EUR/USD falls on the announcement of rate cuts and credit easing programs. However, it’s not clear to us that this will necessarily be a catalyst to ignite European economic activity.

Investment Recommendations: short EUR/USD (FXE); Long GBP/USD (FXB)

Key Take-Aways from today’s ECB Meeting:

- ECB Head Mario Draghi surprised the market with rate cuts and the EUR/USD is trading sub $1.30 intraday. We remain short the cross via the etf FXE - quantit. broken TREND ($1.33) and TAIL ($1.34)

- Draghi’s policy outlook remains dovish and accommodative

- The market’s QE expectations remain elevated, however Draghi’s focus in today’s meeting (and perhaps to reset accelerated QE timing expectations following Jackson Hole) included announcing the ECB’s intention to purchase ABS (no formal size mentioned) and issuing a covered bond purchasing program (details on this program will be announced after the ECB’s next meeting on October 2nd)

- Draghi signaled he wants to return the ECB balance sheet to 2012 - the package to “lever up” now includes today’s policy program announcements, the previously announced TLTROs (scheduled for issuance in late September and December), and eventually QE?

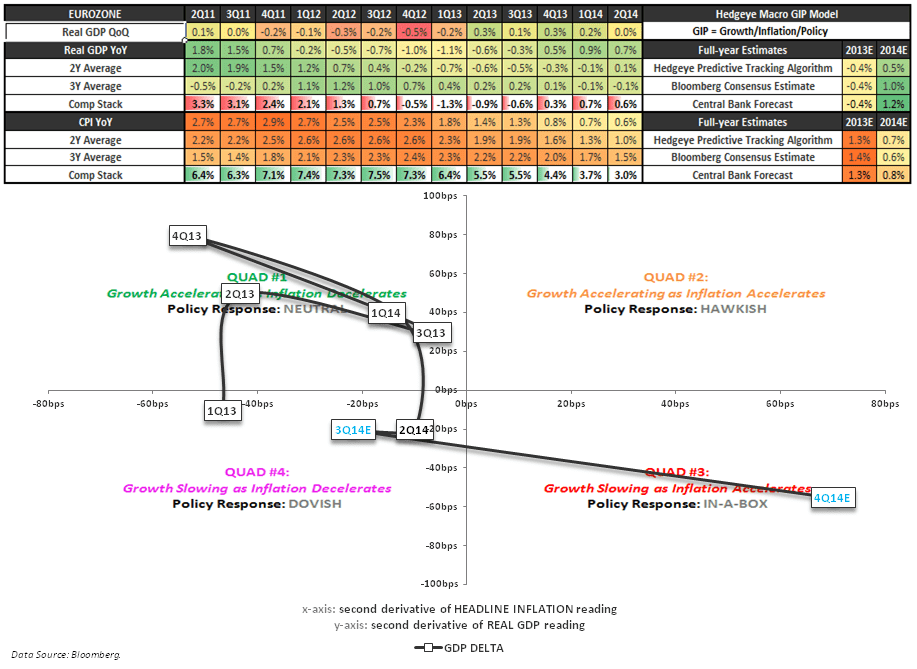

- ECB staff macroeconomic projections for September show downward revisions to the GDP and inflation outlook for the Eurozone (and in-line with our expectations and building on downward revision in the June outlook)

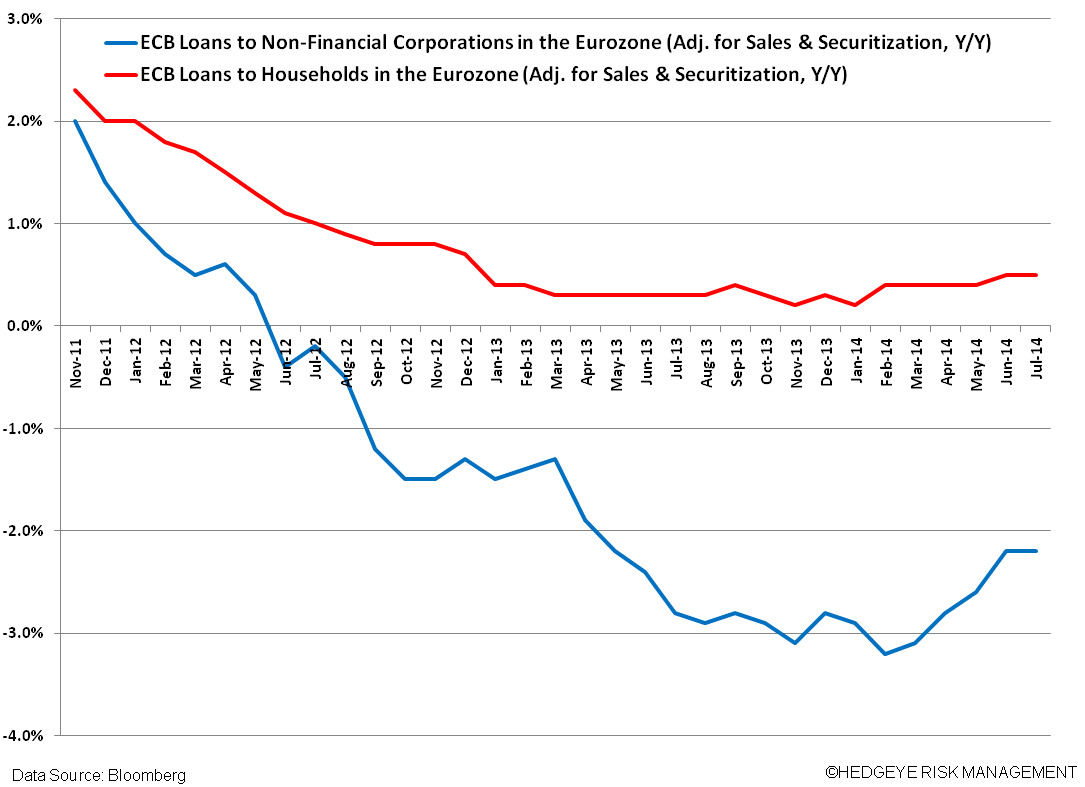

- Despite cutting main rates to near zero and deposit rates to negative first in June, the policy move has not lead to increased lending to businesses that are willing to invest in and grow the European economy. This will remain Europe’s great challenge over at least the medium term

What was delivered in cuts? The cuts to the main interest rate were largely unexpected by the market. In the Q&A Draghi attempted to anchor expectations that there would be no further cuts over the medium term (also not a big surprise since we’re already at or below the zero bound) to encourage participation in upcoming bond purchasing programs.

- Benchmark Rate: cut from 0.15% to 0.05% (0.15% est.)

- Marginal Lending Facility: cut from 0.40% to 0.30% (0.40% est.)

- Deposit Facility: cut from -0.10% to -0.20% (-0.10% est.)

The updated [SEPT] ECB Staff Macroeconomic Projections show further slowing to the outlook (vs JUN):

Growth Projections: +0.9% in 2014 vs +1.0% in June; +1.6% in 2015 vs +1.5% prior; +1.9% in 2016 vs +1.8% prior

Inflation Projections: +0.6% in 2014 vs +0.7% June; +1.1% in 2015 (in-line); +1.4% in 2016 (in-line)

Other Press Conference Mentions

- QE was discussed – some council members in favor of doing more, others doing less

- BlackRock has been hired by the ECB to help structure an ABS purchase program. No size was mentioned, and Draghi did not substantiate a leaked report earlier in the week that called for a program worth up to €500B

- Draghi underlined the drag from Unemployment across the region (currently at 11.5%) and highlighted the slack in the economy as a drag on ECB staff projections

- He stressed the importance of fiscal consolidation at the state level

Hedgeye’s Bearish Bias Remains

- Weeks and months of declining data across the region continue to fuel our bearish outlook on the Euro area

- While QE has proven to put a floor in equities in the past, QE is far from the elixir to inflect weak and declining fundamentals across the region. Witness Japan’s failed efforts with QE!

- While on the margin Draghi’s credit easing programs should help to encourage lending and therefore growth to the real economy, the failure of past LTROs to improve lending conditions are fresh in memory. This time may in fact not be different

- We reiterate that inflation (via currency debasement) is not growth, even if Draghi showers us with QE

- From here our propriety GIP model (growth, inflation and policy) for assessing economies suggests the Eurozone economy will land in the ugly quads #3 and #4 in 2H, representing growth slowing as inflation decelerates/accelerates.

Matthew Hedrick

Associate