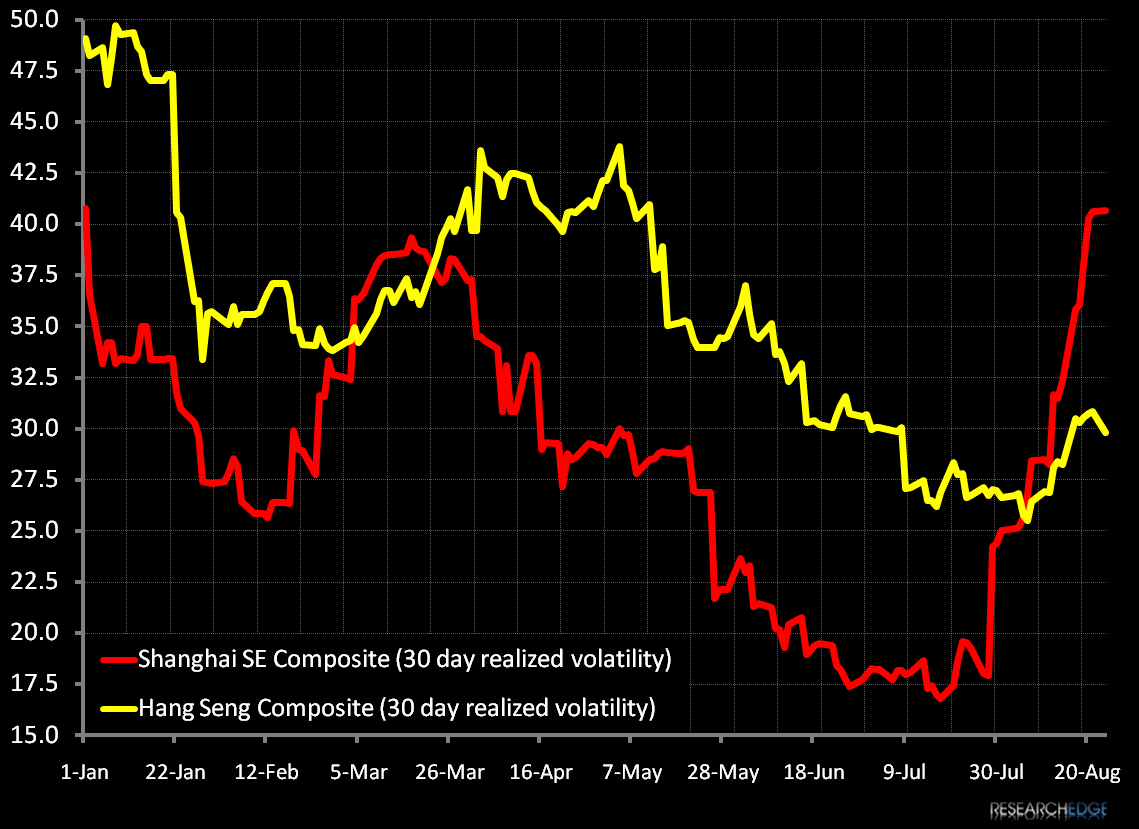

As we Follow tactical opportunities in the Chinese equity market, we have been tracking both the A shares listed domestically and H shares in Hong Kong separately in order to take maximum advantage of the divergent volatility in the two markets and share classes.

Currently the thirty day realized volatility for the Shanghai Composite is about 40 while the ten day realized volatility is about 54 versus 31 and 32 respectively for the Hang Seng. Our preferred vehicle for A share exposure, CAF, has a thirty day realized volatility level exceeding FXI by 5 points despite the fact that CAF contains exposure to a larger group of individual equities, and exceeding the 30DV of EWH by almost 10 points.

From our perspective, this difference in volatility has created a more tolerable trading range for Hang Seng listings in the intermediate term that allows us a greater degree of tactical confidence selecting entry and exit points for now. We reserve the option to harness the greater volatility represented by the Shanghai A shares to our advantage however, in order to capture larger swings when compelling entry points present themselves.

One part of our thesis on this divergence of volatility is that, structurally, the closed Shanghai markets have become capable of greater volatility in recent month as an increasingly significant percentage of volume there has been driven by inexperienced investors including a large retail component (who are using margin for the first time since the practice was introduced late last year) and that the proprietary investing groups at domestic banks. These leveraged traders have been the catalyst for recent spikes in short term lending rates as the market has digested a heavy IPO calendar. Certainly there has been a significant “hot money” factor driving the Shanghai market in recent months.

The decision to choose exposure via an A share vehicle, H share vehicle or even through ADRs becomes increasing less important as the underlying investment duration is extended. In other words, picking the right ETF or closed-end fund is critical for short term traders, but much less significant for longer term investors (provided that the divergence between the valuation metrics for each class are inside a band which is historically reasonable –valuation and not volatility becomes the compelling selection factor on a long tail basis). As we manage our portfolio tactically, in real time, we will continue to select our vehicles to maximize our performance to risk balance.

Andrew Barber

Director