TODAY’S S&P 500 SET-UP – September 9, 2014

As we look at today's setup for the S&P 500, the range is 25 points or 0.98% downside to 1982 and 0.27% upside to 2007.

SECTOR PERFORMANCE

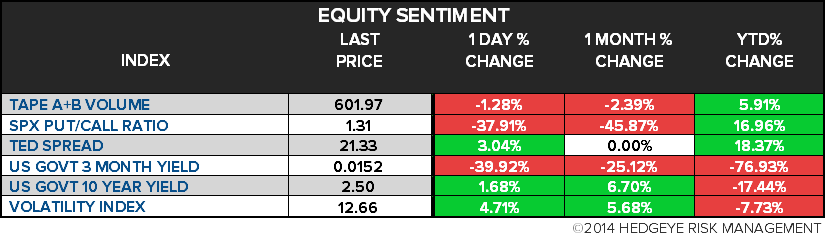

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.95 from 1.94

- VIX closed at 12.66 1 day percent change of 4.71%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Business Optimism, Aug., est. 96.0 (pr 95.7)

- 7:45am: ICSC weekly sales

- 8:55am: Redbook weekly sales

- 10am: JOLTs Job Openings, July, est. 4.7m (prior 4.671m)

- 10am: Fed’s Tarullo testifies to Senate Banking Cmte

- 11:30am: U.S. to sell $35b 4W bills

- 1pm: U.S. to sell $27b 3Y notes

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- Primaries in states including Del., Mass., N.H., R.I.

- President Obama, congressional leaders meet on foreign policy

- Sec. of State Kerry travels to Jordan, Saudi Arabia

- 8am: Blackstone President James speaks at Politico breakfast

- Confirmation hearings:

- 10am: NRLB nominee Sharon Block at Senate Health, Education and Labor Cmte

- 10am: NRC nominees Jeffrey Baran, Stephen Burns at Senate Environment and Public Works Cmte

- 10am: Fed Gov. Tarullo, FDIC Chair Gruenberg, Comptroller of Currency Curry, CFPB Dir. Cordray, SEC Chairwoman White, CFTC Chairman Massad at Sen. Banking Cmte on Wall St. reg. system

- 10am: VA Sec. McDonald testifies before Senate Veterans’ Affairs Cmte on investigation findings from Phoenix medical ctr

- 10am: IRS Commissioner Koskinen, CMS’s Slavitt at House Ways and Means Cmte on Affordable Care Act implementation status

- 10:30am: Senate Homeland Security Cmte hearing on federal programs for equipping state and local law enforcement

- 2pm: House Science panels hold hearing on oversight of Bakken petroleum

- U.S. ELECTION WRAP: Primaries Tomorrow; Brown, Lessig Battle

WHAT TO WATCH:

- Apple Event: Focus on Payments, Sapphire, Smartwatch

- McDonald’s Aug. comps seen declining for third month

- CFTC Said to Alert Justice Department of Criminal Rate Rigging

- U.S. Planning Tougher-Than-Basel Capital Rules, Tarullo Says

- U.K. industrial output exceeds forecast with 0.5% increase

- EU slows new Russia sanctions as Ukraine cease-fire gauged

- Rakuten to acquire Ebates in Japan’s biggest e-commerce deal

- JAB’s Jimmy Choo said near IPO to value shoemaker at $1b

- Telefonica Germany to raise $4.7b in stock for E-Plus

- America Movil to weigh joint bid for Telecom Italia unit

- ABB plans $4b buyback to return cash from disposals

- FX traders said to be surprised by narrow scope of BOE probe

- Trump Casinos plan bankruptcy in new blow to Atlantic City

- Home Depot confirms computer data systems have been breached

AM EARNS:

- Barnes & Noble (BKS) 8:30am, ($0.68)

- Burlington Stores (BURL) 7am, ($0.08)

- Francesca’s (FRAN) 7:30am, $0.26

- HD Supply (HDS) 6am, $0.47 - Preview

- John Wiley & Sons (JW/A) 8am, $0.53

- Leidos (LDOS) 6am, $0.62

PM EARNS:

- Krispy Kreme Doughnuts (KKD) 4:05pm, $0.16

- Oxford Industries (OXM) 4pm, $0.90

- Palo Alto Networks (PANW) 4:04pm, $0.11

- Peregrine Pharmaceuticals (PPHM) 4:01pm, ($0.06)

- Science Applications Intl (SAIC) 4:01pm, $0.68

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Fund Merchant Advances 16% as Crude Declines With Iron Ore

- Wheat Harvest Forecast Cut by Australia as Farms Need More Rain

- Commodities Drop to Lowest Since January as Dollar Cuts Demand

- Soy Yields Set for U.S. Record as Rains Fatten Pods: Commodities

- Brent Crude Near 16-Month Low as Ukraine Truce Holds; WTI Rises

- Lingering Ice This Year Delays Opening of Northern Sea Route

- OIL DAYBOOK: Crude Inventory Draw Fcast; Buzzard Said Shut Again

- Cold to Grip Northern U.S. Offers a Preview of Chills to Come

- Corn Extends Decline as U.S. Yields Seen Topping USDA Forecast

- Indonesia Palm Exports May Become Tax-Free as Prices Drop: Gapki

- Chinese Hot-Pots Stir Imports of Beef, Mutton: Chart of the Day

- Gold Is Little Changed Near Three-Month Low on Dollar to Ukraine

- India July Coal Imports Rise 9% Y/Y to 17.95 Mln Mt: Interocean

- Rubber Falls to 5-Year Low as China Supplies Compound Thai Glut

CURRENCIES

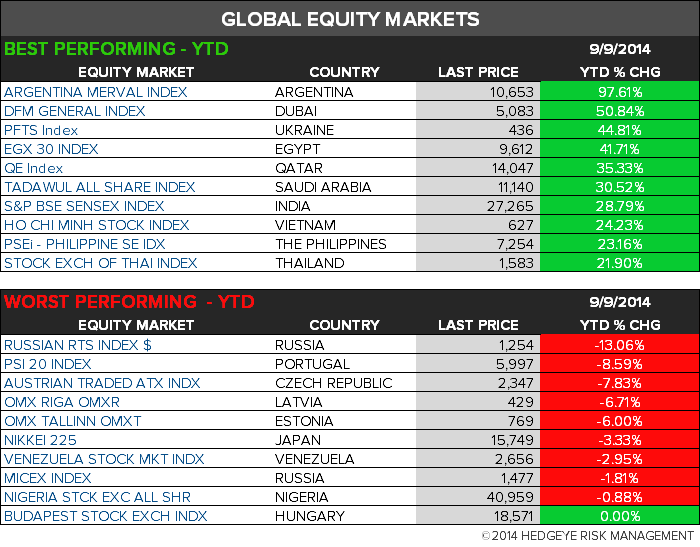

GLOBAL PERFORMANCE

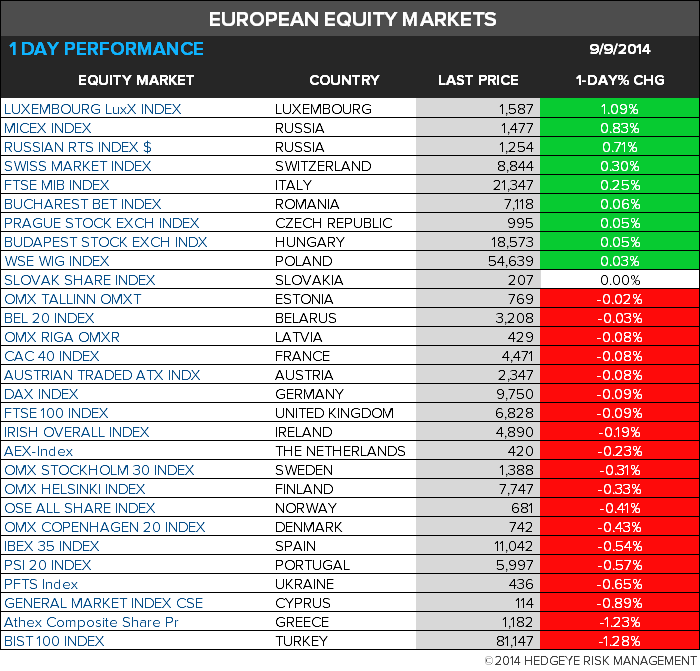

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team