Investment Ideas

The table below lists our Investment Ideas as well as our Watch List -- a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

YUM: We removed long YUM from our Investment Ideas list in part due to the recent food scandal in China and its implications on the company's ability to hit its current full-year targets, which we now fear may be too aggressive. We ran through our thoughts in a recent note below.

MCD: We added short MCD to our Investment Ideas list following the company's lackluster 2Q14 results. We believe the management's current "reset plan" will prove inadequate and the company will be forced to undertake a major restructuring in 2015. We ran through our thoughts in a recent note below.

Recent Notes

07/21/14 MONDAY MASHUP: EARNINGS KICKOFF

07/21/14 CMG CONSUMER SURVEY: DOES CMG HAVE PRICING FLEXIBILITY?

07/21/14 DFRG: THOUGHTS INTO THE PRINT

07/21/14 CMG: SIMPLY INCREDIBLE

07/22/14 INFLATED MULTIPLE DEFLATING

07/22/14 MCD: IN NEED OF A MAJOR RESTRUCTURING

07/23/14 YUM: LOSING FAITH

07/24/14 BLMN: 2Q ESTIMATES ARE TOO HIGH

Events This Week

Monday, July 28th

- DENN earnings call 4:30pm EST

Tuesday, July 29th

- DIN earnings call 11:00am EST

- RT earnings call 4:15pm EST

- BWLD earnings call 5:00pm EST

Wednesday, July 30th

- PNRA earnings call 8:30am EST

- DAVE earnings call 4:30pm EST

Thursday, July 31st

- BAGL earnings call 4:30pm EST

- BBRG earnings call 5:00pm EST

Friday, August 1st

- BKW earnings call 8:30am EST

- RUTH earnings call 8:30am EST

Chart of the Day

Recent News Flow

Monday, July 21st

- No news

Tuesday, July 22nd

- SBUX Nikkei reported that Starbucks has plans to more aggressively open stores (an additional ~260 over the next three years) in Japan, shifting its focus to the suburbs.

Wednesday, July 23rd

- MCD was upgraded to buy at LBBW with a $104 PT.

- MCD was downgraded to equal-weight at Stephens with a $100 PT.

- MCD was downgraded to underperform at CLSA with a $101 PT.

- MCD was downgraded to neutral at RW Baird with a $98 PT.

- MCD was downgraded to neutral at Sterne Agee.

- EAT was downgraded to sector perform at RBC Capital with a $49 PT.

- BOBE detailed the qualifications of its Board nominees in a letter to shareholders.

Thursday, July 24th

- WEN named Brandon Solano Senior VP of Marketing. Prior to joining Wendy's, Solano held various roles at Domino's, The Hershey Company, Procter & Gamble, the Kellogg Company and Newell Rubbermaid.

- DRI Starboard Value filed a complaint against Darden, seeking an order to force the company to hand over certain books and records related to the company's sale of Red Lobster to Golden Gate Capital.

Friday, July 25th

- LOCO El Pollo Loco IPO (originally priced at $15.00) opened at $19.00 on the Nasdaq. It ended the day trading at $24.03.

- CMG detailed plans for its Cultivate Dallas-Ft. Worth Festival, which will include cooking demonstrations, Kids' Zone games, other activities and live music headlined by Amos Lee and O.A.R.

Sector Performance

The XLY (-1.0%) underperformed the SPX (+0.0%). In aggregate, both casual dining stocks (-0.6%) and quick service stocks (+0.7%) outperformed the XLY Index.

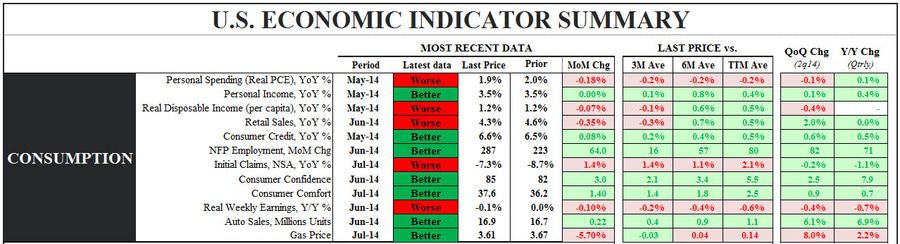

Consumption

The Hedgeye U.S. Consumption Model continues to signal bullish, with 7 out of 12 metrics flashing green.

XLY Quantitative Setup

From a quantitative perspective, the sector remains bullish on an intermediate-term TREND duration.

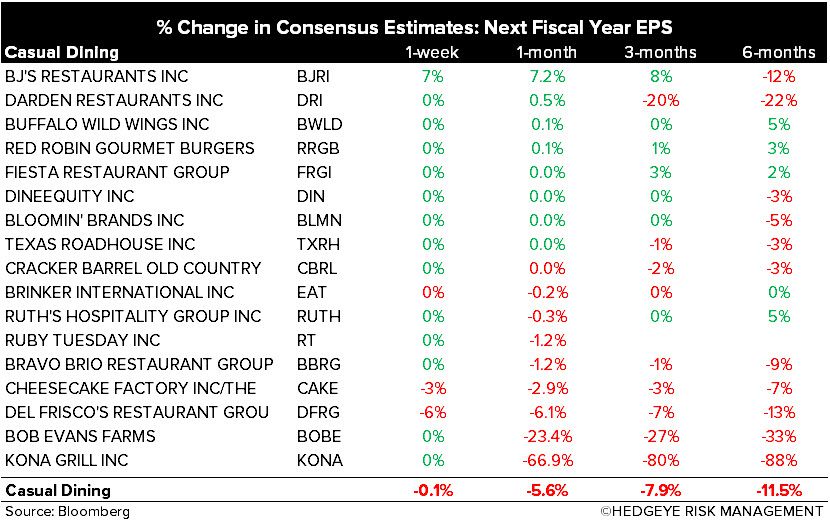

Casual Dining Restaurants

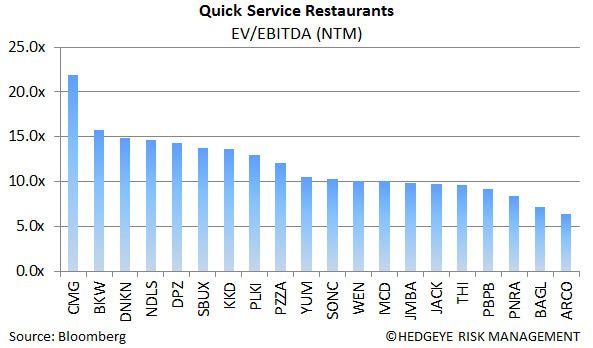

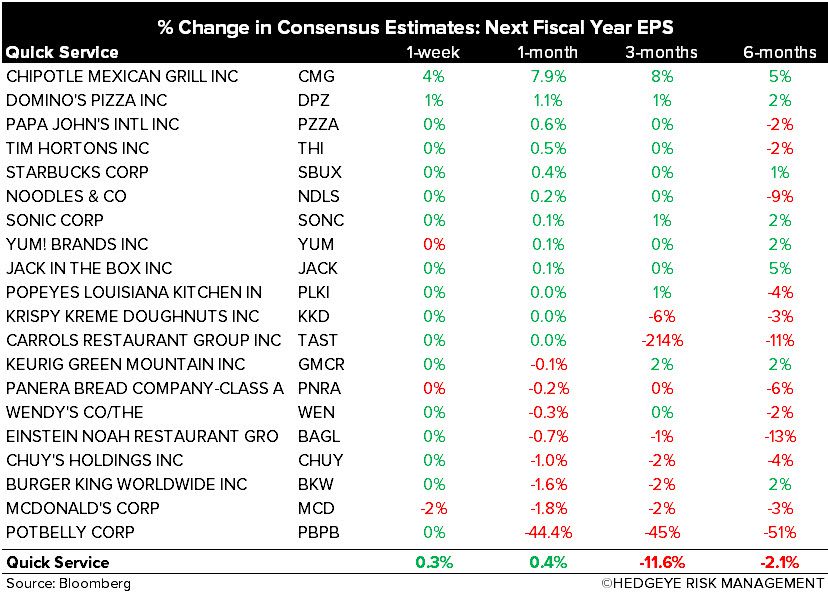

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst