COMPANY NEWS

SIGMA REVIEW: Here are the SIGMAs for the eight retail-related companies that reported earnings this week. There are no clear trends within the group in aggregate, but there are some interesting callouts.

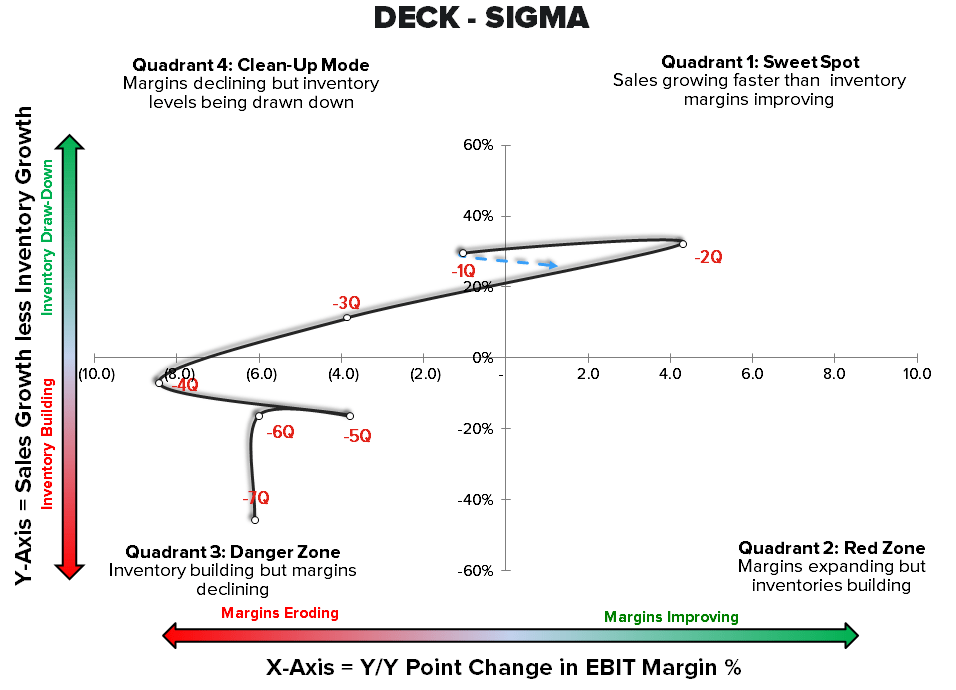

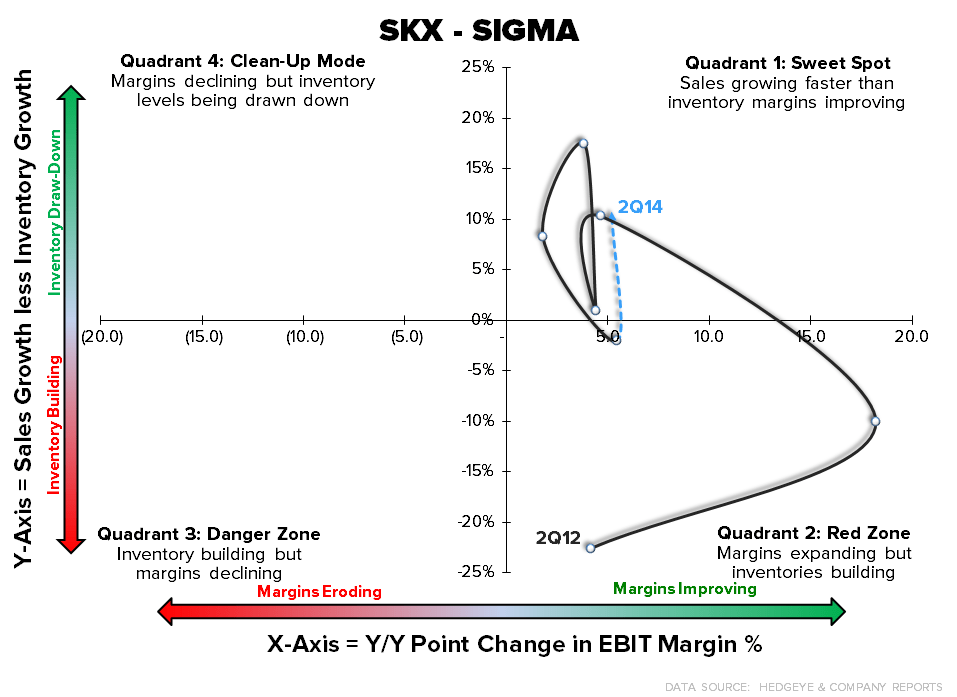

- SKX, HBI and DECK all moved into Quadrant 1 -- sales growing faster than inventories and margins improving. They have the best setup headed into 3Q. But for the most part, the market knows it.

- UA and AMZN are still putting up weak margins, but inventories are getting better on the margin, which bodes well for a GM recovery in 2H.

- CRI is probably the most notable callout. The company has been growing inventory faster than sales for six quarters in a row. In fact, CRI is sitting next to CAB (which missed big) as the only companies that are in Quadrant 2, which we think is the most dangerous place of all. It is a spot where margins are positive, allowing management teams to be complacent about elevated inventory levels. This almost never works out well for the company in question -- especially when it's trading at 18x earnings. We don't like CRI -- to be clear (it's on our short bench). We'll be back with an analysis as to whether this is the appropriate timing for us to be vocal on the name.

AMZN - 2Q14 Earnings

DECK - 1Q15 Earnings

COLM - 2Q14 Earnings

UA - 2Q14 Earnings

CRI - 2Q14 Earnings

HBI - 2Q14 Earnings

SKX - 2Q14 Earnings

CAB - 2Q14 Earnings

DECK 1Q15 Earnings

Takeaway: Weak guide - taking top line expectations up by $15.5mil ($20mil beat in the Q) and EPS up a nickel after blowing away numbers by $0.22. Coming out of the quarter inventories look healthy and that almost always sets up favorably for a positive Gross Margin event, but that will be offset by SG&A deleverage as the company adds another 30-35 units on to its existing base of 117. The question we have for DECK is - why continue the square footage growth when retail concepts have been unable to comp at the store level (-2.8% CY on top of a -5.3% LY)? We don't buy the store and e-commerce symbiosis argument. This is a company that does over a $1bil wholesale…it's not like it has an awareness problem. Instead of opening singularly focused retail concepts, why not roll half that cash into a killer e-commerce site to leverage the awareness offered by wholesale partners.

WMT - Walmart Names Greg Foran President and CEO of Walmart U.S.

- "...Walmart announced that Greg Foran, 53, has been promoted to President and CEO of Walmart U.S. Foran succeeds Bill Simon who has been in the role since June 2010 and will be transitioning out of the company."

Takeaway: For a more detailed recap on our thoughts on Simon's departure and how it relates to TGT see our note from last night titled TGT: 1.0 vs. 2.0. Link - CLICK HERE

TGT - First TargetExpress opens its doors in Dinkytown near U

(http://www.startribune.com/business/268208242.html)

- "The Minneapolis-based retailer will open a 20,000-square-foot TargetExpress store in Dinkytown Wednesday, the first of its kind for Target at about a sixth of the size of traditional locations."

- "The prototype feels like a drugstore along the lines of a CVS or Walgreens, but has its own Target flair with merchandise that includes groceries, bedding, smartphones…"

- "...Target already is planning four more locations for 2015 — one in St. Paul’s Highland Park and three in the San Francisco Bay Area."

Takeaway: TGT's answer to WMT's Neighborhood Markets and Express Stores. TGT Express stores = 1, WMT small format stores = 370. We give the company credit for testing this new prototype. Something it's been slow to do in the past. But, in order for TGT to succeed it needs to redefine its place in the marketplace not chase the 800lb gorilla that is WMT.

OTHER NEWS

JWN - Nordstrom Hiring 400 Staff, Including 30 Managers, for 2nd Canadian Store

(http://www.retail-insider.com/retail-insider/2014/7/nordstrom-hiring)

- "Nordstrom is hiring management and staff for its new Ottawa store, the second to open in Canada. In total, about 30 managers and over 350 additional staff will be hired for the Rideau Centre location, scheduled to open March 6th, 2015."

Vineyard Vines Unveiling NYC Unit

- "This fall, the Stamford, Conn.-based sportswear brand will open its first unit in New York City, a 2,500-square-foot store at 1151 Third Avenue, at 67th Street. The store is expected to be opened in early November."