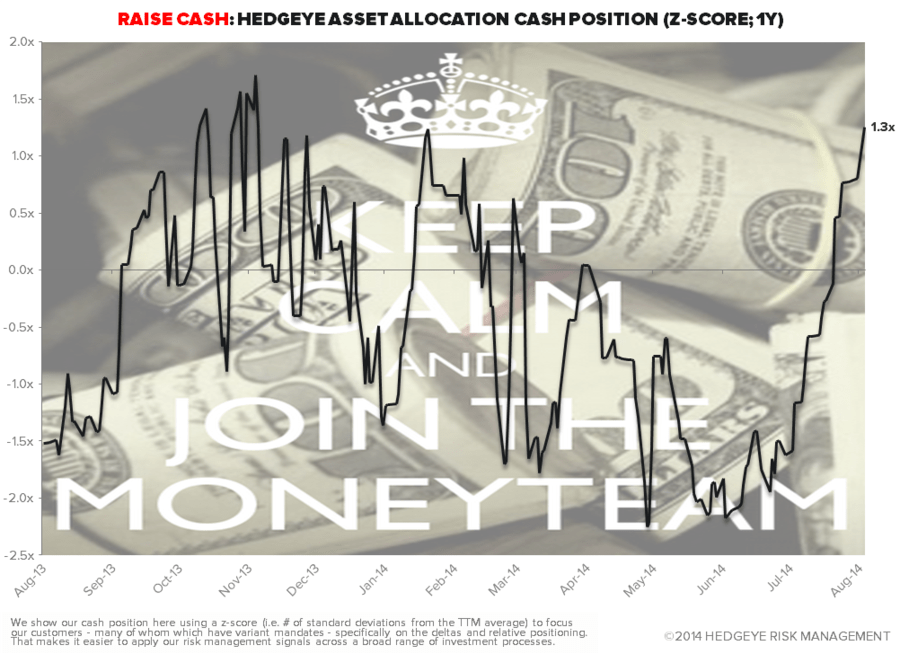

At 52% Cash in the Hedgeye Asset Allocation model this morning, that’s the highest Cash position we have had in at least 2 years.

At 52% Cash in the Hedgeye Asset Allocation model this morning, that’s the highest Cash position we have had in at least 2 years.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.