“Mr. Bohannon, Do you want to build this railroad?”

-Senator Grant in the AMC T.V. show, “Hell on Wheels”

Similar to our office, I’m sure most of you don’t have much time to watch T.V., but every once in a while a great show comes around that is really hard to turn off. A popular one at Hedgeye as of late is AMC’s, “Hell on Wheels.”

The show is about the epic struggle to build a trans-continental railroad. Setting aside the obvious struggles of weather, dealing with Native tribes (who felt their treaties were being violated), and limited technology, the building of the transcontinental railroad also occurred at a time when the nation was healing itself from the Civil War. As a result many former Union and Confederate soldiers worked side-by-side on the railroad.

As Wikipedia describes it:

“The First Transcontinental Railroad (known originally as the "Pacific Railroad" and later as the "Overland Route") was a 1,907-mile (3,069 km) contiguous railroad line constructed between 1863 and 1869 across the western United States to connect the Pacific coast at San Francisco Bay with the existing Eastern U.S. rail network at Council Bluffs, Iowa, on the Missouri River.”

The epic struggle to connect the two sides of the continent took more than six years, but once it was completed dramatically changed the face of commerce in the United States.

Who knows, perhaps the iWatch will do the same?

Back to the Global Macro Grind...

In the global macro world, the epic struggle du jour seems to be related to Scottish independence. Simply, will the Scots decide to leave the United Kingdom, or not?

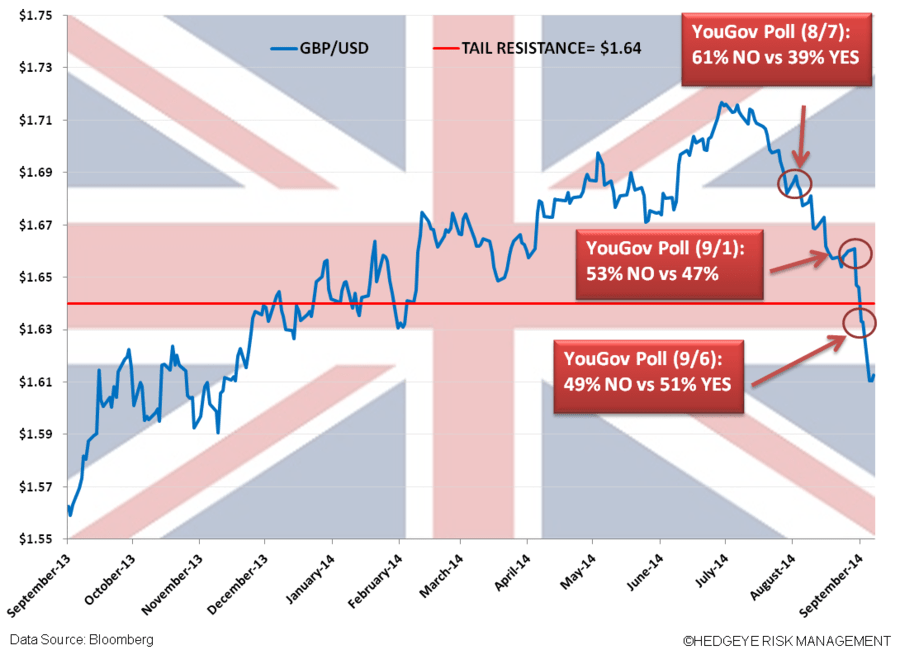

A few weeks ago, no one was even considering this as a potential global macro issue, but after a recent YouGov.Com poll that showed a slight majority of Scots voting Yes (51%) to independence versus No (49%), the British pound was sold dramatically and Scottish independence became a hot topic with the manic media.

So, will the Scots vote for independence on September 18th? If we rely strictly on the YouGov.com poll, it would seem there is a real chance of this occurring. Practically speaking, though, as we have written often in the past it is very unwise to rely strictly on one poll. In fact, there are a couple of key quantitative points that speak in contrast to the YouGov.com poll:

- First, the YouGov poll that showed a 2% edge for the Yes side was literally the second poll ever (of those polls approved by the British Polling Council) to show the Yes side ahead. The other Yes poll was taken by the Scottish National Party back in mid-2013;

- Second, the most recent poll aggregates (though some admittedly occurred before the most recent debate in which pro-independence leader Alex Salmond was widely judged to have won) still show a lead for the No vote outside the margin of error. Specifically, a poll aggregate issued by Strathclyde University on September 1st showed the No side ahead by 10 points and a poll aggregate from The Guardian on September 3rd showed a similar 10 point lead.

- Finally, the online betting website, Bet Fair, shows the market for Scottish Independence at more than 2:1 for No independence. (Incidentally, there have been almost $5 million pounds wagered on Bet Fair for this topic.)

In the Chart of the Day below, we show the impact that the series of YouGov.com polls have had on the British Pound. While certainly there are other factors at play, the increasingly pro-Independence polls have been a defined catalyst for aggressive selling of British Pounds.

Setting aside the polls and betting markets, the most notable reasons for Scotland to stay a part of Great Britain are related to the Scottish economy itself. Hedgeye’s European Analyst Matt Hedrick highlighted a number of major risks to the Scottish economy should the Scots pursue independence, including:

- Currency – UK politicians have stated that Scotland could not use Sterling. The country would have to issue its own currency

- Central Bank – until the formation of a central bank there is no backstop for sovereign debt

- Massive Capital Flight –investors could pull money out of Scottish banks en masse that would destabilize the financial system

- EU Membership – it’s unclear if an independent Scotland would be granted EU membership, which could have huge trade implications

- Regulation – uncertainty if banks would remain regulated under the UK regulatory authority? Tax and trade regulations also uncertain

- Economic Drag – prominent financial firms likely to move to London

- Budget – the Institute for Fiscal Studies pointsout that Scotland's Deficit could be 4.6% if independent. Low credit quality could negatively impact debt raises, and push the country's debt and deficit levels higher, a vicious cycle.

It is certainly possible, even if unlikely, that the most recent YouGov.com poll is the harbinger of Scottish Independence. But for this to be accurate it would fly in the face of all other polls, the betting markets, and really any semblance of rational analysis by the Scots related to their own economy. So our view continues to be that the No vote will prevail and the British Pound will rally accordingly.

That said, given the weak nature of the Scottish economy and the fact that 2 out of every 3 Scots are on some form of social welfare, over the long run a Great Britain without Scotland might actually be a stronger economy and certainly more healthy from a fiscal perspective. So on some level, perhaps the British Pound is in a win-win situation given its recent sell off. A No vote leads to a relief rally and a Yes votes leads currency traders to asses s United Kingdom’s much improved fiscal health without Scotland, which leads to a long term tail wind for the Pound.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.31-2.52%

SPX 1

RUT 1151-1171

Shanghai Comp 2

VIX 11.34-13.83

Brent 98.74-102.99

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research