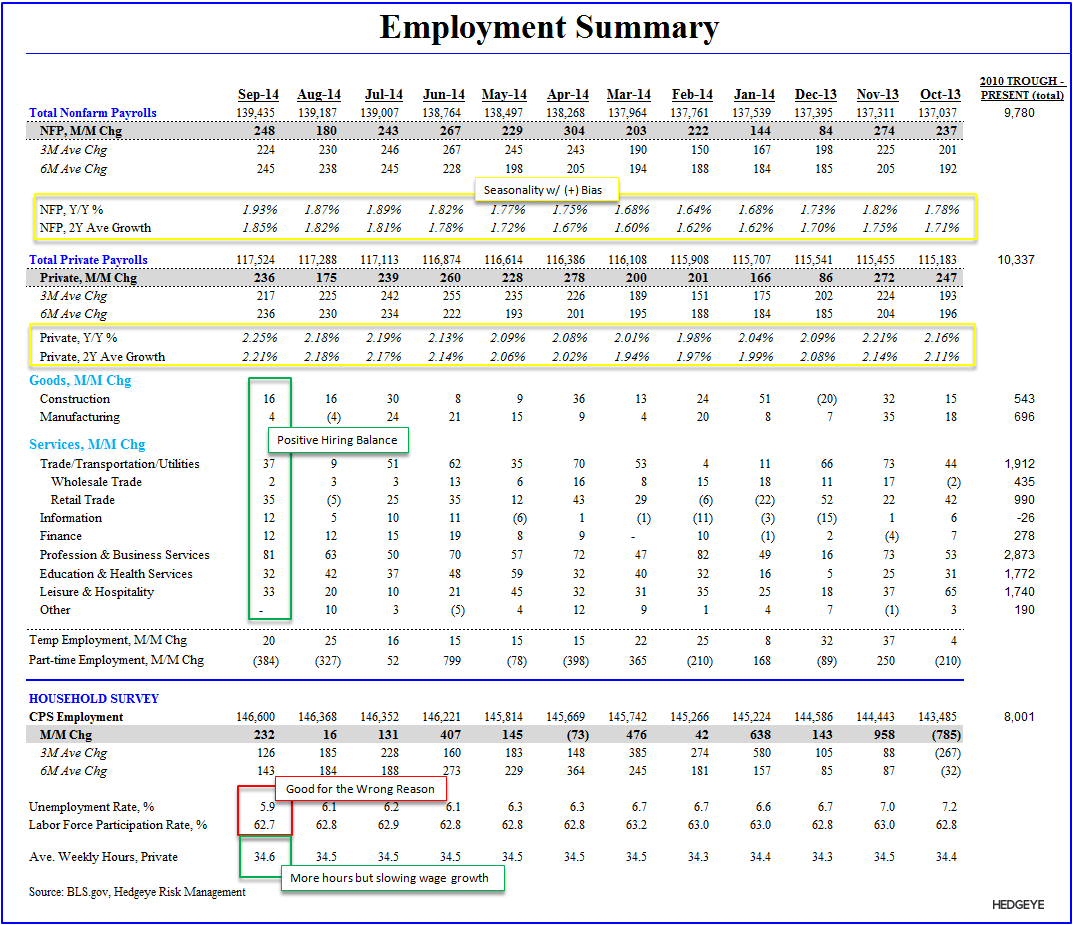

Overall: Solid Jobs report across the establishment survey with private payrolls (+236K) leading the headline gain of +248K, a positive +69K net revision to July/Aug extending the positive bias in revision trends, and solid gains across industries driving positive breadth/balance in September hiring.

On the negative side, wage growth was disappointing as average hourly earnings growth decelerated -20bps to +2.0% YoY while average hourly earnings for supervisory and nonproduction workers decelerated a big -60bps sequentially to +1.8% YoY – the slowest rate of growth in over a year.

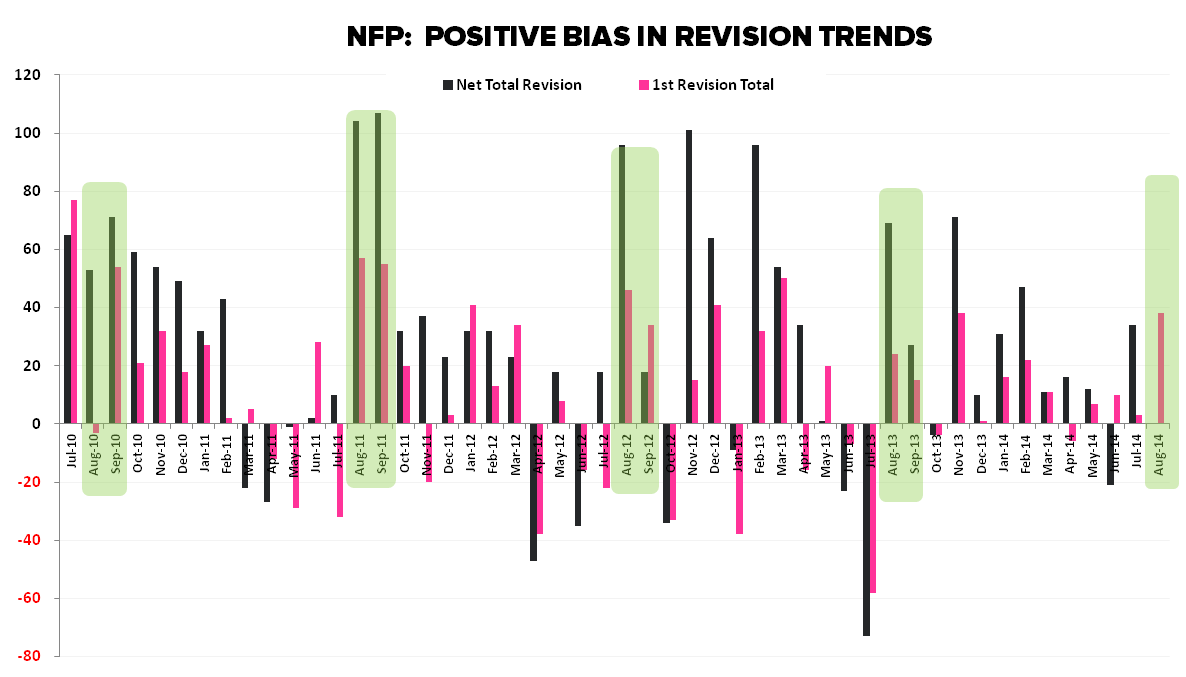

REVISION TRENDS: The two month net revision was +69K with July revised from +212K to +243K and August revised from +142K to +180K. The positive revision wasn’t particularly surprising given the broader positive bias in revision trends and the even stronger tendency for positive (& significant) revisions to the August (& September) data.

SEASONALITY & PEAK GROWTH: Seasonal distortions have been ubiquitous across the reported domestic macro data since the great recession as accelerated employment loss and the collapse in economic activity were, at least in part, captured as seasonal variation rather than as a bonafide shock.

Similar to the Initial Claims data, the NFP figures have reflected ongoing, albeit diminishing, seasonality in recent years resulting in largely steady growth rates alongside sometimes volatile month-to-month changes in the absolute data. For instance, while net job gains slowed materially last month (Aug) the YoY rate of growth in NFP was actually flat-to-up on both a 1Y and 2Y basis.

At +1.93% YoY, Nonfarm payrolls in September recorded their fastest rate of improvement since April 2006. The current pace of improvement is inline with peak growth in the last cycle and may be as good as it gets given the demographic and labor supply headwinds and the secular slowdown in employment growth over the last 30 years.

WAGE GROWTH, INCOME & CONSUMPTION: Ave Hourly Wage growth was the most disappointing series in the release, growing +0% MoM and decelerating -20bps sequentially to +2.0% YoY.

Even more disappointing was wage growth for Production and NonSupervisory employees. After hitting at a 4-year high of +2.4% YoY last month, wage growth slowed a material -80bps sequentially to +1.8% in September – the slowest pace in over a year.

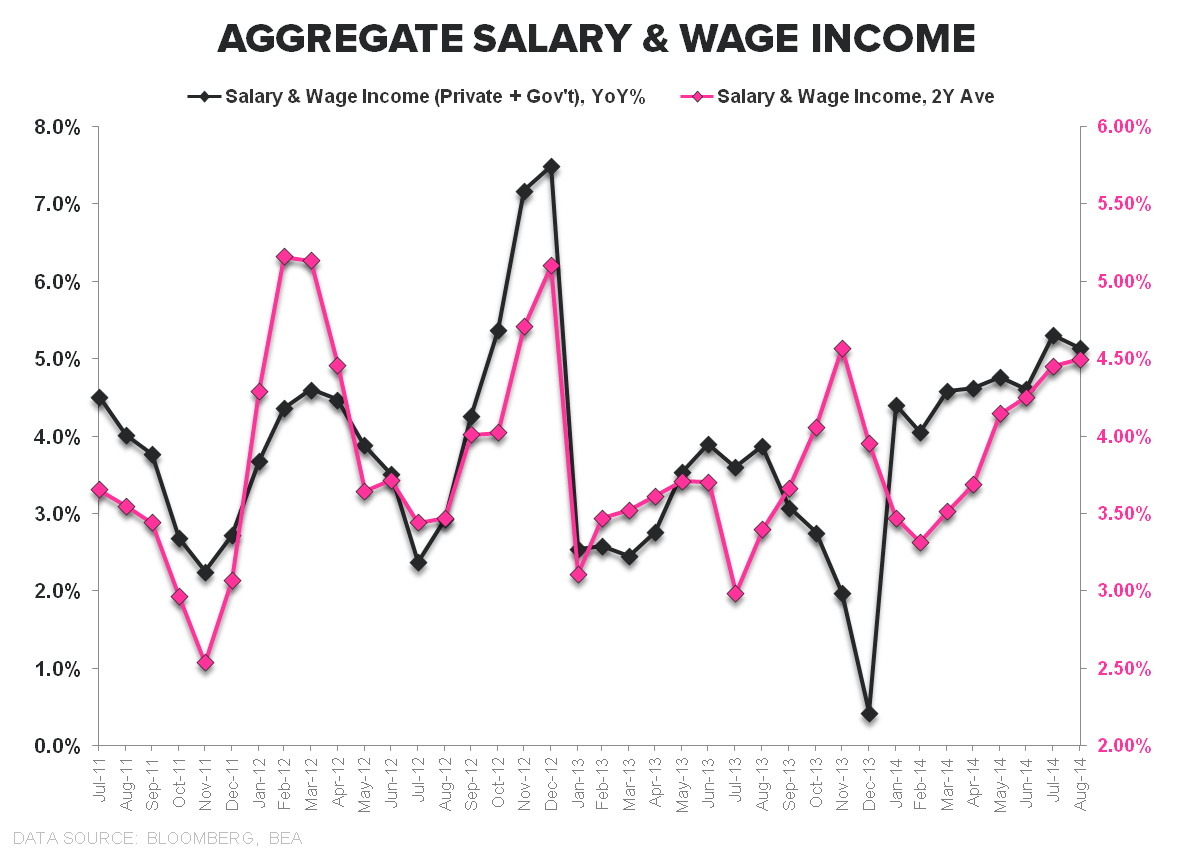

BUT.....despite weakening wage growth, in combination with an accelerating employment base, the confluence should be enough to keep aggregate income on its current positive trajectory. Aggregate private sector salary & wage growth is currently running at +5.8% and holding at its best levels of the recovery outside of the peri-fiscal cliff (income pull-forward) period.

As we’ve highlighted, the acceleration in income growth certainly supports the capacity for rising consumption growth. Its been the steady rise in the savings rate alongside the income acceleration that has depressed the translation to actual household spending growth.

CYCLE ACCOUNTING: In yesterday’s parsing of the Initial Claims data, we highlighted the temporal relationship between claims and equities as claims reach their frictional lower bound at the ~300K level.

To recapitulate, the chart below shows that over the last two cycles rolling SA claims ran at sub-330k for 45 and 31 months, respectively, before the corresponding market peaks in March, 2000 and October, 2007. We are currently in month seven at the sub-330K level in the present cycle.

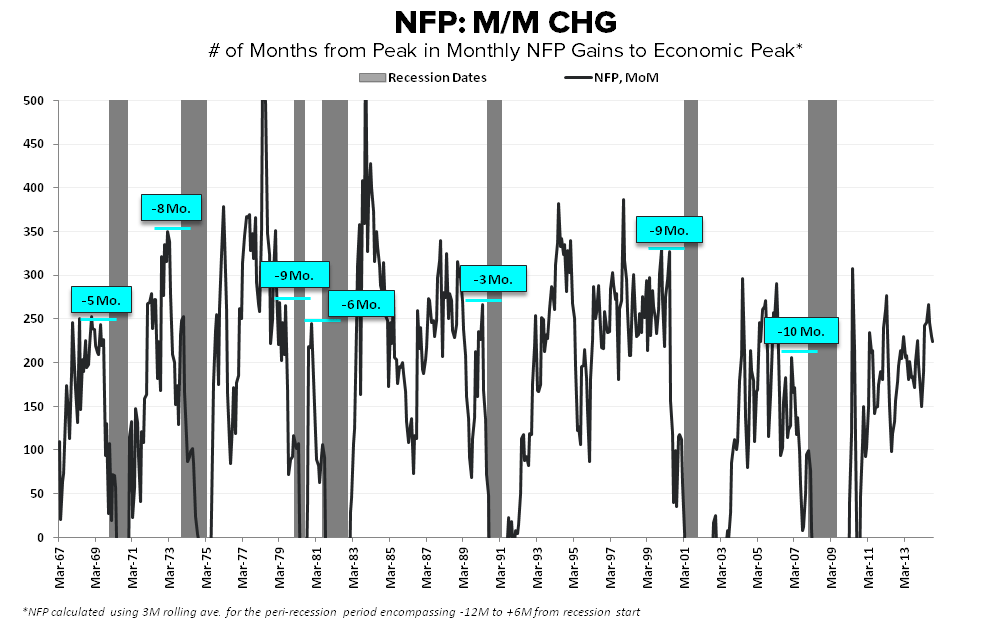

In relation to economic cycle precedents, historically, over the last half century, initial claims and peak monthly NFP gains have led the peak in equities and the peak in the economic cycle by 3 months and 7 months (using 3Mo rolling averages of the data), respectively.

Whether the current level of claims or the May-July NFP gains represented peak improvement in those measures remains to be seen, but it’s worth monitoring given the fairly consistent temporal sequence in the labor --> equity market --> economy over the last half century.

SLACK: The U-6 rate fell to 11.8% from 12.0%, falling at a premium to the U-3 rate and providing for a small compression in the spread between the two.

The short-term unemployment rate (those employed <5wks, % of Total Unemployed) retreated to 25.7%, down from its best level of the cycle last month at 27.4%.

Those working part-time for economic reasons showed modest improvement in September, dropping -170K sequentially to 7.1MM.

BASEMENT DWELLING: Employment growth for the 25-34 YOA age demographic, which sits as the center for 1st time homebuyer demand, didn’t inflect until late 2012. The broader trend has been positive over the last 18 months with growth accelerating above the 2% level over the last four months.

Intuitively, housing demand from this demographic could be expected to improve over the intermediate term as employment growth matures, savings time accumulates, and work history reaches a duration necessary to satisfy mortgage underwriting standards in a tighter regulatory environment.

Christian B. Drake

@HedgeyeUSA