Macau stocks still in decline – have we bottomed?

CALL TO ACTION

We were early and first to make the “Mass Deceleration” call (see our June 13, 2014 note). The sell-side has caught up to this second leg of the Macau bear thesis stool (VIP turning negative was the first) and the stocks are well off their 2014 highs. We fear the third leg hasn’t yet played out which keeps us firmly in the negative camp despite valuations that are becoming more palatable. Q2 margin disappointment wasn’t just labor related, as widely reported by analysts, but such is the Hedgeye view. Mass margins, particularly in the premium segment, are being compressed as operators compete for a slower expanding pie – reinvestment rates are going higher. Given our long term positive view, we are actively looking for the opportunity to pivot to a more constructive near term outlook for the stocks. However, with no positive fundamental pivot in sight and our own models computing generally lower than Street estimates for Q3, Q4 and 1H 2015, we can only conclude that the Macau stocks are likely to retreat. Our caveat to the negative sector outlook is Galaxy Entertainment where we are favorably inclined to buy despite our negative overall view.

THE SET-UP

As early as March 10, we pivoted to the sidelines when we removed LVS from our Best Ideas list - see our note “LVS: REMOVING FROM INVESTING IDEAS”- and shortly thereafter warned investors about junket issues, the Dept of State request to lower the threshold for reportable financial transactions, UnionPay, money laundering scrutiny, as well as the extreme sentiment indicator with the massive “buy” rating skew on MGM, LVS, WYNN, and MPEL. Our view was that VIP would suffer under such scrutiny and a corruption clampdown by the Chinese authorities. As VIP growth slowed dramatically in March and turned negative in May, the Macau stocks faltered but the sell side maintained their ratings citing continued 30%+ Mass growth expectations for the remainder of 2014.

On June 13, 2014 we laid out our “Mass Decelerating” theme as the second point of our bear thesis for a slowdown in gaming revenues, just as the sell-side was defending the gaming operators on the thesis of “mass segment growth of >30% remains healthy”. Today, the sell-side has caught up to us with regard to the mass segment gaming revenue slowdown so the question is where do we go from here?

WHAT WE THINK WE KNOW – BACK TO THE MATH…

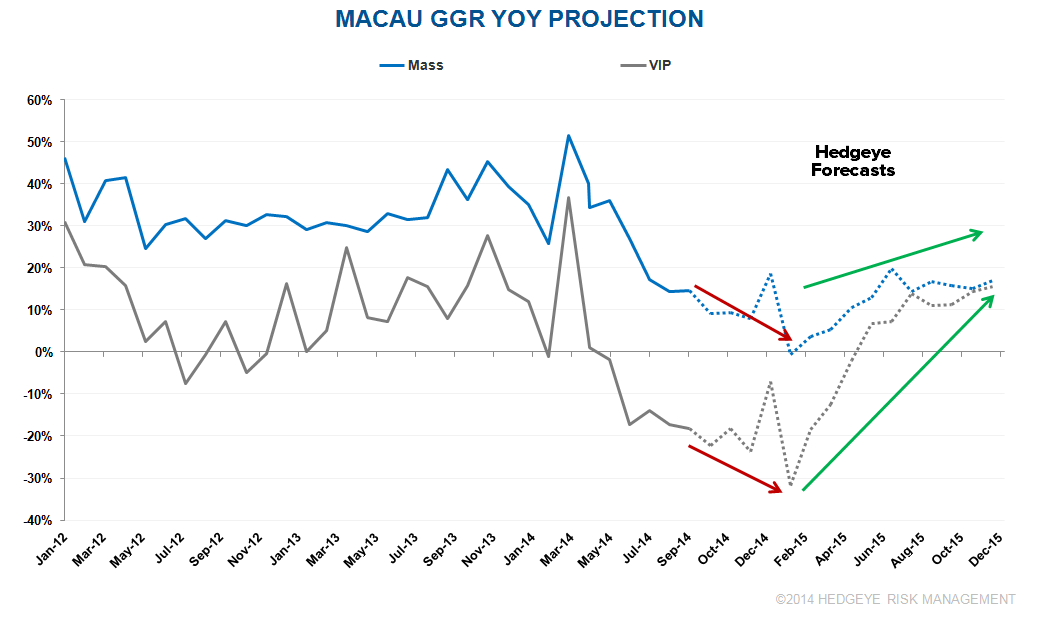

We apply a forecasting algorithm and process across all industries – gaming, lodging and cruise lines that incorporates both quantitative and qualitative factors. This process has allowed us to be ahead of various trend pivots including the recent mass revenue deceleration. Based on our model we believe Macau gaming revenue will trough sometime during Q1 2015.

THE FORECAST

Our forecasting algorithm is dynamic. Recall from our June 13, 2014 “Mass Deceleration” note, we forecasted Mass Segment revenues to trough in October and November 2014, at +18% on a year-over-year basis. At that time, we also forecasted VIP revenue growth of -5% to -8% during Q4 2014.

By comparison, today our forecasting model calls for Mass segment growth of +9% on a year-over-year basis during Q4 2014, nearly half the growth rate we forecast a mere three months ago – and a third of what the Street was projecting at the time. As can be seen in the following chart, we believe Macau gaming revenues will trough during Q1 2014, maybe during January or February as noted by the green arrows.

CONCLUSION

While we are looking for a pivot to become more constructive on the Macau gaming operators given our favorable long-term view, we are forced to reaffirm our negative view as we believe Q3 2014, Q4 2014 and FY 2015 earnings estimates are still too high. Our caveat to the negative sector outlook is Galaxy Entertainment where we are inclined to recommend long even today as a hedge. With its strong VIP business that seems to be less volatile than the market, Galaxy looks safer. Looking ahead, we still think the company will open Galaxy Macau Phase 2 before the May holidays – earlier than expected - thus have at least an eight month first mover advantage as Cotai supply explodes. Unlike the other concessionaries, Galaxy’s 2015 Street estimates look conservative.