TODAY’S S&P 500 SET-UP – July 30, 2014

As we look at today's setup for the S&P 500, the range is 18 points or 0.51% downside to 1960 and 0.41% upside to 1978.

SECTOR PERFORMANCE

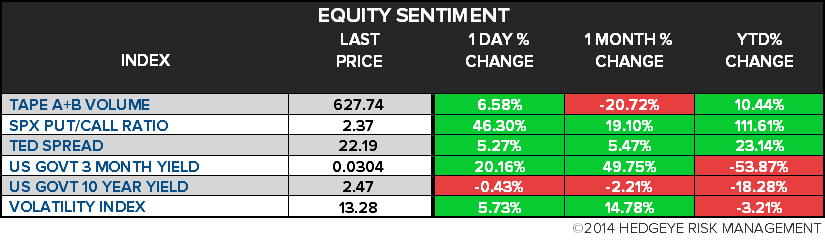

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.93 from 1.92

- VIX closed at 13.28 1 day percent change of 5.73%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, July 25 (prior 2.4%)

- 8:15am: ADP Employment Change, July, est. 230k (prior 281k)

- 8:30am: GDP Annualized q/q, 2Q, est. 3% (prior -2.9%)

- Personal Consumption, 2Q, est. 1.9% (prior 1%)

- 2pm: FOMC seen maintaining overnight bank lending rate target near 0%, reducing QE by another $10b

GOVERNMENT:

- President Obama speaks on the economy in Kansas City

- Sec. of State John Kerry in India, joined by Commerce Sec. Penny Pritzker for 5th U.S.-India Strategic Dialogue

- 10am: Sen. Judiciary Cmte hearing on Violence Against Women Act, protecting women from gun violence

- 10am: Senate Banking subcmte hearing on flood insurance

- 10am: House Judiciary Cmte hearing on need for special counsel to investigate IRS

- 10:45am: Sens. McCaskill, D-Mo.; Heller, R-Nev.; Blumenthal, D-Conn.; Grassley, R-Iowa; Gillibrand, D-N.Y.; Ayotte, R-N.H.; Rubio, R-Fla. hold news conf. to introduce bill to combat sexual assaults on college, university campuses

- 12pm: Sen. Minority Leader McConnell, R-Ky.; and Rep. Kelly, R-Pa., hold news conf. on economic consequences of EPA’s proposed power plant rule

WHAT TO WATCH:

- EU joins U.S. in escalating pressure on Russian finance

- Putin jeopardizes Russian firms’ access to $600b in funds

- MSCI in “active dialogue” with global investors on Russia

- Fed Decision-Day Guide: QE tapering, job gains, inflation debate

- AstraZeneca to buy respiratory rights from Almirall for $875m

- SEC may revise speed rules on IEX exchange plans: Reuters

- McDonald’s Japan pulls profit forecast amid supplier scandal

- Toyota outsells VW, GM in 1H on rising demand for SUVs

- Former Time Warner CEO Parsons says Fox offer “Way Off Mark”

- Barclays returns to 2Q profit on costs, provisions

- ECB says bank credit standards eased for first time since 2007

- Argentine debt talks to resume today as default deadline looms

- Ending ‘too big to fail’ may rest on obscure contract language

- Shelling of UN shelter in Gaza kills 20 as fighting worsens

- Japan’s output drops most since 2011 as consumers spend less

- Osram to cut ~7,800 jobs worldwide

AM EARNS:

- ADT (ADT) 6am, $0.47

- AllianceBernstein (AB) 7:15am, $0.41

- American Tower (AMT) 7am, $0.53 - Preview

- Booz Allen Hamilton (BAH) 6:30am, $0.42

- Carlyle (CG) 6:30am, $0.74

- Cenovus Energy (CVE CN) 6am, C$0.50 - Preview

- CGI (GIB/A CN) 6:30am, C$0.73

- Dominion Resources (D) 7:30am, $0.62

- Energizer (ENR) 7:30am, $1.54 - Preview

- Franklin Resources (BEN) 8:30am, $0.95

- Garmin (GRMN) 7am, $0.76

- Goodyear Tire & Rubber (GT) 7:30am, $0.79

- Hess (HES) 7:30am, $1.18 - Preview

- Hospira (HSP) 7:30am, $0.57

- Humana (HUM) 6am, $2.19

- Huntsman (HUN) 7am, $0.48

- Intact Financial (IFC CN) 6am, C$1.55

- InterActiveCorp (IACI) 7:30am, $0.79

- Lorillard (LO) 7am, $0.88 - Preview

- Lumber Liquidators (LL) 7am, $0.63

- MeadWestvaco (MWV) 7:25am, $0.50

- MEG Energy (MEG CN) 5am, C$0.45

- Nice Systems (NICE) 5:30am, $0.59

- Phillips 66 (PSX) 8am, $1.69 - Preview

- Pitney Bowes (PBI) 6:30am, $0.46

- Public Service Enterprise Group (PEG) 7:30am, $0.51

- Revlon (REV) 6:30am, $0.46

- Rockwell Automation (ROK) 7am, $1.55

- Sealed Air (SEE) 7:30am, $0.38

- Sherritt Intl (S CN) 6:09am, C$(0.07) - Preview

- SodaStream Intl (SODA) 7:30am, $0.40

- Sonus Networks (SONS) 7am, $0.01

- Southern (SO) 7:30am, $0.67

- Sprint (S) 7:30am, $(0.05)

- SPX (SPW) 6:30am, $1.19

- Taser Intl (TASR) 7:30am, $0.08

- Thomson Reuters (TRI CN) 7am, $0.46

- TransAlta (TA CN) 7:45am, $0.01

- Valero Energy (VLO) 7:49am, $1.20 - Preview

- Valley National Bancorp (VLY) 7am, $0.14

- WellPoint (WLP) 6am, $2.26

- Wisconsin Energy (WEC) 7am, $0.52

PM EARNS:

- Agnico Eagle Mines (AEM CN) 5pm, $0.28 - Preview

- Akamai Technologies (AKAM) 4:01pm, $0.55

- Albemarle (ALB) 4:03pm, $1.10

- Allstate (ALL) 4:05pm, $0.66

- American Equity Investment (AEL) 4pm, $0.50

- Barrick Gold (ABX CN) Aft-Mkt, $0.15 - Preview

- BioMarin Pharmaceutical (BMRN) 4pm, $(0.43)

- Duke Realty (DRE) 4:11pm, $(0.03)

- Enbridge Energy Partners (EEP) 4:01pm, $0.24

- First Quantum Minerals (FM CN) 5pm, $0.25 - Preview

- FMC (FMC) 4:15pm, $1.02

- FNF (FNF) 4:03pm, $0.52

- Fortune Brands (FBHS) 4:01pm, $0.54

- Halcon Resources (HK) 4:15pm, $0.04

- Hartford Financial (HIG) 4:15pm, $0.67

- Hologic (HOLX) 4:01pm, $0.34

- Intersil (ISIL) 4:05pm, $0.18

- KapStone Paper (KS) 4:15pm, $0.60

- Kinross Gold (K CN) 5pm, $0.04 - Preview

- Kraft Foods (KRFT) 4pm, $0.82 - Preview

- Lam Research (LRCX) 4:05pm, $1.23

- LifeLock (LOCK) 4:05pm, $0.04

- Lincoln National (LNC) 4:10pm, $1.36

- Lundin Mining (LUN CN) 5pm, $0.06 - Preview

- Manitowoc (MTW) 4:25pm, $0.43

- MetLife (MET) 4:05pm, $1.41

- Moelis (MC) Aft-Mkt, $0.25

- Murphy Oil (MUR) 5:01pm, $1.22

- Noble (NE) 5pm, $0.66

- Penn Virginia (PVA) 4:05pm, $(0.04)

- Pilgrim’s Pride (PPC) 4:45pm, $0.66

- Questar (STR) 4:14pm, $0.22

- Rovi (ROVI) 4:05pm, $0.40

- RR Donnelley (RRD) 4pm, $0.35

- Ruckus Wireless (RKUS) 4:05pm, $0.05

- Service Intl (SCI) 4:15pm, $0.23

- ServiceNow (NOW) 4:01pm, $(0.07)

- Solazyme (SZYM) 4:25pm, $(0.39)

- Spansion (CODE) 4:03pm, $0.25

- Suncor Energy (SU CN) 10pm, C$0.98 - Preview

- Superior Energy Services (SPN) 4:05pm, $0.41

- Tesoro (TSO) 4:30pm, $1.82 - Preview

- Unum (UNM) 4pm, $0.87

- Weight Watchers Intl (WTW) 4:05pm, $0.77

- Western Digital (WDC) 4:15pm, $1.73 - Preview

- Whiting Petroleum (WLL) 4pm, $1.26

- Whole Foods Market (WFM) 4:03pm, $0.39

- Williams (WMB) 4:05pm, $0.22

- Yamana Gold (YRI CN) 4:20pm, $0.03 - Preview

- Yelp (YELP) 4pm, $(0.03) - Preview

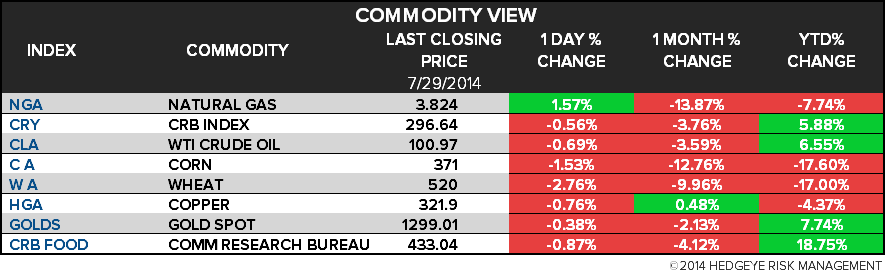

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI’s Discount to Brent Shrinks as Russia Sanction Impact Muted

- Stolen India Coal Sent to Market in Modi’s Backyard: Commodities

- Commodity Assets Seen by Barclays Increasing to $325 Billion

- Thai Sugar Offered at Discount to New York, Green Pool Says

- Gold Holds Two-Day Decline as Investors Weigh U.S. Outlook

- Japan Buys 26,340 Mt of Feed Wheat 122,750 Mt of Feed Barley

- Soybeans in Chicago Climb as Much as 0.3%, Reversing Decline

- Haze Fines Win Indonesia’s Support With Caveats: Southeast Asia

- Rubber Drops as Japan Industrial Output Falls More Than Forecast

- HSBC, ABN Sue Metals Trader Detained in Qingdao Loan Fraud Probe

- Cocoa Arrivals in Brazil’s Bahia Advance 2.3%, Hartmann Reports

- China Rows Back on Shale Ambitions as Expertise Falls Short

- Aluminum Beating Copper as Supply-Demand Flips: Chart of the Day

- Oil Market Losing Faith in Libya’s Ability to Ramp Crude: Energy

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team