This note was originally published at 8am on August 29, 2014 for Hedgeye subscribers.

“Because there is no effort without error and shortcoming.”

-Teddy Roosevelt

That’s one of the best quotes from one of the best leadership speeches in American history – President Teddy Roosevelt’s “The Man In The Arena” (more formally referred to by political types as his “Citizenship in a Republic” speech).

I’m not much of a political type. I’m more of a Mucker in the arena type. Perversely, I love getting smacked around once in a while. I love to fight against consensus. Yes, it can get messy. But working alongside those of you whose portfolios are “marred by dust and sweat and blood” drives me.

Those of you who didn’t get run over buying the tops of the 2000 and 2007 US stock market bubbles get where I am coming from. We are going to do this all over again. And while this time may be different, we know “the triumph of high achievement” … and if we fail, at least we’ll do so “while daring greatly.”

Back to the Global Macro Grind…

I obviously love that speech, but I don’t think our call for US #GrowthSlowing as inflation accelerated (from 3 year lows) in 2014 was much of a dare at all. It was a playbook modeling call. Amidst all of the storytelling out there, the easiest US Macro positions to take were:

- Long Inflation Assets in 1H 2014 (JAN-JUN)

- Long Slow-Growth all year long (Long Bond and anything Equities that looks like a Bond)

- Short US Domestic Growth (Russell 2000)

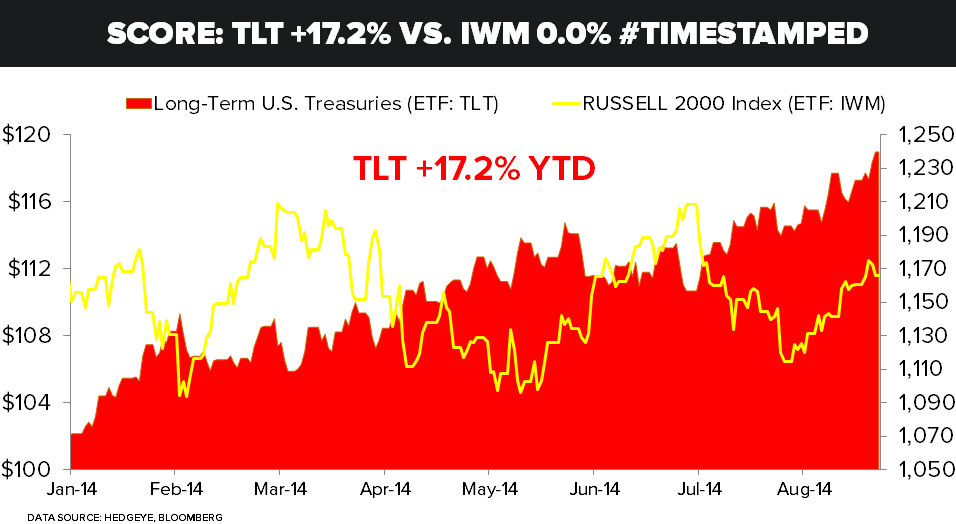

Score: Long Bond (TLT) +17.2% vs. Russell 2000 0.0% YTD #timestamped (10yr yield = 2.34%)

*that’s pre-reinvesting dividends if you are long the 30yr UST Bond, the absolute return is even better

But you won’t hear that on Old Wall TV. You probably won’t read that in the paper either (I certainly haven’t – mainly because I don’t read newspapers!). Instead, you’ll hear something from the cheap seats like, “look at the Dow – its above its 50-day moving avg.”

The Dow, btw, is up less than 3% for 2014. Thanks for coming out.

If you’re a hard core perma growth bull, where you should really be long is India. Unlike the Russell 20000, India’s stock market (BSE Sensex) closed the month at its YTD highs, +27.7% YTD. Inflation is falling there – and real consumption growth is accelerating. Sound familiar?

It certainly doesn’t sound like Europe.

European central planning bureaucrats (who are just like the un-elected ones we have here at the Fed) live in perpetual fear of what the general population wants (hint: lower cost of living). Read their conflicted and compromised media headlines this morning:

- “Eurozone deflation risk at its highest level since 2009”

- “Draghi hints at more stimulus”

This isn’t the arena of real life where real players have a real scoreboard. This is a joke.

For those of you who recall what the Keynesian finance newspaper (The Economist) was trumpeting last year (Abenomics), only 1-year after implementing 60-70 TRILLION Yen in incremental “easing”, here’s what Japan reported for July 2014:

- Japanese inflation +3.4% y/y

- Japanese Household Spending -5.9% y/y

- Japanese Housing Starts -14.1% y/y

In Hedgeye rate of change speak, “y/y” means year-over-year (or what it is now versus last year). And in Japan it’s just plain sad to watch. If you’re blowing up on the golf course this weekend, try it yourself – just keep doing the same things, over, and over, and over again. But don’t expect different results.

“So” Europe definitely needs to do that… definitely, right?

Right, right. And as US growth continues to slow from this fanciful Q2 headline Obama was trying to trumpet yesterday (newsflash: it’s Q3), guess what your central planning committee at the Fed is going to do in the face of that? Must do moarrr easing…

With a few Hedgeye Best Short Ideas going against us (like YELP) right now, I have plenty of issues of my own to deal with, but a broken process is not one of them. If I had a broken process, I would either get fired or mocked.

Where I grew up, they call the place where people who get paid to get mocked a circus. That’s the perfect place for a bunch of unaccountable people who are bought and paid for by governments policies to perform.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.32-2.39%

SPX 1972-2009

RUT 1138-1175

Shanghai Comp 2181-2280

VIX 11.34-13.90

EUR/USD 1.31-1.33

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer