TODAY’S S&P 500 SET-UP – September 19, 2014

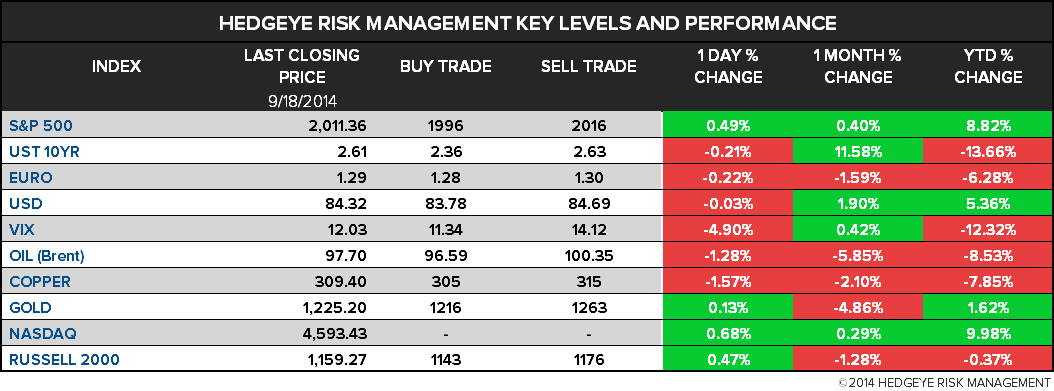

As we look at today's setup for the S&P 500, the range is 20 points or 0.76% downside to 1996 and 0.23% upside to 2016.

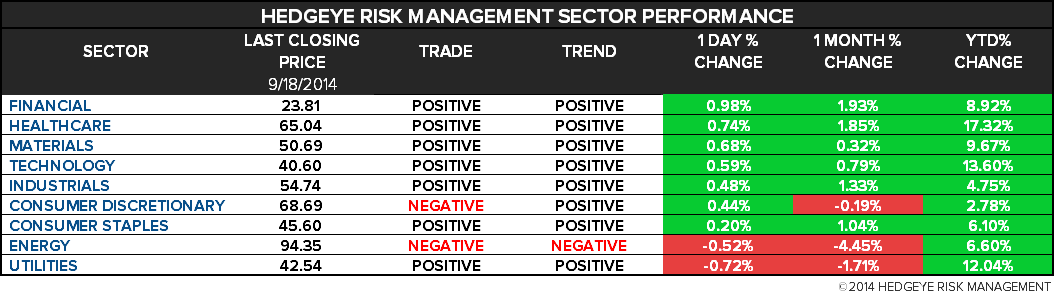

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.05 from 2.05

- VIX closed at 12.03 1 day percent change of -4.90%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Leading Economic Indicators, Aug., est. 0.4% (pr 0.9%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- 8am: House Intelligence Chairman Mike Rogers, R-Mich., delivers keynote Intelligence and National Security Summit

- 9:30am: Sec. of State John Kerry remarks on importance of inclusive economic growth at New Frontiers in Development forum

- 2pm: Kerry chairs UN Security Council Iraq ministerial debate

- 10am, 1:30pm: FCC holds open Internet roundtable discussions

- 1pm: CVS CEO Merlo speaks at Nat’l Press Club

- U.S. ELECTION WRAP: La., Colo., Kan. Polls; Adelson Donations

WHAT TO WATCH:

