NOTE SUMMARY

- NEW MOVING PARTS: Acquisitions, new ad formats, World Cup, management shakeup, potentially new metrics. There will be a lot of noise in this print distracting the street from the underlying trends in the core business.

- WHAT'S MORE IMPORTANT: We believe TWTR's chief source of growth over the LTM has been, and will continue to be, surging ad load. Ultimately, we expect this strategy has limited runway since it risks pushing its users away.

- WILL IT BE ENOUGH?: Upside to estimates is the ongoing street expectation; its quarterly sell-offs on strong results suggest as much. The question is how much upside is the street looking for? We don't know the answer, but either way, it's asymmetric setup to the downside.

NEW MOVING PARTS

TWTR has been very active this quarter. The company has made 7 acquisitions in 2Q14, which we believe is a record for the company. We are not sure how much they will contribute to the top-line, but if anything, it offers some upside to 2Q14 and guidance, especially considering the potential impact of the World Cup on engagement trends.

We've also seen some churn at the management level. The company has eliminated its COO position, hired a new CFO (Noto), moving Gupta to oversee a group focusing on start-up acquisitions, in addition to replacing heads of Finance and Engineering.

There may also be some added noise to the print. WSJ reported that TWTR may introduce new metrics, supposedly to provide another perspective on user engagement (link).

A series of acquisitions, management shake-up, and potentially new metrics sound like management is scrambling; the question is why. Maybe they're seeing what we're seeing: it's going to get that much tougher to deliver the type of growth the street is expecting under its current growth strategy.

WHAT'S MORE IMPORTANT

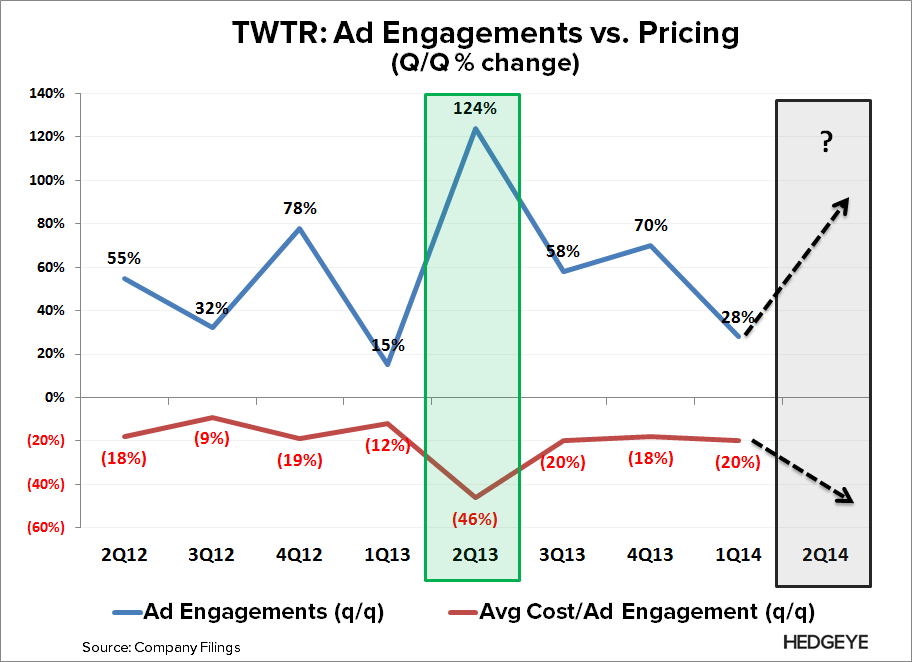

The issue we see to future growth is how we believe the company is deriving it today: surging ad load (supply). This isn't a reported metric, but the company's trends in reported ad engagements and ad prices paint the picture.

The metrics in the chart below are the sequential change in ad engagement and ad pricing as reported by management (-.86 correlation dating back to 2Q12). We believe the ongoing deceleration in pricing is a reflection of an accelerating level of available ad inventory (supply).

Twitter's ads are purchased through its self-service ad exchange, where the price is determined through a bidding process. We estimate the average cost/ad engagement (price) has cumulatively declined 85% over the last 2 years. We believe a continued surge of increasing ad inventory led to this decline. The tight correlation between ad engagements and pricing during the period suggests rising supply has been its largest source of monetization growth.

It's important to note what happened in 2Q13, when TWTR saw its sharpest drop in ad price, which we see as massive supply shock in ad inventory. In order to sustain its growth trajectory, TWTR needed a comparable surge in ad supply in 2Q14, which is what we believe they've done. We ran a small poll of twitter users asking if they have noticed rising ad load, 71% said yes (link). Remember TWTR's ads are scattered throughout a user's timeline, so far such a high percentage of users to notice suggests the increase is considerable.

Now the issue with this strategy is that there will be a point where rising ad load will push the user away because TWTR's ad revenue/engagements are primarily driven by mobile (smaller screen). We're not saying they will lose the loyal user, but the quasi-plugged-in casual user, who are more likely its newer members. In turn, user growth will become more challenging because the company will have to produce growth alongside a growing churn issue. If user growth starts to meaningfully decelerate, the street will likely punish the stock for it, even if revenues are climbing. One way or another, something has to give: revenue or user growth.

WILL IT BE ENOUGH?

TWTR's short public history suggests it has fallen victim to outlandish expectations. Despite the beats and raises on both the 4Q13 and 1Q14 prints, the stock has sold off on each. With TWTR, the expectation isn't consensus, its beating consensus, so the question is how much of a beat is the street expecting?

We don't know the answer to that, but we do see an asymmetric setup to the downside. Further, with upside comes a higher hurdle later on, as consensus increases estimates for 2014, but more so for 2015.

So the longer-term question is what happens when to the stock when TWTR can no longer jump the ever-increasing hurdle?

Let us know if you have any questions, or would like to discuss further.

Hesham Shaaban, CFA

@HedgeyeInternet