TODAY’S S&P 500 SET-UP – August 15, 2014

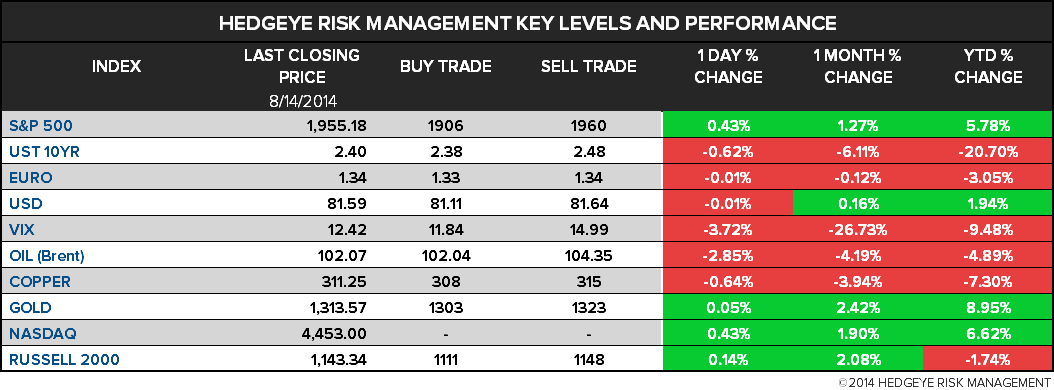

As we look at today's setup for the S&P 500, the range is 54 points or 2.52% downside to 1906 and 0.25% upside to 1960.

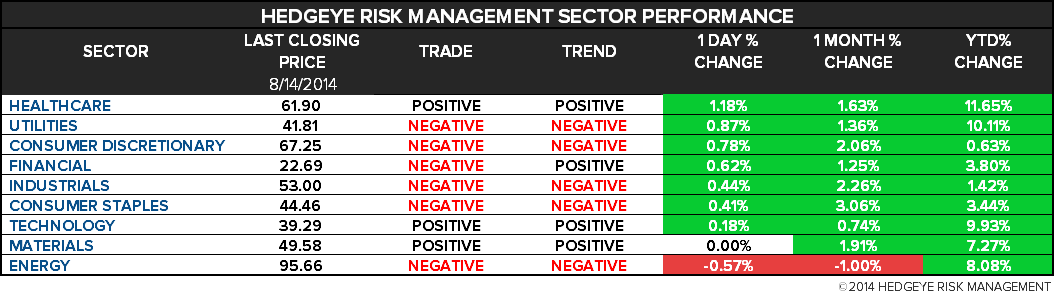

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.98 from 1.99

- VIX closed at 12.42 1 day percent change of -3.72%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, Aug., est. 20 (prior 25.6)

- 8:30am: PPI Final Demand m/m, July, est. 0.1% (prior 0.4%)

- 9am: Net Long-term TIC Flows, June (prior $19.4b)

- 9:15am: Ind. Production m/m, July, est. 0.3% (prior 0.2%)

- 9:55am: UofMich Confidence, Aug. prelim, est. 82.5 (pr 81.8)

- 10:45am: Fed’s Kocherlakota speaks in Brainerd, Minn.

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Senate, House on Aug. recess; President Obama on vacation on Martha’s Vineyard

- 2pm: Foreign Policy Initiative conf. call on “Iraq in Turmoil,” with Michael Pregent, adjunct lecturer, Natl Defense University’s College of Intl Security Affairs

- U.S. ELECTION WRAP: Hawaii Primary Timeline in Flux; Debates

WHAT TO WATCH:

- Coca-Cola to gain Monster Beverage stake in $2.15b deal

- Berkshire redoes pay-TV bets with Charter stake, less DirecTV

- Billionaire Paulson keeps stake in world’s biggest gold ETP

- Icahn takes new activist position in Gannett, backs split plan

- John Paulson bets on Allergan, takes 5.6m shr stake

- J.C. Penney’s loss narrows as return to roots boosts sales

- Supervalu says hackers may have stolen U.S. shoppers’ card data

- Citigroup, JPM, others report July credit-card delinquencies

- ZF talks to buy TRW Automotive said to hinge on Bosch JV exit

- Chiquita sticks to Fyffes deal as Cutrale-Safra offer rejected

- Applied Materials forecasts sales that may top analyst ests.

- BlackBerry shipments rise from prior quarter under Chen’s watch

- GM plans top-range Cadillac car, redesigned SRX for next year

- Maliki resigns as Iraqi prime minister to make way for Abadi

- U.K. keeps momentum in second quarter with 0.8% GDP growth

- BOJ officials said to mull cutting growth forecast for 2014

- Hong Kong cuts 2014 growth target after unexpected contraction

- BHP eyes Billiton assets split to focus on iron ore to coal

- Impala Platinum sees profit falling as much as 75% after strike

- Ackman’s Pershing Square sues U.S. over Fannie, Freddie bailout

- Samsung buys startup SmartThings to move into smart homes

- U.S. video-game industry sales rise 16% on console spending

- Ebola outbreak in W. Africa worse than cases suggest, WHO says

- Jackson Hole, Yellen, Draghi, Fed Minutes: Wk Ahead Aug. 16-23

EARNINGS:

- Estee Lauder (EL) 7:30am, $0.55

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Billionaire Paulson Keeps Stake in Top Gold Fund as Price Climbs

- WTI Oil Set for Weekly Loss With Brent on Weaker Demand Outlook

- Brazil Turns Aluminum Importer as Power Costs Surge: Commodities

- Copper Rises Before U.S. Factory Output Data as Stockpiles Drop

- London Silver Price Set at $19.86 an Ounce on First Day

- Soybeans Drop as Rain Seen Helping Crop; Corn Climbs With Wheat

- ABN Amro Adds Heads of Metals, Energy to Asia Commodities Team

- Panama Says a $5.3 Billion Canal Expansion May Not Be Big Enough

- Libyan Gas Flows to Italy Climb as Russian Supplies Threatened

- Traders Lured to Bet on Power Overloads Worth Billions: Energy

- Oil Sands Profits Most at Risk From Falling Crude Price: Study

- BHP Eyes Billiton Assets Split to Focus on Iron Ore to Coal

- Copper Traders Bearish on Slowing Economies to Demand Weakness

- HSBC, Mitsui, ScotiaMocatta to Participate in New Silver Price

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

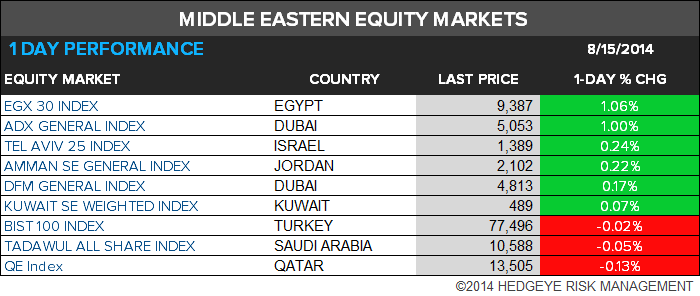

MIDDLE EAST

The Hedgeye Macro Team