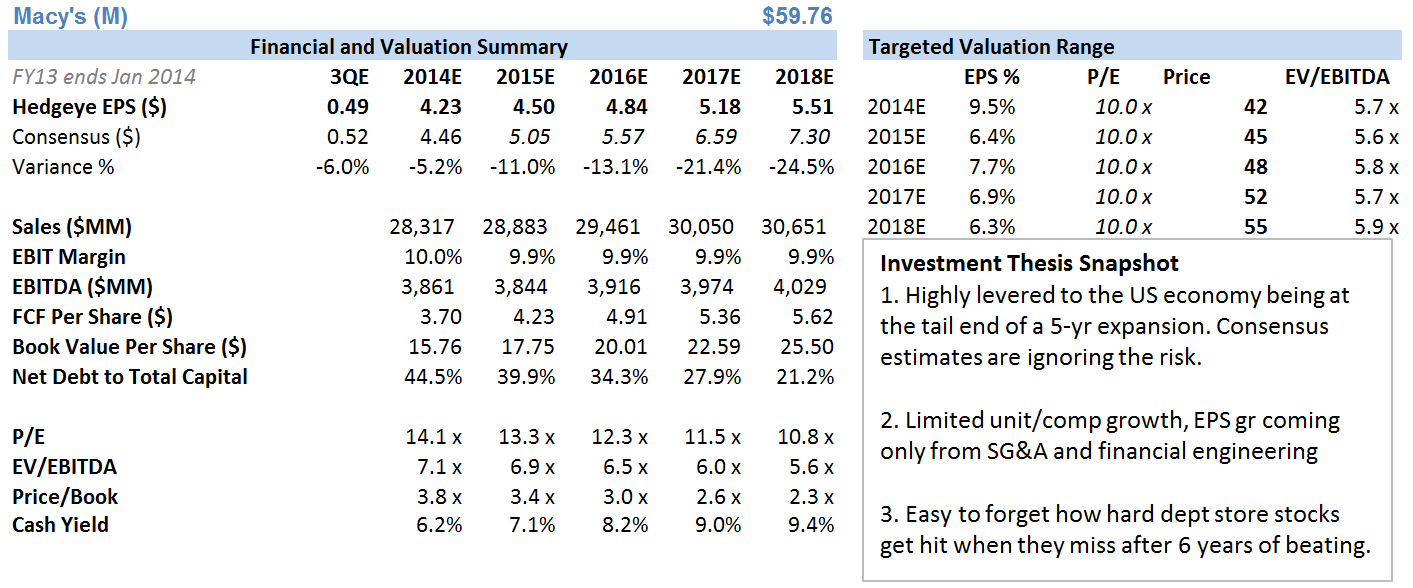

Conclusion: The quarter was more balanced than the print suggested, but we struggle with how to model anything in the ballpark of the Street’s numbers in the out years. Margins are tapped and costs are accelerating. That’s not in expectations.

We struggle with this Macy’s print to some degree. It’s easy for us to jump on the bandwagon of the company missing EPS and taking down comp guidance – obviously negative developments. But in reality, this was probably not as bad as the headline otherwise suggests. A financial algorithm of a 3.4% comp, 6.9% EBIT growth, and 10.7% EPS, and 53% cash from operations is tough to label as an outright #fail. Macy’s is the best in the business at driving its financial model, and we’ve got to respect that. But when all is said and done, we simply have a tough time justifying that there’s enough room to evolve the financial model into something that’s meaningfully better than we see today.

One of the most telling points of the conference call for us was when CFO Hoguet compared Macy’s to how the company looked a year before the economic melt-down in 2008. Since that prior peak; a) square footage is down 2%, b) sales are up by $1.95 bn, or 7.4%, c) Gross Margins are flat at 40% (peak), d) SG&A dollars are down in absolute terms by $170mm, or 2%. She’s right to call it out. It’s a heck of an accomplishment. But it’s also what gives us pause in modeling material upside over the next three years.

