TODAY’S S&P 500 SET-UP – August 1, 2014

As we look at today's setup for the S&P 500, the range is 41 points or 0.35% downside to 1924 and 1.78% upside to 1965.

SECTOR PERFORMANCE

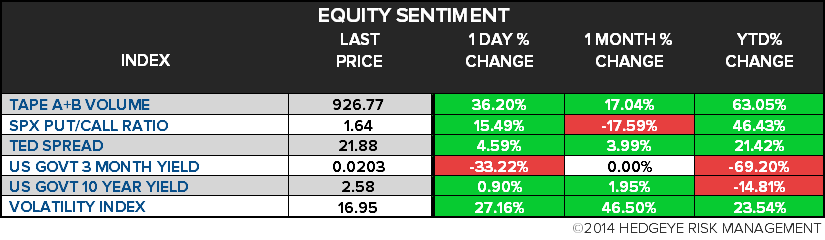

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.05 from 2.03

- VIX closed at 16.95 1 day percent change of 27.16%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, July, est. 230k (prior 288k)

- Unemployment Rate, July, est. 6.1% (prior 6.1%)

- 8:30am: Personal Income, June, est. 0.4% (prior 0.4%)

- Personal Spending, June, est. 0.4% (prior 0.2%)

- 9:45am: Markit US Manufacturing PMI, July, est. 56.5 (prior 56.3)

- 9:55am: University of Michigan Confidence, July final, est. 81.7 (prior 81.3)

- 10am: ISM Manufacturing, July, est. 56 (prior 55.3)

- 10am: Construction Spending m/m, June, est. 0.5% (prior 0.1%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Republic of Congo President Denis Sassou-Nguesso speaks about stability, security, oil investments in central Africa region

- 9am: House Republicans meeting at 9am to discuss border plan

- 2pm: DNC Chair Debbie Wasserman Schultz speaks at Natl Assn of Black Journalists conference in Boston

- U.S. ELECTION WRAP: Farmers on Immigration; Koch-Funded Groups

WHAT TO WATCH

- U.S. employers may have added 230,000 workers last month

- Ford, GM, others report U.S. auto sales; SAAR may be 16.7m

- Argentina doesn’t oppose deal sought by JPMorgan, other banks

- Argentina outlook revised to negative at Moody’s

- ICE said to seek mortgage role through talks with data service

- China HSBC PMI jumps to highest in 2 yrs

- Societe Generale 2Q net rises 7.8% as loan-loss provisions fall

- RBS trims lending ties with Russia

- No-exit strategy may be Fed’s burden as record stimulus unwinds

- Lions Gate to refile proxy after underreporting Feltheimer’s pay

- Cisco localizes production in Russia amid tensions: Kommersant

- Rosneft closes deal for Weatherford assets in Venezuela, Russia

- ArcelorMittal increases European, U.S. steel demand forecast

- Macau July casino rev. falls 3.6%, beats est.

- Israel, Hamas stop Gaza fighting as 3-day truce begins

- Flights over Iraq restricted by FAA due to armed conflict

AM EARNS

- Allete (ALE) 8:30am, $0.44

- American Axle & Mfg (AXL) 8am, $0.72

- Bell Aliant (BA CN) 6am, C$0.41

- Burger King (BKW) 7am, $0.23

- Calpine (CPN) 6am, $(0.02)

- Catamaran (CCT CN) 6am, $0.50

- CBOE (CBOE) 7:30am, $0.50

- Chevron (CVX) 8:30am, $2.63 - Preview

- Clorox (CLX) 8:30am, $1.35 - Preview

- Enbridge (ENB CN) 7am, C$0.39 - Preview

- Exelis (XLS) 6:30am, $0.35

- Fortis (FTS CN) 7am, C$0.28

- Genesee & Wyoming (GWR) 6am, $1.11

- Hilton Worldwide (HLT) 6am, $0.19

- ImmunoGen (IMGN) 6:30am, $(0.34)

- PBF Energy (PBF) 7am, $0.65

- Procter & Gamble (PG) 7am, $0.91 - Preview

- Spirit AeroSystems (SPR) 7:30am, $0.68

- Targa Resources (TRGP) 7:17am, $0.63

- Telephone & Data Systems (TDS) 7:56am, $(0.05)

- United States Cellular (USM) 7:57am, $(0.06)

- WisdomTree (WETF) 7am, $0.07

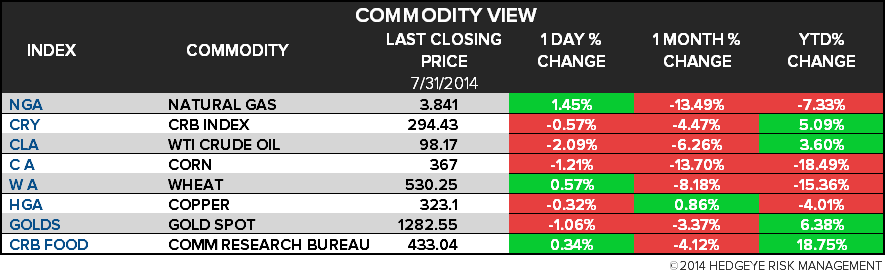

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Heads for Biggest Weekly Decline in 7 Months; Brent Steady

- Gold Trades Near Six-Week Low Before U.S. Employment Report

- Copper Set for Weekly Drop on Speculation U.S. to Curb Stimulus

- Twin Corn Ears Push U.S. Yields to Bin-Busting Crop: Commodities

- Arabica Coffee Extends-Bull Market Run as White Sugar Declines

- Sugar Seen Needing Further Drop to Attract Demand Amid Glut

- Milling Wheat Slides to Four-Year Low in Paris on Rising Supply

- AngloGold Sees More Mine Sales as Producers Chase Margin Gains

- WTI Crude Seen Rising in Survey on U.S. Economic Growth

- Rubber Sales From Vietnam Set for First Drop Since ’08 on China

- U.K. Winter Power Prices Advance After SSE Fire in England

- Shipping Rates Suffer as China Hydro Curbs Coal Imports: Freight

- As One Kurdish Crude Tanker Waits, Another Heads to New Jersey

- Europe Set for Hottest Summer Since 2006 as Warm August Seen

- Steel Rebar Has First Weekly Advance in Three on China PMI

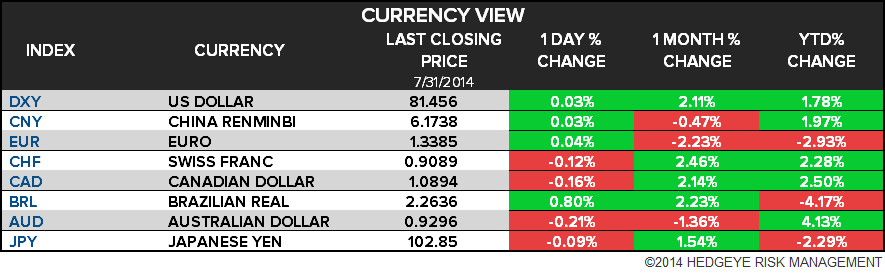

CURRENCIES

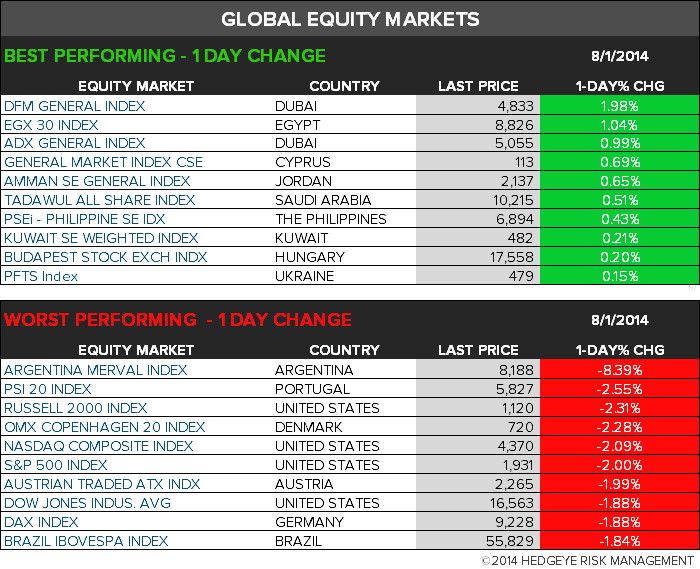

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team