This note was originally published at 8am on July 28, 2014 for Hedgeye subscribers.

“Very simple. It’s going to be a big letdown for everyone. It was process and spot.”

-Rory Mcilroy

I don’t know about yours, but my multi-factor, multi-duration analysis this summer has revealed that my golf game needs some serious work. The hottest hand on the Hedgeye Research Tour, Howard Penney, reminded me that I need to get Rory’s #process.

After his British Open win, Mcilroy explained “with my long shots, I just wanted to stick to my process and stick to making good decisions… I just wanted to roll that ball over that spot. If it went in, then great. If it didn’t, then I’d try it the next hole.”

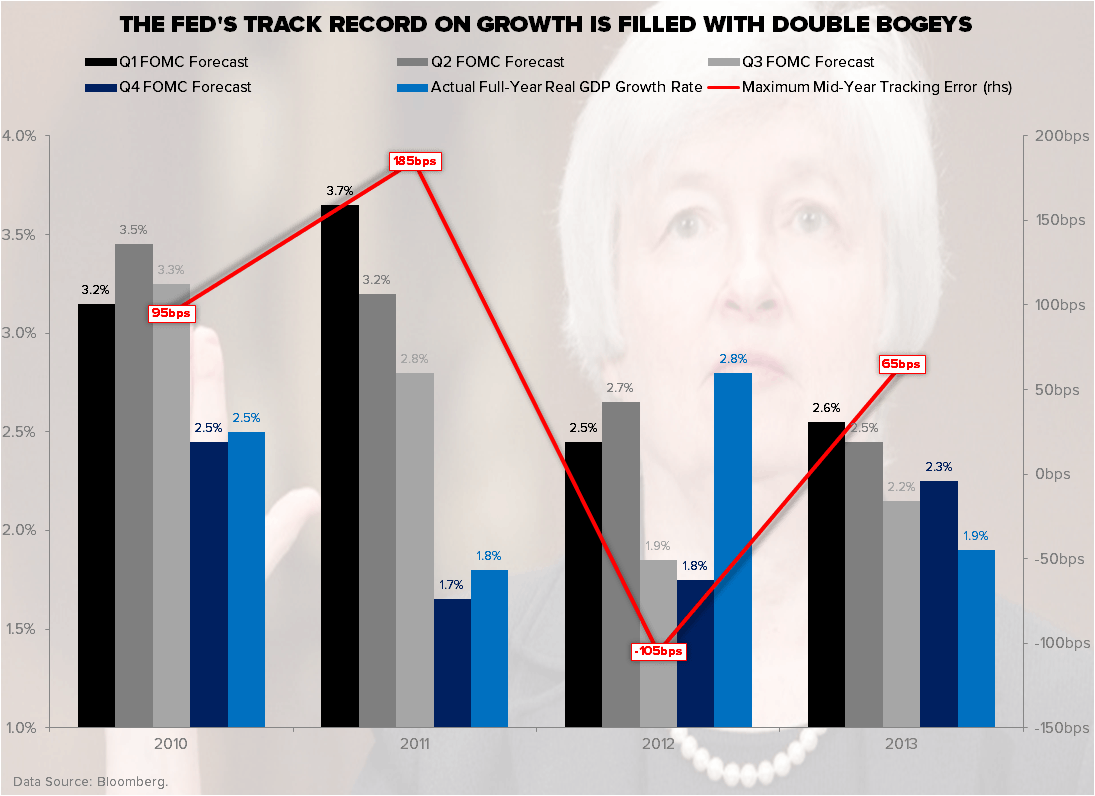

Process & Spot - #love that. If we can execute it, consistently, on the Global Macro course of interconnected risk, we’ll make less double bogeys. Remember, it’s those of you who don’t have a lot of blow-up holes that have the best performance track records.

Back to the Global Macro Grind…

In Hedgeye-speak, making our tee-to-fairway swing (process) repeatable means embracing the uncertainty of Mr. Macro Market’s intermediate-term TREND signals:

- If something like Chinese Stocks or Copper signal a bearish to bullish TREND reversal, we buy/cover

- If something like the Russell 2000 or Bond Yields signal a bullish to bearish TREND reversal, we sell/short

In long-bond speak, when we sell bond yields, we buy bonds. And we like it.

When it comes to our shorter-term duration game (putting), we try to manage what we call the immediate-term TRADE risk of the range. In other words, we respect the breaks and try to take the highest probability line of the proverbial putt by:

- Selling if the price is at the high end of the range

- Buying if the price is at the low-end of the range

Yep. So easy a Mucker can do it. What’s differentiated in this process is that I’m consistent in being inconsistent:

- My long shots are playing with the wind (bullish or bearish TREND)

- My putts are playing the breaks (fading last price)

Consensus Macro tends to do the opposite:

- Longer-term – consensus tends to be late in acknowledging bullish and bearish TREND reversals

- Shorter-term – consensus tends to chase, rather than fade, last price

Across both short and longer-term durations, you can see this on the most emotional strokes the Consensus Macro takes (net long or short futures and options bets in Big Macro positioning):

- LONG BOND (10r Treasury) saw a +26,023 wk/wk swing to a net LONG position in bonds now of +5,282 contracts last wk

- SPX (Index + Emini) saw a +37,728 wk/wk swing to a net LONG position in SP500 of +614 contracts last wk

Now, if you only look at these putts in isolation, you’d say that week over week, these were the right lines to take. But if you look at all the swings it took to get to the green, this was the score:

- LONG BOND – consensus net SHORT bet on average of -21,204 and -43,289 contracts for the last 3 and 6 months, respectively

- SPX – consensus net SHORT bet on average of -65,318 and -44,327 contracts for the last 3 and 6 months, respectively

In other words, for the last 3-6 months, Consensus Macro was A) shorting 10yr Treasuries and B) shorting SPY (and C) making double bogeys). You don’t want to be doing that.

And now you don’t want to be getting net long US Equity beta A) after consensus hedge funds have covered SPX shorts, B) Russell 2000 continues to signal bearish TREND, and C) front-month VIX is testing an intermediate-term TREND bearish to bullish reversal.

Or at least my process says you wouldn’t…

With the CRB Food Index and Energy Stocks (XLE) both up another +0.9% last week to +19.7% and +12.8%, respectively (Coffee and Cattle prices are +52.9% and +28.2% YTD), you probably want to stay net LONG our 2014 #InflationAccelerating Theme and short US Consumers (discretionary and housing stocks) too.

In golf sometimes it’s the shots you don’t take that make all the difference. #Process, spot, #process. Rinse and repeat.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.44-2.54%

SPX 1966-1987

RUT 1133-1161

VIX 11.94-14.29

Gold 1299-1323

Copper 3.20-3.28

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer