Investment Recommendations: short France (EWQ), EUR/USD (FXE) and Eurozone equities (EZU); Long GBP/USD (FXB)

ECB head Mario Draghi has opened the gates for QE, but we think market expectations are over the skis on timing going into the September 4th meeting.

Quantitatively, major European equities remain broken TREND and we’re sticking to our playbook (we shorted France this week in Real-Time Alerts) as we see growth decelerating and inflation weak in the 2H. As Keith noted this morning, “we believe European Equity bulls traverse the thesis drift plains (begging for more QE), remember that Japan’s didn’t work.” And we reiterate, inflation is not growth, even if Draghi showers us with QE!

So the river cards market participants were talking about this week are now out:

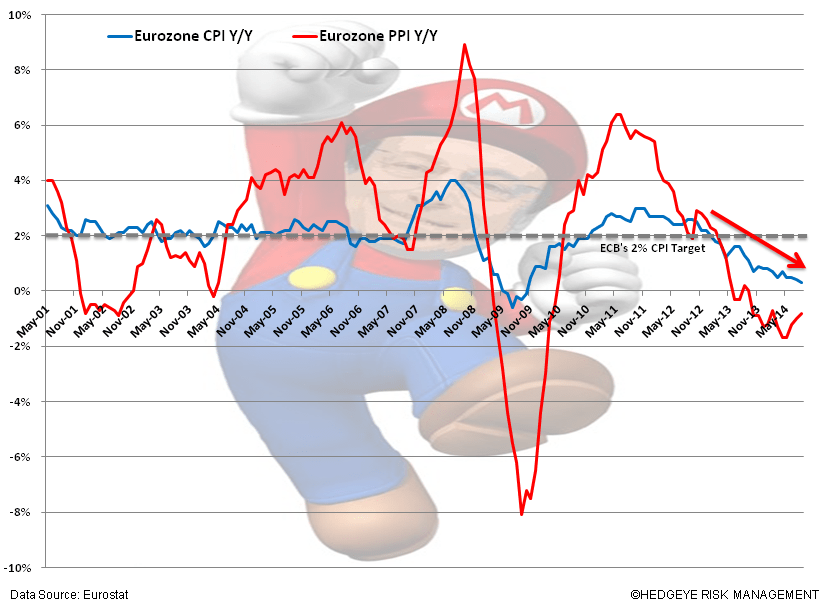

- Eurozone CPI fell to 0.3% Y/Y (4-yr low), a 10bps move lower – in line with our view and that of consensus (released today)

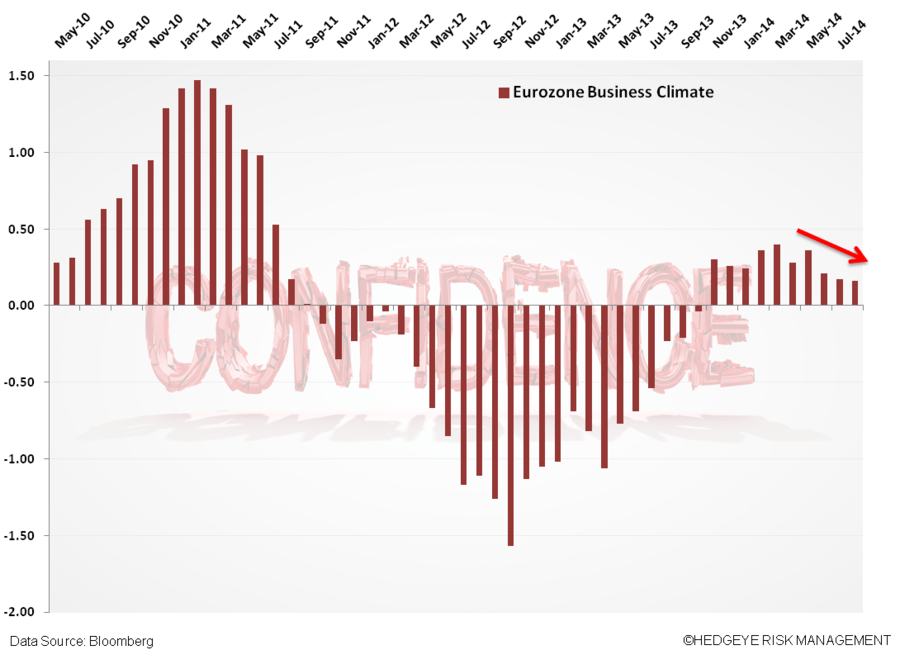

- European Confidence figures (Economic, Consumer, Industrial, Services, Business) turned lower in AUG versus the previous month and have weakened since ~ MAY 2014 – in line with our view and missing consensus (released yesterday)

As we made clear in notes this week (see Shorting France (EWQ); Draghi Trumps Yellen’s Dovishness – Sticking with the Playbook) we expected the decline in both CPI and confidence - it's clear and present in the recent data!

What’s our outlook? Conditions are not desperate enough to warrant QE in September, but expectations will rise.

Come September 4th we expect updated ECB staff projections to show downward revisions to growth and inflation outlooks, in line with the spate of weak Eurozone data over recent weeks and months. We expect that Draghi will “push” the growth and inflation prospects from TLTROs and QE-lite (ABS buying) programs in his public commentary (although we are not buying it to move the needle), and that the downward move in inflation for the August period is not enough (it’s not negative, yet) to accelerate a QE announcement to September.

Consider further, the TLTROs won’t be issued until September and December and he hasn’t experimented with QE-lite beyond a soft announcement. As the ECB has shown time and time again, it can flirt with “aid” packages for EXTENDED periods, to test expectations and further assess economic conditions (think of all the programs with 3 and 4 letter acronyms since the “crisis” got under way with Greece).

While we expect Draghi to leave QE in his back pocket through the September meeting, what we’re managing against is recent news that some sell-side economists, including JPMorgan, Deutsche Bank, Nomura, and Credit Suisse are now pricing in policy easing next week, according to the WSJ.

As the saying goes, expectations will always be the root of all heartache, and we’re sticking to our guns. For now our investment recommendations remain short France (EWQ), EUR/USD (FXE) and Eurozone equities (EZU); Long GBP/USD (FXB).

Enjoy the long holiday weekend!

Matthew Hedrick

Associate