Well…if you didn’t know why TGT has been strong over the past month, now you know. It’s been on the verge of hiring a new CEO and someone apparently got the memo. Quite frankly, we’re very surprised and extremely disappointed by the Board’s appointment of Brian Cornell as the new CEO and Chairman. There’s nothing wrong with Cornell at face value from where we sit. But a company as well capitalized as Target has the resources to hire the best of the best. We assumed that it would. It didn’t.

As we outlined previously (see comments below) the company could have gone in one of two directions. 1) TGT 1.0: sustain its recent strategic acceleration to being an old economy retailer – a capital-light option that will make tweaks to the business to produce near-term earnings results, or 2) TGT 2.0: hire someone who can transform the retailer to be aligned with how consumers will actually shop over the next 5-10 years, and re-emerge as the best-in-class aspirational retailer in the US, and even globally. Capital intensive near-term, but huge potential payoff long-term.

In the press release, the Board snuck in a statement that ‘Omnichannel’ will be a focus for Cornell. But truth be told, ‘Omnichannel’ is a focus for just about everyone. It’s the most abused buzzword retailers have had in decades. Don’t mistake that for #TGT2.0.

We’re divided on what this means for the stock. The twittersphere is already lighting up about how positive this is for TGT, and we’re seeing sell-side upgrades on the news. This is after a 11% run in the stock since the beginning of last month – which is a lot for Target.

Without having heard Cornell’s plans, we’re inclined to think that he’ll be focused on near-term tactical patches to the model. At risk of sounding punitive, he has not even been in any of his four most recent executive roles for more than 3-4 years before exiting for the next opportunity. Maybe he’s looking to settle down in Minny for the long haul. A near-term focus could mitigate numbers going down further over the near-term. That’s an obvious inhibitor to a short playing out right now. But it would rob exponentially from the value that could be created in the outer years – the same value that any long-term investor would pay for today.

In the end, we need to see what Cornell’s plans are for this company. The market already is placing its bets that he’ll be a winner. But call it #TGT1.0, #OldEconomy – it’s all the same. This is a bad choice and a missed opportunity to make this company great again.

07/24/14 08:33 PM EDT

TGT – Target 1.0 vs 2.0

Takeaway: If it turns out that WMT’s US CEO left to take the top job at Target, we’d look to get much heavier on the short side of TGT.

CONCLUSION: If it turns out that Bill Simon left his post as CEO of WalMart US to take the top job at Target, we’d look to get much heavier on the short side of TGT. We think that move would simply be disastrous for Target, and would set the company down a path that is simply uninvestable, and likely value-destroying.

WHY THIS WOULD BE A BAD MOVE

First off, there’s nothing wrong with Simon. The guy ran a $280bn business – nearly 4x the size of Target’s revenue base. Did WMT’s US stores knock the cover of the ball during his tenure? No. But you don’t get to be CEO of the largest division of the biggest company in the world (ranked by revenue) by being incompetent. Furthermore, Simon potentially knows more about how to collect customer data and use it to generate sales than everyone in the Target organization combined. Ultimately, for someone who thinks that the key for TGT is to be more competitive with WMT, then this would be a massive win.

But TGT Needs to Become Everything That WalMart is NOT. Trying to become WalMart is what got Target into trouble in the first place. Remember in 2008 when ‘Tarjay’ was actually inked in the Urban Dictionary to memorialize Target as a place where teens went to get trendy fashion at cheap prices? Well, management had the Branding equivalent of lightning in a bottle. Yes, WalMart envied it. So did Macy’s. So how did Target answer?

- It converted 65% of its stores from 2008 through 2013 to P-Fresh stores. Basically, this is a Supermarket where a Soccer Mom could get Eggs, Bread, Pop Tarts, and then grab a sweater and some bed linens.

- It pushed the Red Card, which gave 5% off all purchases. Over the same 2008-2013 time period, Red Card went from 5% of purchases to just shy of 20%. We’re really not worried about the direct financial impact, which is about $833mn/yr in lower Gross Profit due to higher discounts, as that realistically was offset at least a little bit by higher purchase volume. The real problem we have is with how this, combined with P-Fresh conversion changed the shopper profile.

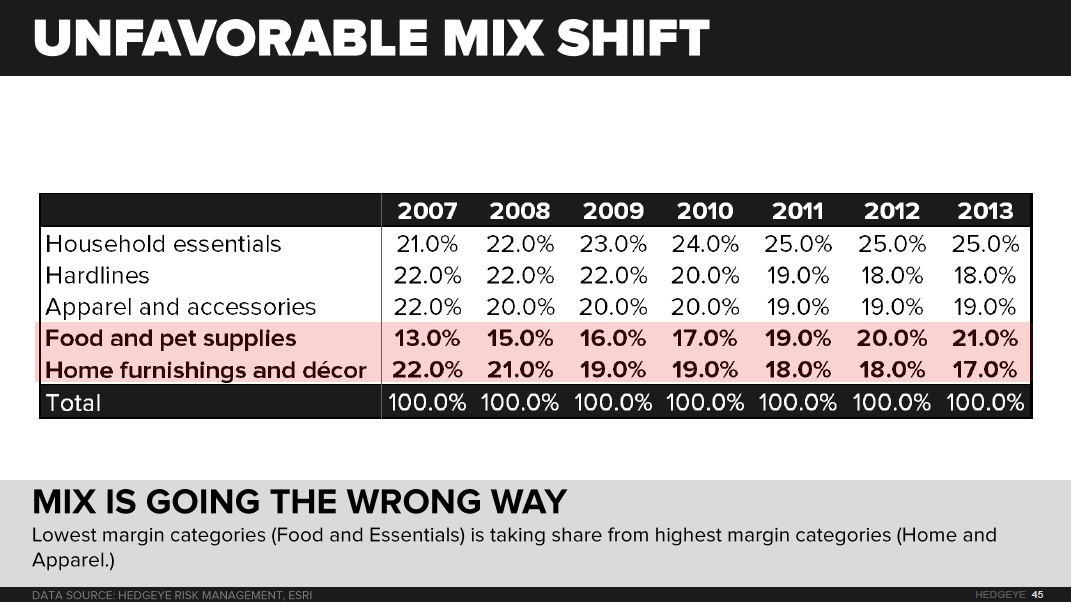

- Mix changed accordingly, with the highest margin categories like Apparel and Home Furnishings giving way to perennially low-margin Food and Household Essentials (non-food products you buy at a grocery store).

So think about it. TGT went from cool, edgy ‘Tarjay’ where it was the envy of most of its peers, with a relatively defendable customer and would actually compete on the fringes with the likes of H&M, to being the place where a person who cares about nothing but price, or shops there simply because they hate going to WalMart. It went from having a peer group where it had a notable competitive advantage, to putting itself right in the middle of four unique competitors – 1) WalMart, 2) Department Stores, 3) Dollar Stores, and 4) Supermarkets. As a bonus, it has Amazon.com hovering over its head plucking away every last sales dollar it can.

Oh, and by the way, once TGT realized this was a multi-year string of horrible decisions, it decided to look to a new venue for growth – Canada. We have a whole deck quantifying why that’s flawed. But by now that’s hardly an out-of-consensus view.

Our point is that this whole mess is why Steinhafel was fired as TGT’s CEO. It wasn’t due to the data breach. Maybe the breach was a good excuse, or a catalyst, for the Board. But it was not the reason for ousting him.

This brings us to why hiring Bill Simon as TGT’s CEO would be a very bad idea.

All of Target’s missteps over the past six years are a product of what we’d call ‘Retail 1.0’. Simon is the zen master of Retail 1.0. Unfortunately, upgrading to Retail 2.0 is the only thing that can save Target now, and we seriously doubt that Simon could do it. Importantly, if the Board hires him, then it shows us that it is content with Retail 1.0. That’s a multiple-compressing event, over time.

We don’t think that Target 2.0 will be achieved by rolling back the clock to try and recapture the string of excellence it had in the 2000s. That’s actually borderline impossible. It would be like taking a pickle and trying to make it a cucumber again.

It really needs someone to step in and change the paradigm. Target has tremendous assets – in its store base, logistics network, and (too many) people. The Board should not be looking at McMillon’s team at WMT for a new CEO, but instead should be looking at Jeff Bezos’ team at AMZN. That’s the place/culture to look for a winner that could not only fix Target’s dot.com business, but make it a Brand that anticipates where and how consumers will shop 5-10 years down the road.

What This Means For The Stock.

1) We’re going to give the TGT Board the benefit of the doubt on this one. We think that it is looking for a CEO who can make sweeping changes to create considerable shareholder value 4-5 years out (i.e. Target 2.0). We also think that anyone who takes on that challenge will make sure that he/she has the Board’s buy-in to spend the considerable capital needed to change this company so dramatically. Ultimately, we think that this could lead to TGT being the best performing stock in the S&P – in about 2019. Until then, it will be extremely slow and painful, and earnings and cash flow assumptions out there will prove to be way to high. For the record, this is similar to what we said about JCP when it was at $40. TGT could get cut in half under that scenario.

2) Scenario 2 is a little tougher. This is the Target Board sticking with Target 1.0. That means that we could see the stock pop on the news, like with any scenario, and that the new CEO will be making tweaks to boost near-term cash flow and earnings. That might take numbers higher, but it will seriously dampen the potential for any real growth in this business. Then you’re playing for a levered, low-growth retailer in year six of a retail margin expansion cycle – something we’ve never EVER seen go into year seven.

We still like the risk-reward on this one – a lot.