TODAY’S S&P 500 SET-UP – August 18, 2014

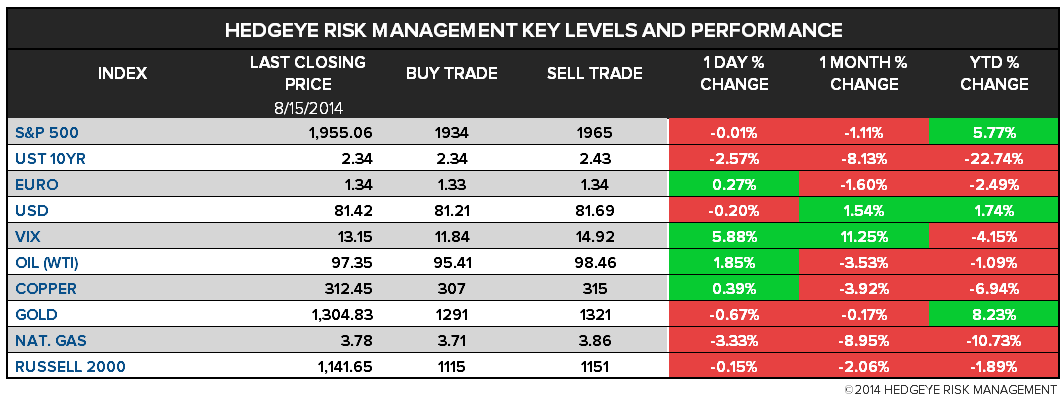

As we look at today's setup for the S&P 500, the range is 31 points or 1.08% downside to 1934 and 0.51% upside to 1965.

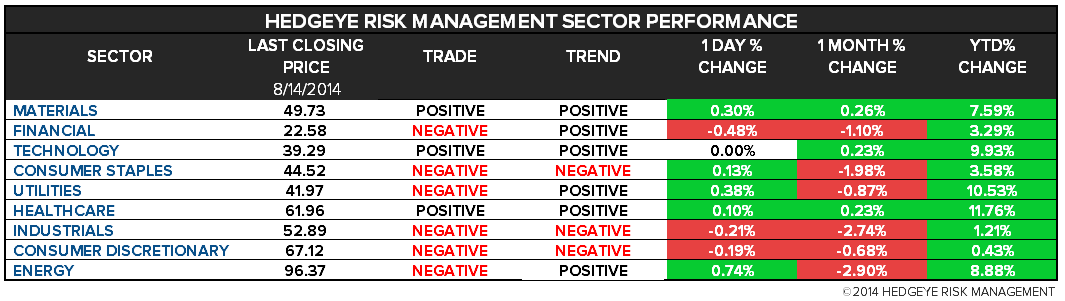

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.94 from 1.93

- VIX closed at 13.15 1 day percent change of 5.88%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: NAHB Housing Market Index, Aug., est. 53 (pr 53)

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $29b 3M bills, $25b 6M bills

- U.S. Rates Weekly Agenda

- FX Weekly Agenda

GOVERNMENT:

- Senate, House out on August recess

- Former House Majority Leader Eric Cantor, R-Va., said he will resign from Congress Aug. 18

- Former CFTC commissioner Scott O’Malia’s first day as chief executive of International Swaps and Derivatives Assn

WHAT TO WATCH:

- Valeant extends tender offer for Allergan until end of 2014

- Missouri Gov. Nixon dispatches National Guard to Ferguson

- Kurdish forces take control of Iraq’s largest dam

- Banks may lose Fed discount loans as part of living wills: FT

- Russia widens band on ruble trading vs USD-EUR basket to 9

- Google buys photo-analysis startup Jetpac; terms not disclosed

- BofAML said to be selected by Gulf Capital as main IPO adviser

- Wintergreen exits Berkshire Hathaway stake over Coke pay

- Fmr. SAC COO Kumin’s firm said to get $400m from Leucadia: WSJ

- Tesoro refinery explosion case closes; no charges brought

- Boeing 747 hull said to have been punctured in July collision

- Twitter to meet Turkish govt Aug. 25 on taxes, grievences: HT

- IBM says CFIUS approves x86-based server unit sale to Lenovo

- Target may keep some stores open until midnight: WSJ

- Judge in GM class-action ignition switch case names counsel

- U.S. banks see Ireland alternative in case of U.K. move: FT

- Teenage Mutant Ninja Turtles top box office for second wkend

- China home prices fall in majority of cities on weak demand

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Materials, Media/Ent, Real Estate

- North American M&A Agenda

- Jackson Hole, Yellen, Draghi, Fed Minutes: Wk Ahead Aug. 16-23

PM EARNS:

- Urban Outfitters (URBN) 4pm, $0.48

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Palladium Advances to 13-Year High in New York as Gold Declines

- Nickel Drops as Chinese House-Price Slump Fuels Slowdown Concern

- Robusta Coffee Drops Amid Rains in Vietnam; White Sugar Falls

- Hedge Funds Extend Longest Soy Bear Run Since 2006: Commodities

- Shanghai Gold Exchange Said to Plan FTZ Contract for September

- Refinery Breakdowns Boost Gasoline as Labor Day Nears: Energy

- OPEC Oil Call May Increase on Economic Growth, Rising Prices

- Oil Mkt Struggles to Find Buyers to Take Physical Delivery: MS

- European Naphtha Shipments to Asia Rise to 12 Cargoes in Aug.

