This note was originally published at 8am on August 01, 2014 for Hedgeye subscribers.

“The future is not a point – a single scenario that we must predict. It is a range.”

-Chip & Dan Heath

In Chapter 10 of Decisive, “Prepare To Be Wrong”, the Heath boys nail it with that risk management thought. Translating it into Hedgeye-speak: market tops and bottoms are processes, not points.

Price, volume, and volatility are all dynamic but measurable beasts. You don’t have to be a rocket scientist to be able to visualize their patterns. All you need is a process to score them. It’s rarely an absolute price level that matters – it’s almost always about its rate of change.

Measuring rate of change (slope of the line) won’t help you much unless you contextualize it across multiple durations. We strongly advise that you stand outside your western academic confirmation biases and consider rates of change across multiple factors as well.

Back to the Global Macro Grind…

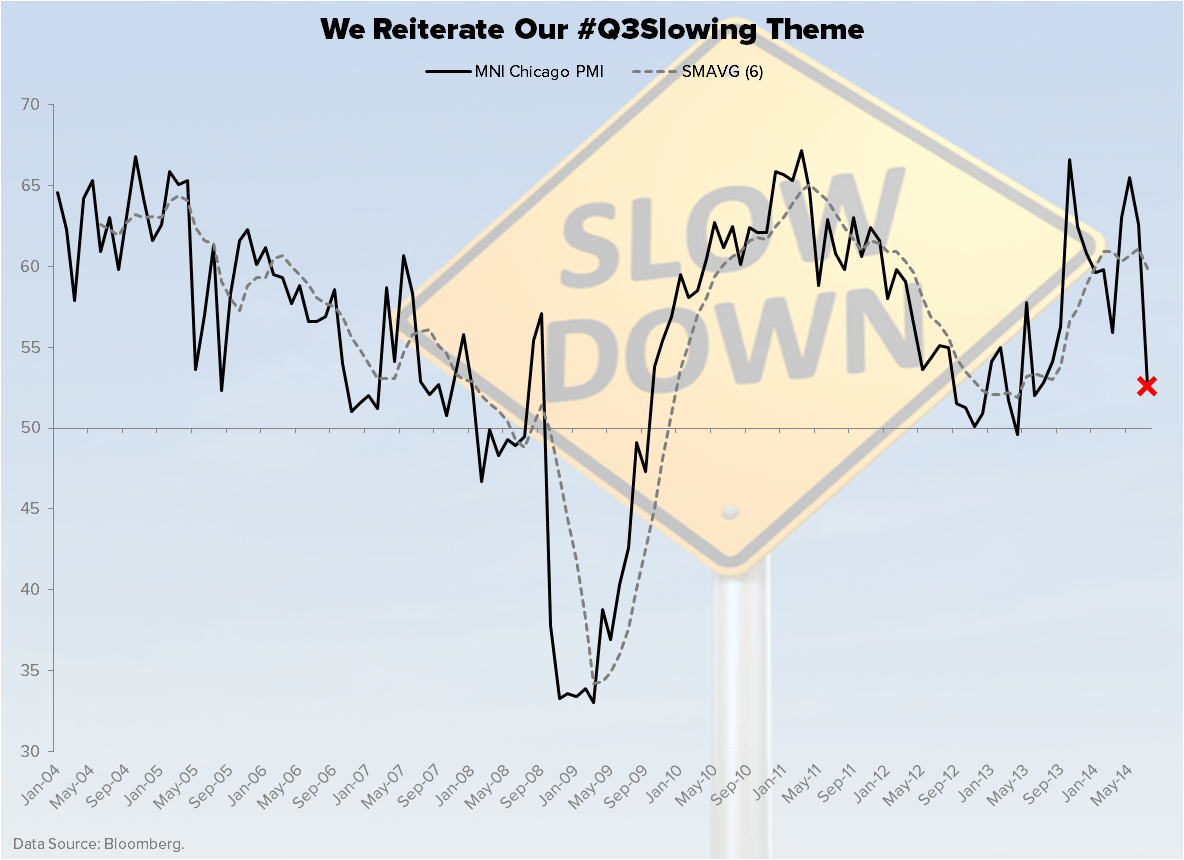

Multi-factor, multi-duration macro. Yep. That’s how we roll. And after a +64% rip in front-month US stock market volatility (since July 7th) we’re not only going to stick with that process this morning, but also remind you that it’s not Q2. It’s Q3.

They can blame Argentina or my cousin’s neighbor’s brother for yesterday’s levered-long-beta-belly-flop in US Equities (worst down day of the year), but they can’t change that the USA’s PMI print got powdered (rate of change) down to 52.6 in JULY vs 62.6 in JUNE.

They may very well have built inventories into the USA growth-hope narrative in Q2, but in Q3 the PMI (purchasing manager index) looks almost identical to the Industrial Stocks (XLI). Since US Equity volatility bottomed late June, early July:

- Industrials (XLI) are down -7.2%

- And the Russell 2000 (IWM) is down, well, -7.2%

Forget our #VolatilityAsymmetry Q3 Macro Theme. How symmetric is that?

More importantly, who gets what it’s been signaling? Who is writing about an early-cycle slowdown? These rates of change didn’t start yesterday. Depending on which factor in the US economy you have been measuring, they have been in motion now for 7 months!

What are the early-cycle slowdown sectors of the US stock market?

- Housing (ITB)

- Consumer Discretionary (XLY)

- Industrials (XLI)

All three of these early-cycle sectors are down now for 2014.

“So”, if god called you and said ‘hey, here’s my survey of the US economy’:

- Long-term Bond Yields are down -15% YTD (10yr UST Yield)

- The Russell 2000 is down -3.7% YTD… and

- Housing (ITB) is down -10.5% YTD

What would you say back if you were bullish on something like +3-4% US GDP growth? I think Bill Ackman would say, “my bad.”

I’m not trying to be snarky about this. I’m actually trying to drive my Scottish-Canadian flag right into the front-line of this ongoing culture war I’ve been fighting vs. #OldWall since we started the firm in 2008. You know, and wiggle the Braveheart kilt at them.

Let’s have some bull/bear battles already. At some point, someone out there in Consensus Macro land needs to man-up and just say ‘hey, I’ve missed calling every early-cycle slowdown since 1999, and I’m tired of this Canadian-mutt doing the rate of change thing.’

Now many would argue that consensus economists and strategists in Washington and on Wall Street would rather all be wrong together than wrong all on their own (#JobSecurity). But I think our profession is better than that.

I’m betting someone who is a lot smarter than me is going to change what they are doing and fight me, Red-White-And-Blue style! In every profession in America, there’s always been a progressive rate of change in that too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.43-2.59%

SPX 1924-1965

RUT 1111-1145

DAX 9206-9613

VIX 13.12-17.91

Brent Oil 105.54-108.79

Gold 1271-1305

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer