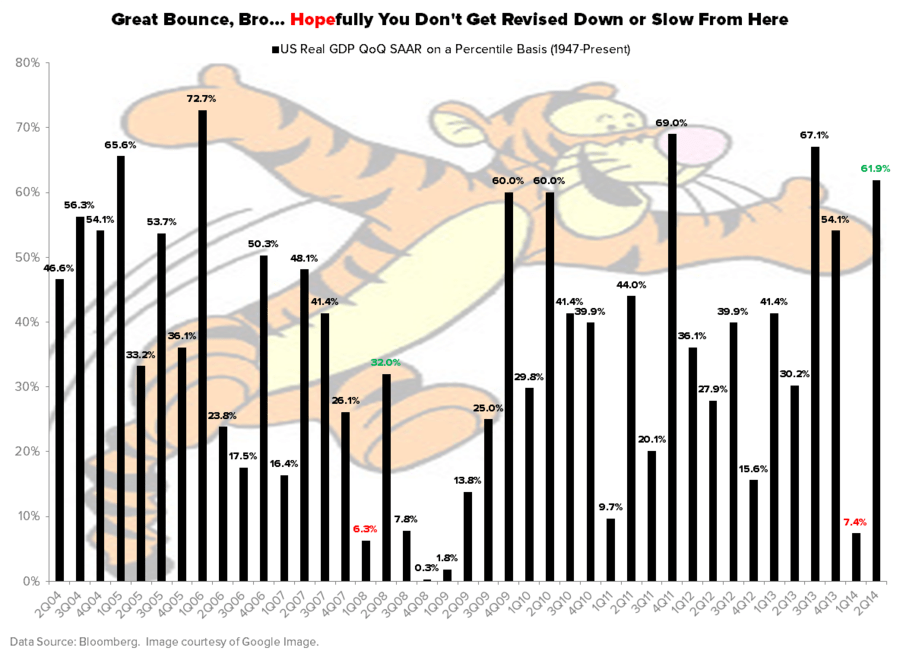

To be fair to the 2014 US Growth Bulls who are looking for +3-4% GDP and a 10yr Yield > 3%, with a Q2 +4% bounce off of one of the worst Q1s since WWII on an annualized basis, 1st half of the year GDP in the US wasn’t negative. It was +0.87%.

To be fair to the 2014 US Growth Bulls who are looking for +3-4% GDP and a 10yr Yield > 3%, with a Q2 +4% bounce off of one of the worst Q1s since WWII on an annualized basis, 1st half of the year GDP in the US wasn’t negative. It was +0.87%.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.