***********************************************************************************

"Is FICC Fixable? A View From The Trading Desk"

Invitation to Conference Call Thursday

Please join us this Thursday, August 7th at 11 am EST for a call with the Head of Credit Trading at TCW to discuss bond trading trends.

Participant Dialing Instructions:

- Toll Free Number:

- Direct Dial Number:

- Conference Code: 919219#

We are hosting a conference call Thursday, August 7th at 11 am EST with Jerry Cudzil, the Head of Credit Trading at TCW. This call aims to help us understand, from the view of a major buy-side trading desk, the trends in Fixed Income, Currency, and Commodity trading (FICC). Specifically, we'll be focusing on:

- Cyclical or Secular?: The buy-side's perspective on whether FICC weakness is secular or cyclical.

- Share Shifts: Market share shifts that are occurring amongst the broker-dealer community in various markets.

- The Fed: How a post-QE bond market may look and the risk/reward setup in fixed income currently.

This call will be helpful to investors in broker dealer stocks and volume-related market structure companies: GS, MS, JPM, BAC, C, PJC, RJF, CME, ICE, NDAQ

Jerry Cudzil's Bio:

Mr. Cudzil is head of U.S. Credit Trading at the Trust Company of the West (TCW), overseeing the U.S. Fixed Income group’s trading of corporate and high-yield securities and derivatives. Prior to joining TCW in 2012, Mr. Cudzil was a high yield bond trader for Morgan Stanley and Deutsche Bank, specializing in project finance, aviation, and energy securities. He was previously a portfolio manager for Dimaio Ahmad Capital, managing the multi-strategy credit fund and aviation fund and leading the firm’s risk management team. Mr. Cudzil began his career as a corporate bond trader for Prudential Securities and has also traded investment and high yield debt for Credit Suisse and Goldman Sachs. Mr. Cudzil earned a BA in Economics from the University of Pennsylvania.

***********************************************************************************

Current Best Ideas:

Key Callouts:

Last week saw one of the sharpest corrections in US equities in a few years.

Our last three weekly risk monitor headlines have read:

