Investment Recommendations: short Eurozone equities (EZU) and EUR/USD (FXE)

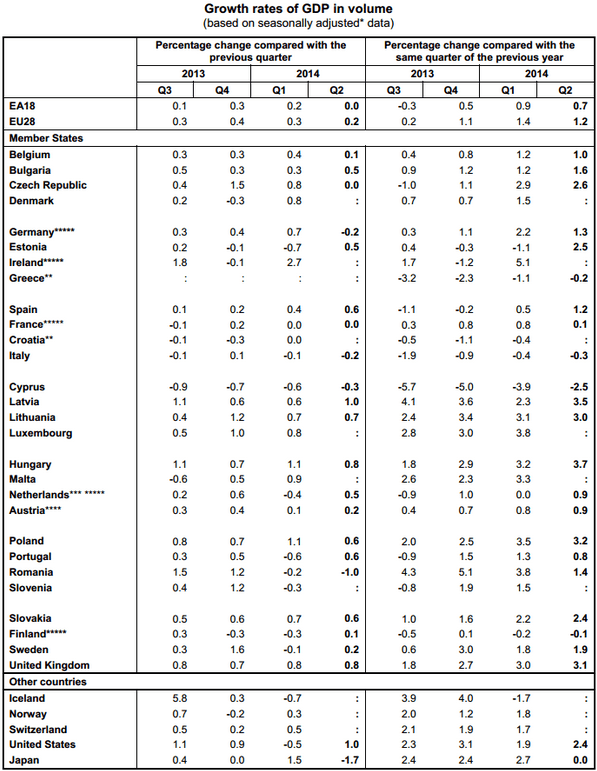

Europe has been on the sell side in our current macro themes deck and that position is seeing the benefit of more slowing economic data from Europe this morning. Beyond the EU region stalling to 0.0% sequentially and +0.7% Y/Y, Germany saw a significant drop Q/Q (from +0.8% to -0.2%) and France’s slowing led the government to cut its GDP forecast in half (again) to 0.5% for 2014 (and it will likely cause the country to miss its deficit target of 4%). Ouch!

This is also the first time both the USA and Europe have slowed (in rate of change terms) at the same time since 2011. German GDP has now fallen to the annualized rate of change the USA had in 1H of 2014 (+0.8-0.9%).

Our quantitative lines of support have been broken across European equities for 1.5 months (the DAX, CAC, and MIB index all remain bearish TREND signals) and our propriety GIP model (growth, inflation and policy) for assessing economies suggests the Eurozone economy will land in the ugly quad #3 in 2H, representing growth slowing as inflation accelerates.

Beyond the economic growth signals, our outlook for asset classes in the Eurozone remains focused on the actions of ECB President Mario Draghi. While Final CPI for July (released today) was unchanged at 0.4% Y/Y, we believe there’s a risk to the downside that we expect will force Draghi’s hand and accelerate expectations that the Bank launches a full scale QE program into year-end.

Currently we see the Bank on hold (it’s August and vacation time after all), however come Fall he may begin QE-lite purchases (via ABS), and as expectations mount of a recession in the Eurozone, full blown QE could be the last saving grace to stoke growth and inflation.

Should expectations heighten around a QE program while economic data continues to slow, we may well be altering our view across the region. For now, we recommend short Eurozone equities (EZU) and EUR/USD (FXE).

Here are the preliminary Q2 GDP results for the Eurozone, Germany, and France:

Eurozone 0.0% Q/Q (0.1% est.) vs. 0.2% prior

Eurozone 0.7% Y/Y (0.7% est.) vs. 0.9% prior

Germany -0.2% Q/Q (-0.1% est.) vs. 0.8% prior

Germany 1.3% Y/Y (1.4% est.) vs. 2.2% prior

France 0.0% Q/Q (0.1% est.) vs. 0.0% prior

France 0.1% Y/Y (0.3% est.) vs. 0.7% prior (0.8% revised)

For Germany, this is the first sequential contraction since 2012, and comes as no great surprise given the downturn in German Industrial production, Factory Orders, and ZEW expectation numbers released over the last two weeks.

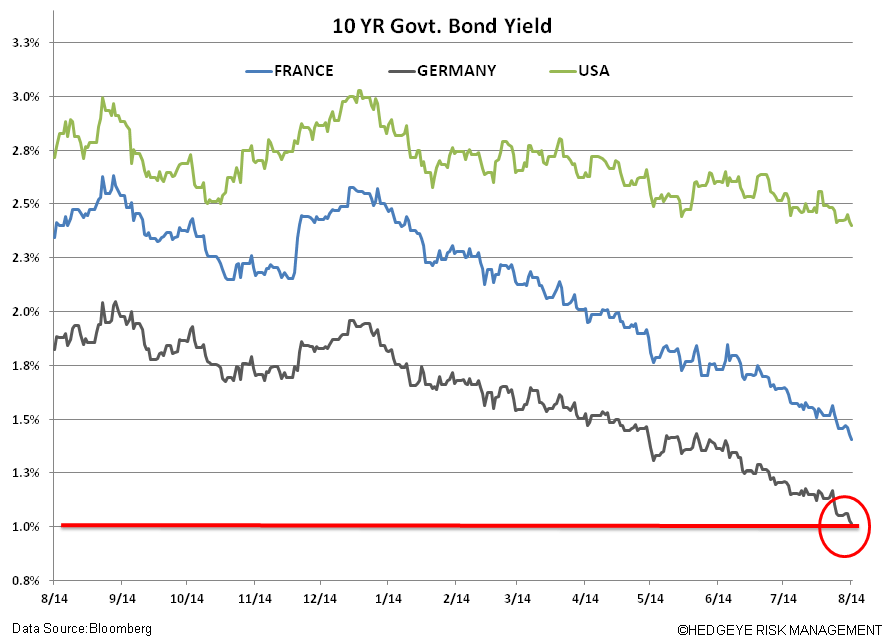

As my colleague Daryl Jones wrote in today's Early Look, "given this, it’s no surprise then that the German Bund hit a record low of 1.0% this morning and has been front running this slow down. Clearly, low reported inflation is leaving the door open (some might say wide open!) for incremental easing in Europe (a point the German bund market is front running)." Indeed.

Here are the region’s Q2 GDP results according to Eurostat:

Matthew Hedrick

Associate