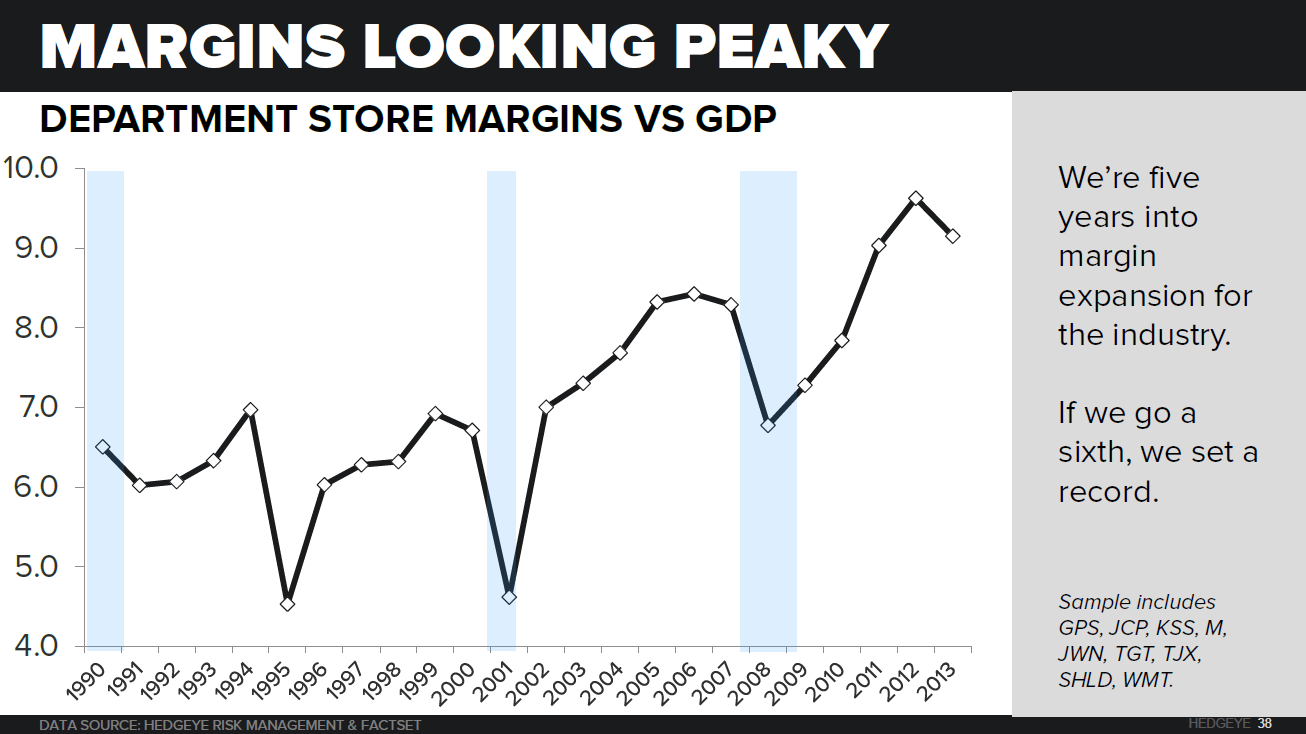

The department store group is in year six of a margin recovery cycle – and it has never gone more than five years without a correction in the past (see chart below). The company is up-front about its gross margin pressure, but then (responsibly) admits that it needs to keep spending on key initiatives to drive the top line. Management notes that it will absolutely hit a 14% EBITDA margin (70bps above current run rate), but that 15% is not likely. Whenever a management team in retail is that certain about hitting a margin target, it is usually due to lower SG&A. Our point here is that it sounds like Gross Margins are completely tapped, and SG&A leverage is in the 8th inning. In the absence of square footage growth, this tells us that we need to rely on capturing market share to drive the top line, or financial engineering to enhance EPS in order for this model to work.

Could the company earn the Street’s $5.05 next year? It’s possible. If Macy’s really wants to get there, it could. But if it accelerates investment to sustain any form of comp alongside a peak Gross Margin, then we think we’re looking at $4.50 at best.

The stock is admittedly cheap at face value. But it’s easy to forget what can happen to a department store stock that misses expectations meaningfully. People think that 7-8x EBITDA is cheap today – but these names have traded at 7x EARNINGS on the back end of past cycles. We’re not making the call today that we see this again. At least not yet. But for all these reasons, we simply would not touch Macy’s on the long side.