TODAY’S S&P 500 SET-UP – September 25, 2014

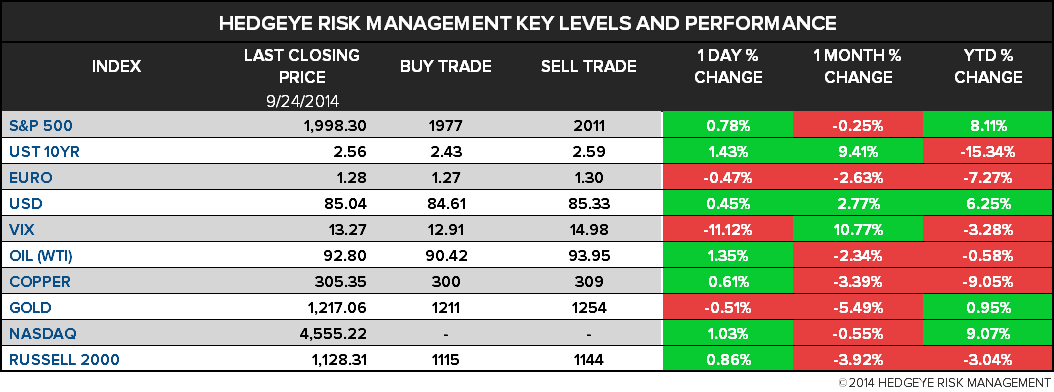

As we look at today's setup for the S&P 500, the range is 34 points or 1.07% downside to 1977 and 0.64% upside to 2011.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.97 from 1.98

- VIX closed at 13.27 1 day percent change of -11.12%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Initial Jobless Claims, Sept. 20, est. 296k (pr 280k)

- 8:30am: Durable Goods Orders, Aug., est. -18% (prior 22.6%)

- 9:45am: Markit US Services PMI, Sept., est. 59.2 (prior 59.5)

- 9:45am: Bloomberg Consumer Comfort, Sept. 21 (prior 37.2)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Kansas City Fed Mfg Activity, Sept., est. 6 (prior 3)

- 1pm: U.S. to sell $29b 7Y notes

- 1:20pm: Fed’s Lockhart speaks in Jackson, Miss.

GOVERNMENT:

- Senate, House out of session

- President Obama speaks at UN meeting on Ebola

- Congressional Black Caucus holds 44th legislative conference: speakers incl. Reps. Lewis, D-Ga.; Rep. Becerra, D-Calif.

- 9:30am: Gen. David Perkins speaks on role, U.S. Army’s future

- U.S. ELECTION WRAP: Ads Pulled; Possum Festival; Cosmo Endorse

WHAT TO WATCH:

- U.S.-Arab Strikes Hit Islamic State Oil Refineries in Syria

- U.K. Seeks to Criminalize Rigging of Seven More Benchmarks

- DHL Beats Amazon, Google to First Scheduled Drone Delivery

- Pimco’s ETF Probe Is Said to Be Separate From Broader SEC Sweep

- Apple to Release Fix for IOS Update Issues in “Next Few Days”

- Ford Tops Hiring Pledge Adding 14,000 Workers in U.S. Since 2011

- Shorting Alibaba Costs 7% to Borrow Shrs Following Biggest IPO

- Harvard Names Stephen Blyth to Run $36.4b Endowment

- Gold Downside Risk Seen ‘Significant’ to Goldman Sachs’s Currie

- GE Said to Pick Banks for Australian Consumer Finance Unit Sale

- Microchip Deadline to Make Offer for CSR Extended to Oct. 15

EARNINGS:

- Diamond Foods (DMND) 4:01pm, $0.15

- Micron Technology (MU) 4:02pm, $0.81

- NIKE (NKE) 4:15pm, $0.88 - Preview

- Progress Software (PRGS) 4:15pm, $0.33

- Scholastic (SCHL) 7am, ($0.84)

- Thor Industries (THO) 4:15pm, $1.23

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China’s Forex Watchdog Uncovers $10 Billion in Fraudulent Trade

- Currency to Oil Benchmarks Targeted as U.K. Extends Penalties

- Sweet-Sour Spread Will Narrow Further When OPEC Cuts: Julian Lee

- Vale Sees China Iron Ore Imports Rising to Absorb Seaborne Glut

- Copper to Aluminum Fall as Stronger Dollar Curbs Investor Demand

- Gold Premium in India Seen Doubling as Festivals Fuel Demand

- Rubber Drops for Five Days to Five-Year Low on Demand Concern

- UkrAgroConsult to Cut Ukraine Corn Crop Estimate to 25.9m Mt

- Blackouts Threaten South Africa Growth as Utility Decays: Energy

- EU Can Cope With Russia Gas Disruption Under Normal Winter: Citi

- LME Aluminum Canceled Warrants in Detroit Rise Most Since 2012

- France Imports Wheat From Canada and Belgium in Sept. 24 Week

- Uganda’s Tea Production on Course to at Least Match Last Year

- WTI Trades Near 1-Week High as U.S. Supplies Drop; Brent Steady

CURRENCIES

GLOBAL PERFORMANCE

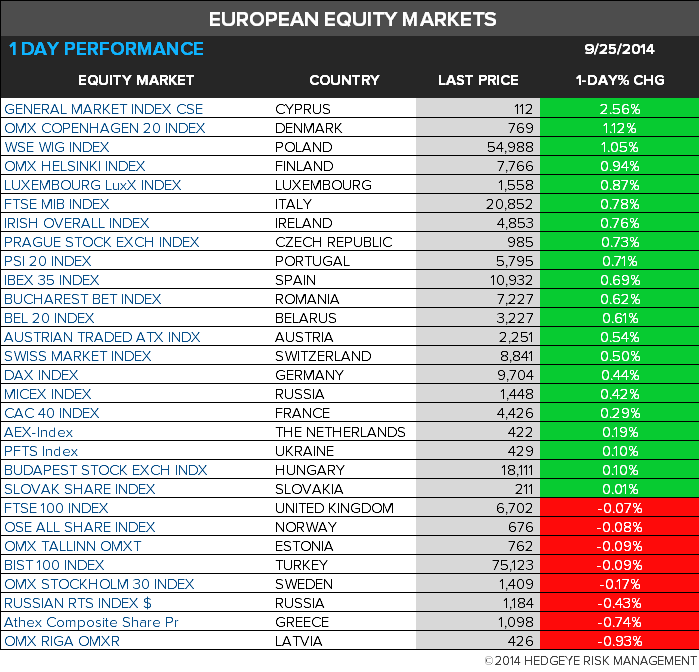

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team