This note was originally published October 03, 2014 at 09:04 in Retail

Last night (Thursday night) RH announced a long-term financing program that we think is positive news for its top line. The company already offers a credit card, but that carries a much higher interest rate (24.99%) and is a shorter-term financing bridge for consumers. With the new RH program, consumers can finance purchases at 5.99% for a duration ranging from 24 months to 7-years.

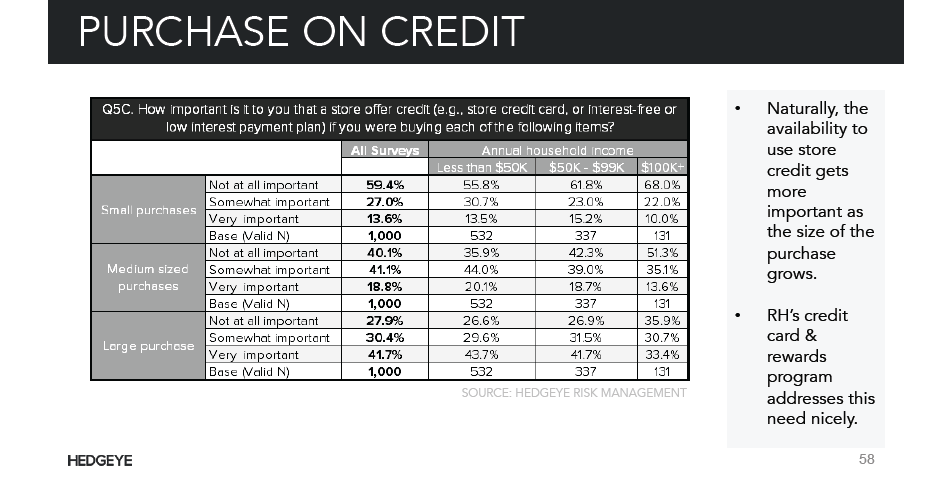

There's no question for us that this is a positive for RH's top line. In our latest RH consumer survey, we asked 1,000 consumers how important it is for a furniture store to offer store credit -- on small, medium and large purchases. Interestingly, it is 'Very Important' to only 13.6% of consumers for 'Small Purchases' and only '18.8% for 'Medium Purchases'. But once we get into the 'Large Purchase' classification, it is 'Very Important' for 41.7% of customers. Even 33.4% of the $100k+ demographic said that it Very Important to their purchasing decision.

An interesting note is the screen shot below that 'advertises' consumers to meet with RH designers. This is the first time we EVER saw this advertised by the company. Approximately 40% of RH's business comes from designers, but they are largely third party designers. These are people that are hired by a customer and shop dozens of stores, where they pick and choose assortments that work -- maybe including RH, maybe not.

But now RH not only has a massive product assortment (i.e. 3,300 pages), but a stepped-up in-house Interior Design team AND a superior long-term financing program. Add all that up and you get a stealth revenue driver that will build meaningfully. We're not taking up our estimates (which are already high on the street by a country mile) but these factors give us more confidence that the company will get there.