TODAY’S S&P 500 SET-UP – September 30, 2014

As we look at today's setup for the S&P 500, the range is 25 points or 0.80% downside to 1962 and 0.47% upside to 1987.

SECTOR PERFORMANCE

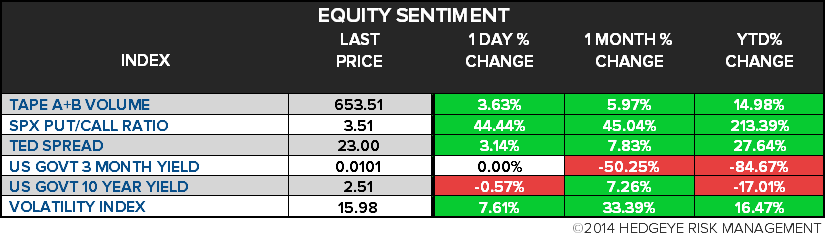

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.93 from 1.91

- VIX closed at 15.98 1 day percent change of 7.61%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:55am: Redbook weekly sales

- 9am: ISM Milwaukee, Sept., est. 61 (prior 59.63)

- 9am: S&P/Case-Shiller Home Prices m/m July est 0.0% (pr -0.2%)

- 9:45am: Chicago Purchasing Mgr, Sept., est. 62 (prior 64.3)

- 10am: Consumer Confidence Index, Sept., est. 92.5 (pr 92.4)

- 10:45am: Fed’s Powell speaks in Washington

- 11:30am: U.S. to sell $30b 4W bills

- 3pm: Fed issues QE schedule for Oct.

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- Senate, House out of session

- Obama, Modi hold bilateral meetings at White House

- 10am: House Oversight and Govt. Reform Cmte hearing on Secret Service security protocols w/agency director Pierson

- 10:30am: FCC open meeting; subjects incl. sports blackouts

- 12:30pm-2:15pm: Hillary Clinton speaks at Congressional Hispanic Caucus Institute conference

- 2pm: Attorney General Eric Holder delivers remarks at Global Alliance Conf. against child sexual abuse

- 3:45pm: Speaker Boehner, Democratic leader Pelosi, Modi media availablity after meeting

- U.S. ELECTION WRAP: Ballot Law Key in Kan. Race; Sen. Outlook

WHAT TO WATCH:

- iPhone 6, 6 Plus to be available in China from Oct. 17

- Apple’s Irish tax deal doesn’t comply with EU standards

- U.S. seeks to reverse locks on Apple, Google smartphone data

- Iron Mountain said to consider more than $2b Recall bid

- FCC said to consider rules to help web TV svcs. access shows

- Netflix to co-produce ‘Crouching Tiger’ sequel

- Computer Sciences said to approach Blackstone, Bain on LBO

- AMC said close to $200m deal for stake in BCC America

- Argentina found in contempt of court on bond payment fight

- Euro-region inflation slows as ECB prepares for policy meeting

- Pimco talks to Morgan Stanley, BofAML on strategy: WSJ

- Total Return fund cut to bronze by Morningstar

- GM CEO Barra to give detailed plan for cash, WSJ says

- Schlumberger said to remove U.S., EU staff from Russia

- Supervalu, Albertson’s discover new holes in card networks

- AIG bailout by U.S. was ‘extortion,’ Greenberg lawyer says

- Lawmakers to quiz Secret Service chief on White House breaches

- Venezuela’s Maduro says on TV that Clorox abandoned country

EARNINGS:

- Walgreen (WAG) 7:30am, $0.74 - Preview

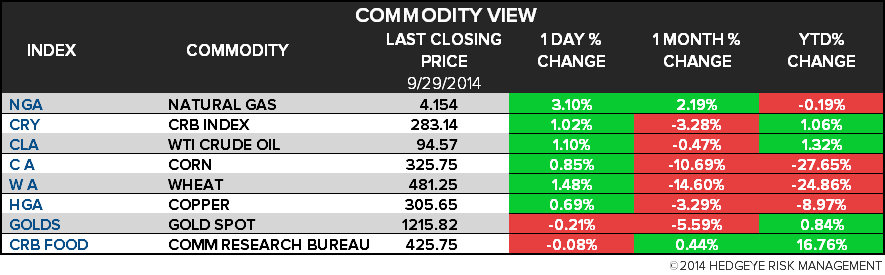

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Falls to Lowest Since January as Metal Set for Monthly Drop

- Oil Heads for Biggest Quarterly Drop Since 2012 on Ample Supply

- Gluts Spur Investor Exit Signaling Prolonged Slump: Commodities

- European Coal Set for 10th Quarterly Drop as Power Demand Wanes

- Iron Ore Heads for Record Run of Losses as Global Surplus Builds

- Freeport Says Grasberg Copper Shipments Continue Amid Suspension

- Rubber in Tokyo Trims Third Quarterly Loss as Thai Exports Fall

- U.K.’s Wheat Farmers May Delay Planting After Driest September

- Soybeans Head for Quarterly Slide Before USDA on Harvest Outlook

- Nasdaq OMX Plans First German Renewable Power Futures in 2015

- Rebar Pares Record Quarterly Loss as Recent Drop Seen Excessive

- Corn Price Rout Seen Nearly Complete by UBS as U.S. to Cut Area

- Dubai Gold & Commodities Exchange Pushes Back New Gold Contract

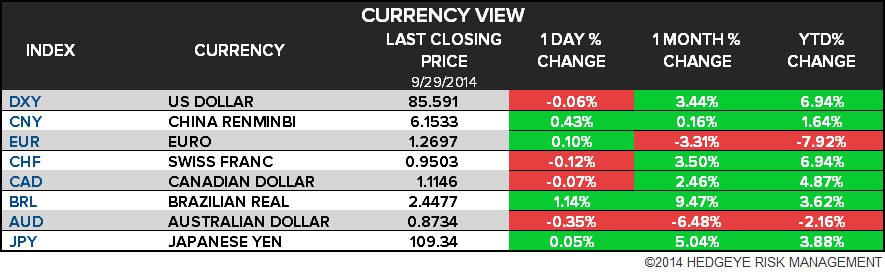

CURRENCIES

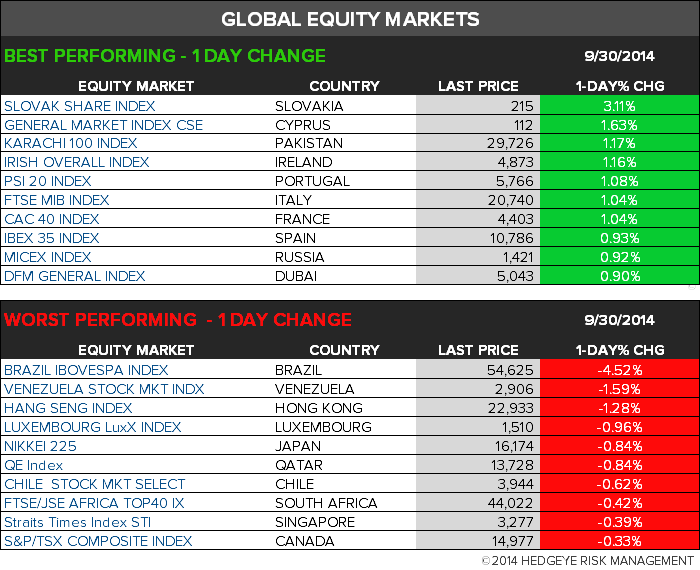

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team