- Scotland rejects independence 55% to 45%

- Alibaba raises $21.8b in U.S. IPO

- Ellison becomes Oracle chairman as Catz, Hurd split CEO job

- SAP to buy Concur for $129/share or ~$7.4b

- Home Depot says data breach affected 56m payment cards

- Arkema bids $2.2b for Total’s Bostik adhesives business

- Telefonica to buy Vivendi’s Brazil unit GVT for $9b

- JetBlue names Hayes as CEO as Barger leaving at contract end

- Clorox says executive Benno Dorer to succeed Knauss as CEO

- AIG says Wintrob departs after being passed over for CEO job

- Goldman Sachs faces SEC probe on internship for Libyan: WSJ

- Regulators said to weigh delay for separating banks’ swaps units

- Exxon said to halt Arctic well drilling on Russian sanctions

- Congress clears spending bill with U.S. aid to Syrian rebels

- Lockheed said close to $4b F-35 deal with Pentagon: Reuters

- U.S. said to see chance for progress in nuclear talks with Iran

- Apple IPhone 6 Plus contains Hynix, BRCM, QCOM: iFixit teardown

- China fines Glaxo $489m, ending investigation of bribery

- U.K. prosecutors said to ready more charges on Libor this year

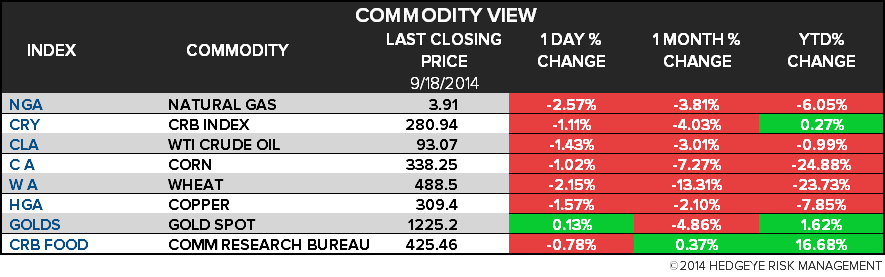

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Oil Falls as Fed Outlook Counters Supply Risk; Brent Steady

- Fortescue’s Forrest Lauds China City Push as Iron Ore Slumps

- Natural Gas Supply Gain Hides Risk of Winter Price Shock: Energy

- Gold Falls Toward 8-Month Low as Fed Outlook Strengthens Dollar

- Copper Heads for a Fourth Weekly Decline on Slowdown in Housing

- Cocoa Climbs to Three-Year High as Ebola Seen Risk to Production

- Wheat Extends Drop to 4-Year Low as Demand Wanes Amid More Crops

- EU Emissions Drop Seen Accelerating as Lawmakers Mull Supply Fix

- Earth Baked in Record Fashion This Summer Even If You Were Cool

- Soybean Traders Bearish for Sixth Week on U.S. Harvest Outlook

- Oil Clogging U.S. Rail Seen Constricting Grain Exports: Freight

- Libya Resumes Oil Flows to EU as Africa Exports Remain Subdued

- Rebar Falls to Record Low as Weak Property Sector Hurts Demand

- India Monsoon Food Grain Output Seen Falling 6.9% to 120.3m Tons

CURRENCIES

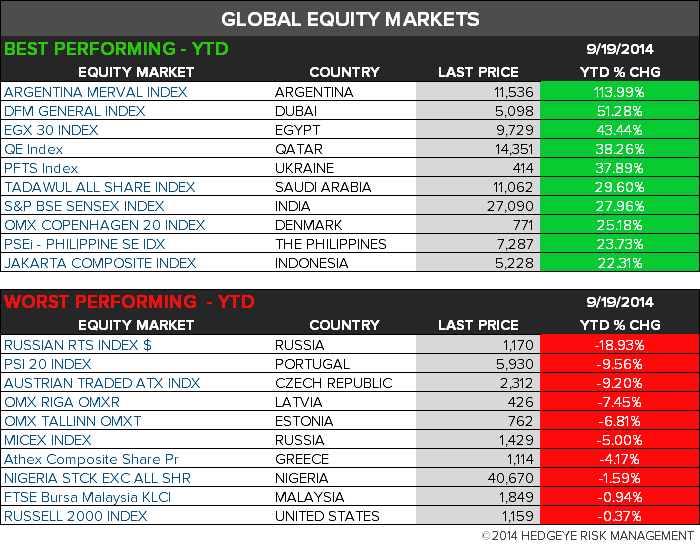

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team