- Copper Charges in China Seen Rising to $120/t as Freeport Ships

- Potential $60 Billion Mine in Play as Rio Reviews Its Stake

- Palm Oil Declines to Lowest Level in Five Years on Weak Exports

- China Plan to Cut Wholesale Power Price May Help Coal Producers

- Steel Rebar Declines on China Home Prices as Ore at Record Low

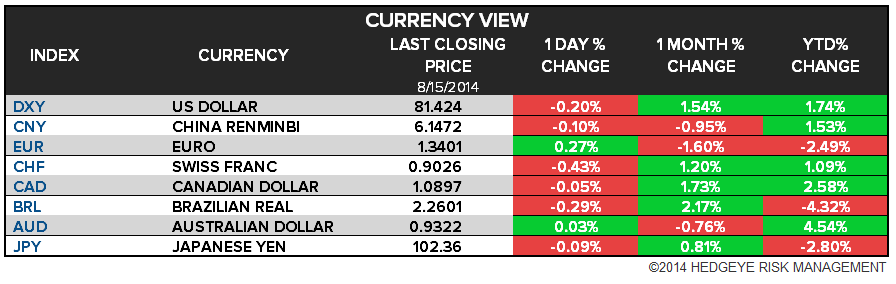

CURRENCIES

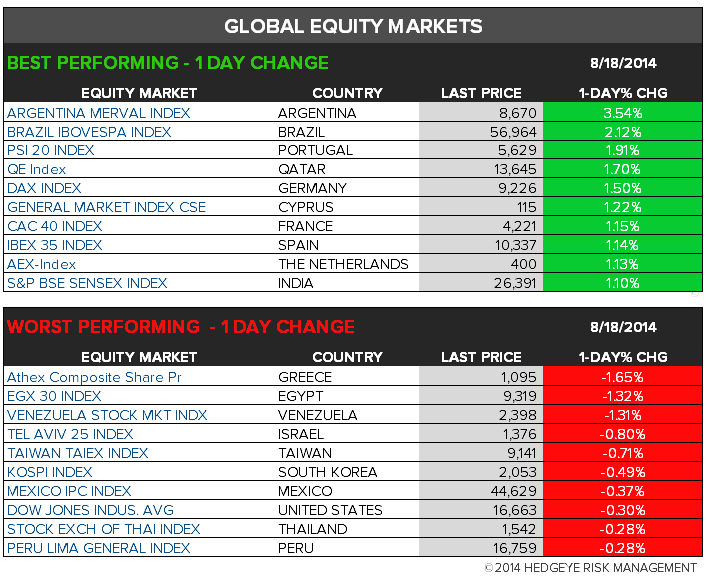

GLOBAL PERFORMANCE

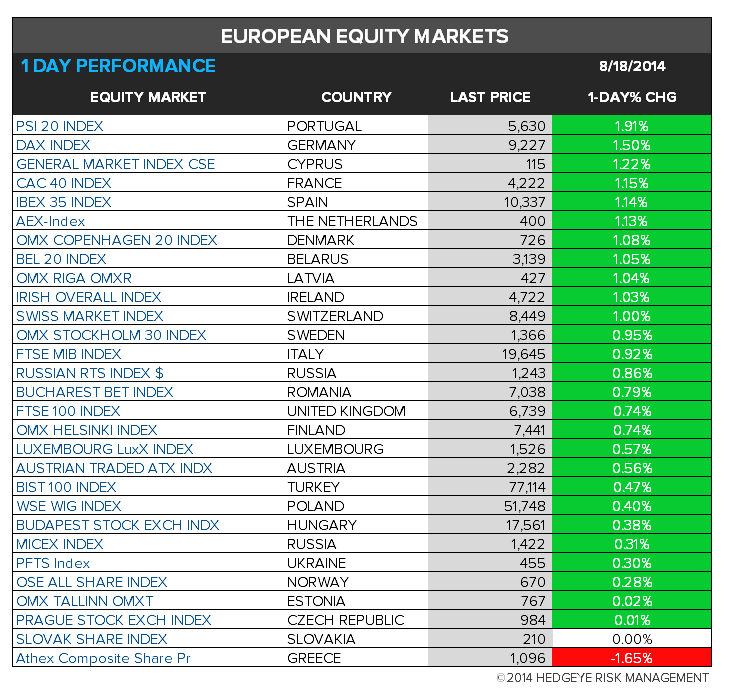

EUROPEAN MARKETS

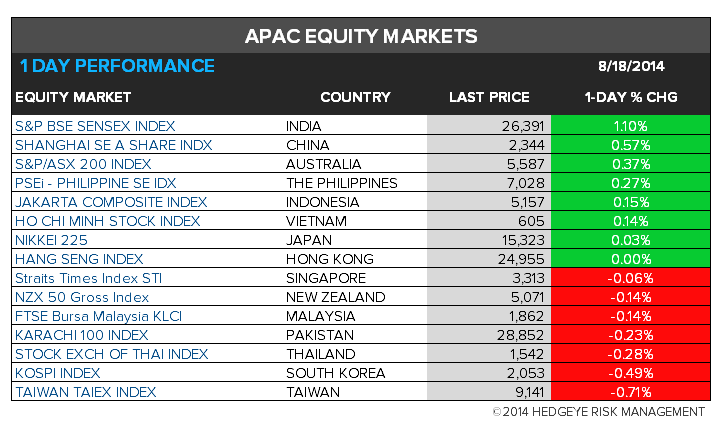

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team