Another tough quarter for Singapore gaming with a resumption of growth elusive.

THE CALL TO ACTION

Q2 2014 was another disappointing quarter for the Singapore casinos with declining hold adjusted GGR and EBITDA. Singapore Macro isn’t helping nor are a few extraneous issues such as the Malaysian airplane disappearance. Unfortunately, the outlook looks more challenging – at least through the end of 2015. Growth is proving elusive and we wonder if Singapore will ever be a growth market again given the casino supply growth throughout Asia. In conclusion, the lack of Singapore growth could continue to provide an overhang on the stock of LVS and obviously, Genting Singapore.

THE METRICS

GGR

- Higher MBS hold boosted Singapore gross gaming revenues 5% YoY in Q2 2014 to S$1.93 billion. Also, both MBS and RWS had easy Q2 hold comps - 2.5% and 2.6%, respectively. On a QoQ basis, Singapore GGR declined 12% in Q2 2014.

- MBS GGR share is in-line with 3 year average.

- Adjusting for hold (based on average since inception for both properties) for both periods, GGR fell for the 3rd consecutive quarter, -5% YoY or S$1.83 billion. (MBS: -10%, RWS: flat)

VIP

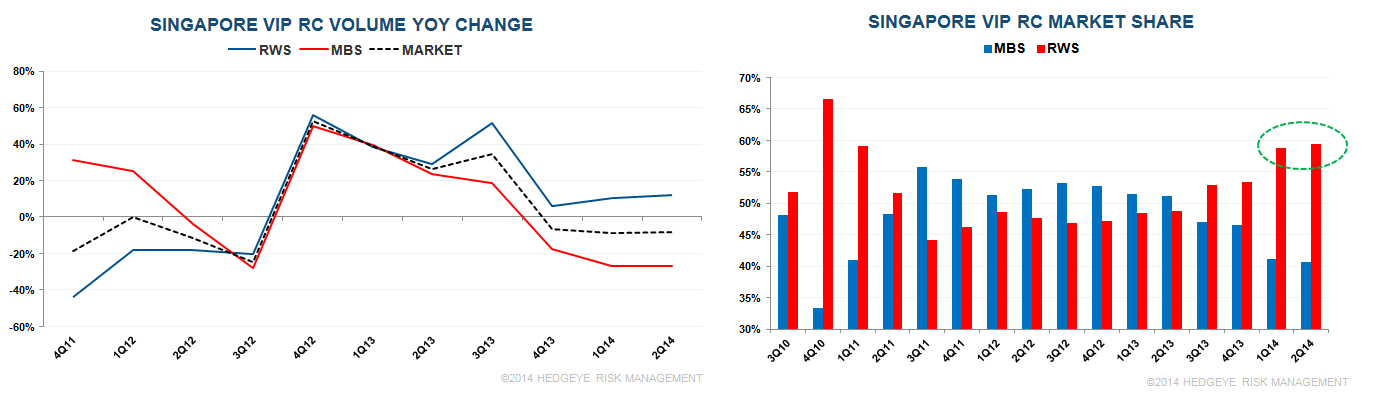

- VIP Rolling chip volume tumbled for the 3rd consecutive month, falling 8% to S$32.23 billion.

- MBS continues to lag on VIP volume share - its 40% share is the lowest since Q4 2010. Its S$13 billion is the lowest quarterly VIP volume since Q1 2011.

- Q2 2014 market hold was 3.13%

- Market historical hold since inception was 2.88%

MASS REVENUE

- Mass revenue dropped another 3% YoY in Q2 2014, the 4th consecutive quarterly decline with volumes down 9% YoY.

- Thanks to its success on the slots/ETGs, MBS holds a commanding 58% mass (including slots) win share.

NON-GAMING

- Net non-gaming revenue fell 5% YoY in Q2 2014 the 3rd consecutive quarterly decline

- Genting Q2 2014 REVPAR declined 3% compared with a 1% decline in the upscale hotel comp set. Q2 is seasonally a weak quarter.

- MBS Q2 2014 REVPAR rose 8% YoY compared with 5% growth in the luxury hotel comp set.

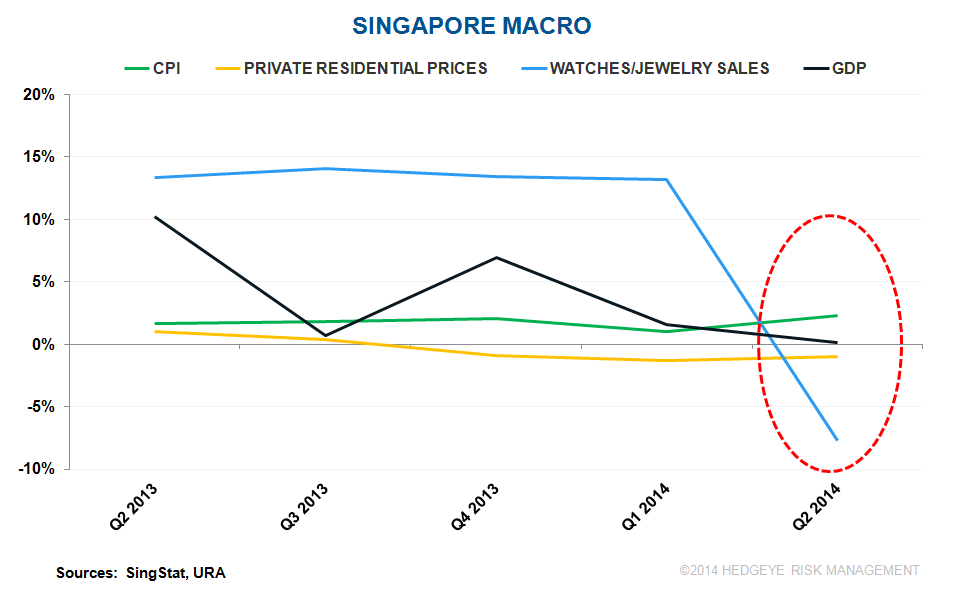

MACRO

- Revisions on several Singapore macro data points in the past few weeks continue to show a weak macro picture

OUTLOOK

- Comps will continue to be difficult on the VIP side in Q3 2014. VIP win and rolling chip volume grew 72% and 34%, respectively in Q3 2013.

- LVS and Genting both expressed caution with extending credit to VIPs. Genting’s large bad debt expense in Q2 2014 indicates a shaky lending environment that will lead to greater prudence in the coming quarters.

- Mass play is also struggling. Even with more mass tables and greater investment in the premium mass segment from LVS, this segment has been declining to stagnant since Q1 2012. Singapore visitation has shrunk this year, although Genting mentioned there has been a greater mix of higher spend visitors. With many headwinds (macro, currency, travel fears stemming from the airline/ferry disasters), it would be tough for the mass market to achieve growth in 2H 2014.