"Battening Down the Hatches" - 7/28/14

"Moving to Higher Ground" - 7/21/14

"Portuguese Risk" - 7/14/14

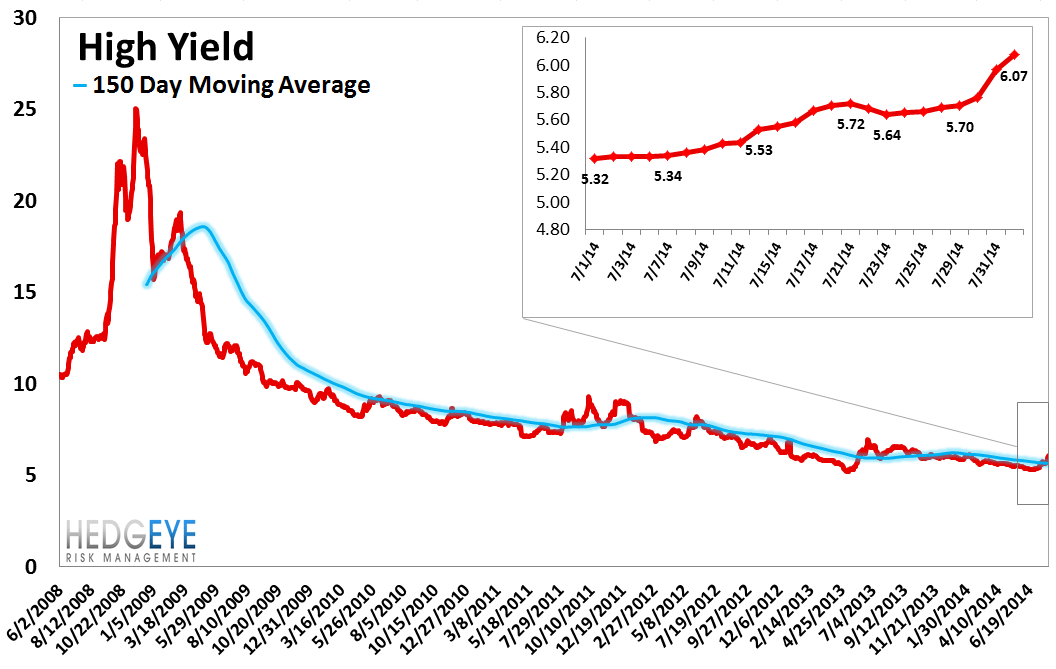

US Financial Equities are strongly correlated to junk bond yields and junk has been moving for a while. High yield was up +41.5 bps last week, rising to 6.07%, from 5.66%. On the month, high yield is now +74 bps.

Rather than point out the obvious, we'll try and point out something that could be helpful: while there is broad-based weakness across US Financials (all 27 reference entities we track were wider on the week), the systemic interbank risk measures were unimpressed. TED Spread rose 1 bp to 22 bps and Euribor-OIS rose 1 bps to 15 bps. In other words, systemic risk appears to be stable, for now.

Bigger picture, our view has been and remains that ongoing 2H14 macro headwinds from falling rates and decelerating home prices will continue to put pressure on the Financials complex.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 12 improved / 5 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Negative / 1 of 12 improved / 7 out of 12 worsened / 4 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 3 out of 12 worsened / 7 of 12 unchanged

1. U.S. Financial CDS - Swaps widened for all 27 out of 27 domestic financial institutions on the week. The average increase was 11 bps (roughly 12%). Meanwhile, the corresponding equity prices were down by an average of 4% on the week.

Widened the least WoW: UNM, XL, AGO

Widened the most WoW: GNW, AXP, PRU

Widened the least/ tightened the most WoW: AGO, MBI, UNM

Widened the most MoM: GNW, MTG, C

2. European Financial CDS - Portugal and Russia saw their bank swaps widen sharply, again, on the week. Not suprisingly, Portugal's Banco Espirito Santo - after weeks of heavy negative news flow - received a bailout over the weekend from the Bank of Portugal. Depositors and senior creditors appear to be protected, but everything downstream in the capital structure looks to be a washout. Meanwhile, US sanctions continue to take a toll on Russian banks, as Sberbank swaps widened 69 bps w/w to 352 bps and are up 110 bps on the month.

3. Asian Financial CDS - Indian bank swaps widened by an average of 15 bps on the week, while Chinese banks widened by an average of 7 bps. Japanese financials were wider, on average, by 1 bp.

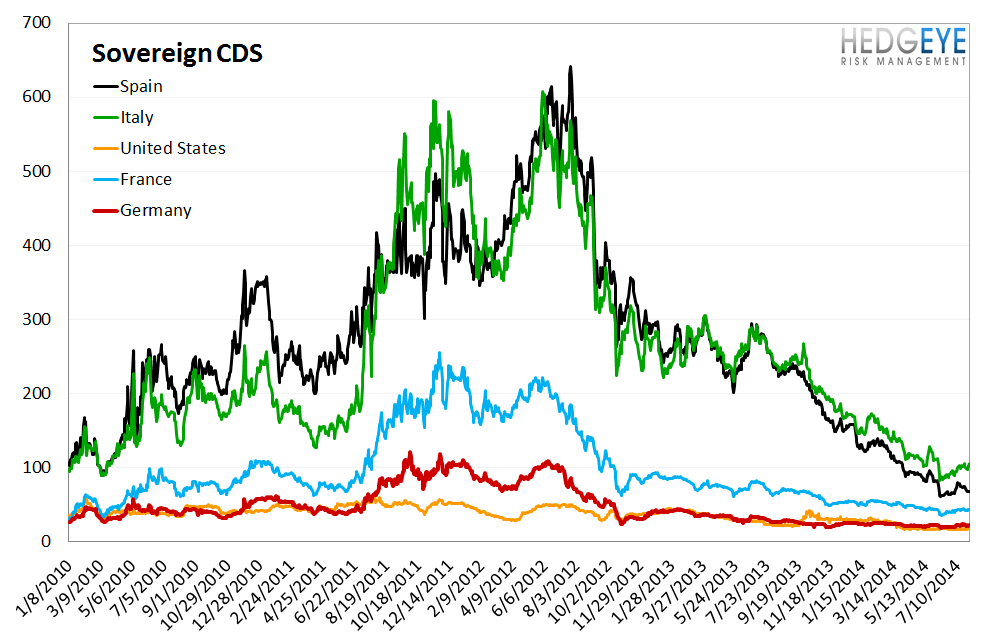

4. Sovereign CDS – Sovereign swaps were wider in Portugal and Italy (+21 bps and +6 bps, respectively), but little changed elsewhere, and actually tightened 4 bps in Spain. The US and Germany were unchanged.

5. High Yield (YTM) Monitor – High Yield rates rose 41.5 bps last week, ending the week at 6.07% versus 5.66% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 8.0 points last week, ending at 1876.

7. TED Spread Monitor – The TED spread rose 1.0 basis points last week, ending the week at 21.6 bps this week versus last week’s print of 20.61 bps.

8. CRB Commodity Price Index – The CRB index fell -2.1%, ending the week at 292 versus 299 the prior week. As compared with the prior month, commodity prices have decreased -4.6% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 15 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 14 basis points last week, ending the week at 3.20% versus last week’s print of 3.34%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China rose 0.2% last week, or 5 yuan/ton, to 3131 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

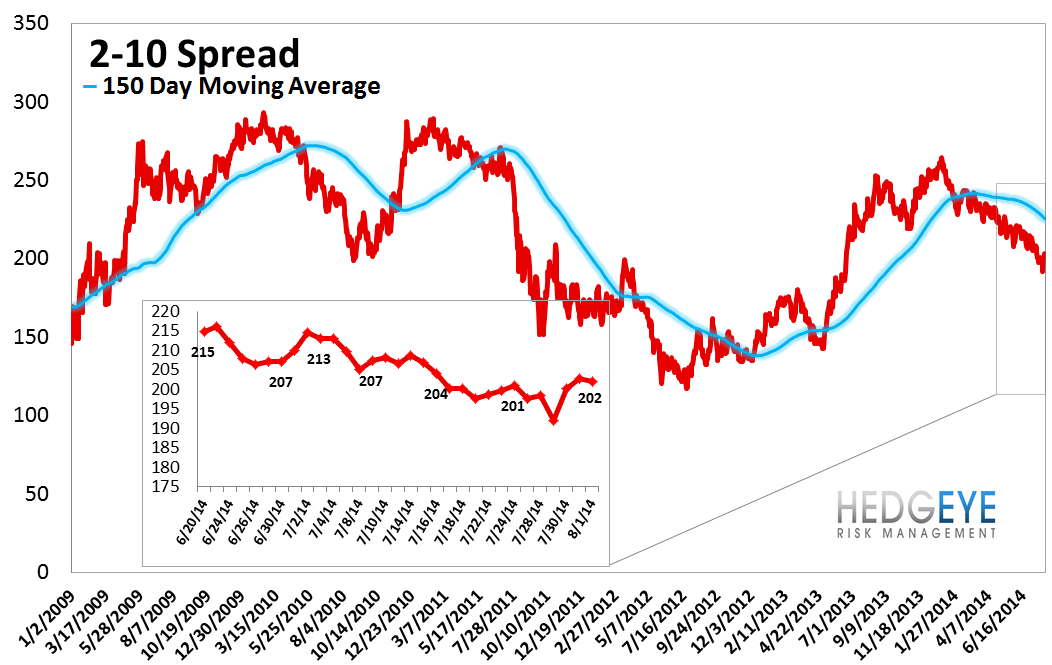

12. 2-10 Spread – Last week the 2-10 spread widened to 202 bps, 4 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 3.1% upside to TRADE resistance and 0.3% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT