TODAY’S S&P 500 SET-UP – September 8, 2014

As we look at today's setup for the S&P 500, the range is 15 points or 0.68% downside to 1994 and 0.06% upside to 2009.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.94 from 1.95

- VIX closed at 12.09 1 day percent change of -4.35%

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $26b 3M bills, $23b 6M bills

- 3pm: Consumer Credit, July, est. $17.0b (prior $17.255b)

GOVERNMENT:

- Senate, House return from summer recess

- 8:45am Treasury Sec. Lew speaks on tax reform

- 9:30am: HHS SEC. Burwell speaks to students, staff and faculty

- U.S. ELECTION WRAP: Roberts Shakes Up Campaign; Polls

- Obama’s immigration delay forced by Republican amnesty attacks

WHAT TO WATCH:

- Electrolux to acquire GE’s appliances unit for $3.3b

- FMC buys Cheminova for $1.8b as CEO tweaks break-up plan

- Facebook’s WhatsApp takeover faces fast EU review, Almunia says

- EU seeks to extract Google concessions to rescue antitrust pact

- CenturyLink said seeking to acquire Rackspace for cloud services

- Brent crude declines below $100 for first time since 2013

- Alibaba M&A spree to be questioned at Waldorf as IPO starts

- U.K. races to extend powers to Scots to blunt independence drive

- Scotland independence seen risking $23b of power projects

- Disney’s ‘Guardians’ leads slowest box office weekend since 2001

- EU Banks sidestepping bonus cap face crackdown from regulators

- German trade surplus at record as exports rise to all-time high

- GM to introduce hands-free driving in Cadillac model in 2016

- Schumer draft proposal on inversions could reach back 20 yrs

- Ryanair said poised for $11b purchase of Boeing Max Jets

- Rakuten in talks to buy U.S. online shopping operator Ebates

- U.S. expands air offensive to protect Iraqi dam from militants

- Ukrainian deaths test cease-fire as both sides report casualties

- U.S. gasoline falls to $3.4631 a gallon in Lundberg Survey

EARNINGS:

- Campbell Soup (CPB) 7am, $0.49

- Casey’s General Stores (CASY) 4pm, $1.25

- FuelCell Energy (FCEL) 4:10pm, ($0.03)

- Korn/Ferry Intl (KFY) 4:05pm, $0.40

- NCI Bldg Systems (NCS) 4:05pm, $0.09

- Triangle Petroleum (TPLM) 5:58pm, $0.15

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel Climbs to 9-Week High on Philippine Ore Supply Concerns

- Brent Crude Declines Below $100 for First Time in 14 Months

- Raw Sugar Rebounds From 7-Month Low While New York Cocoa Drops

- Gold Bulls Retreat as $1.6 Billion Erased From ETPs: Commodities

- Palm Oil Rises to Two-Week High as Exports May Expand on Waiver

- Gold Trades Little Changed Near 12-Week Low on U.S. to Ukraine

- Corn Declines as Traders Weigh Record U.S. Production Outlook

- Philippine House Body Approves Bill Banning Mineral Ore Exports

- Drillers Piling Up More Debt Than Oil Hunting Fortunes in Shale

- BNP Paribas Said to Curb Commodity-Trade Finance to Trafigura

- China Aluminum Exports Rise With Steel as Demand at Home Wanes

- Hedge Funds Reduce Bullish Gas Bets as Volatility Slides: Energy

- Clearinghouses Get CFTC Scrutiny So Solution Isn’t Problem

- China’s Import Drop Caused by Falling Commodity Prices, CBA Says

- Credit Suisse Sees Aluminum Rally Overdone Amid Plentiful Supply

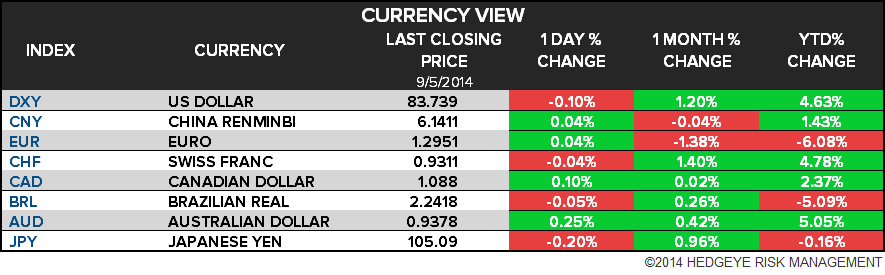

CURRENCIES

GLOBAL PERFORMANCE

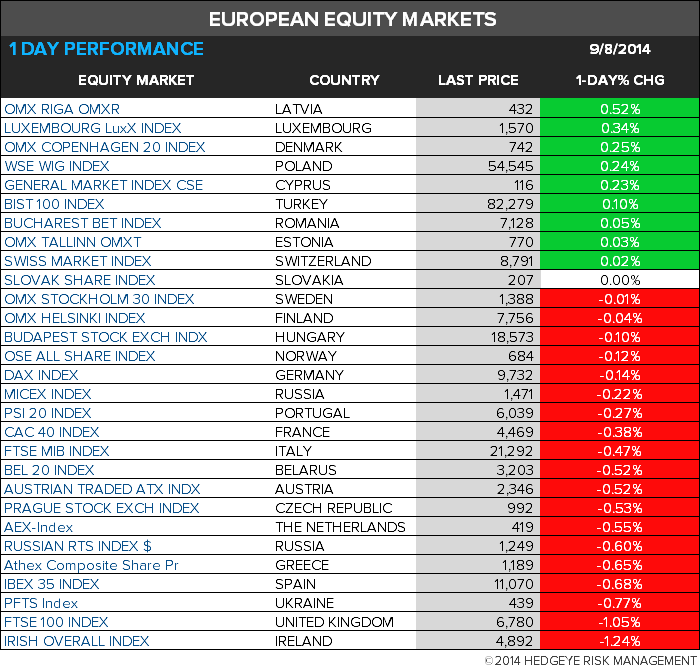

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team