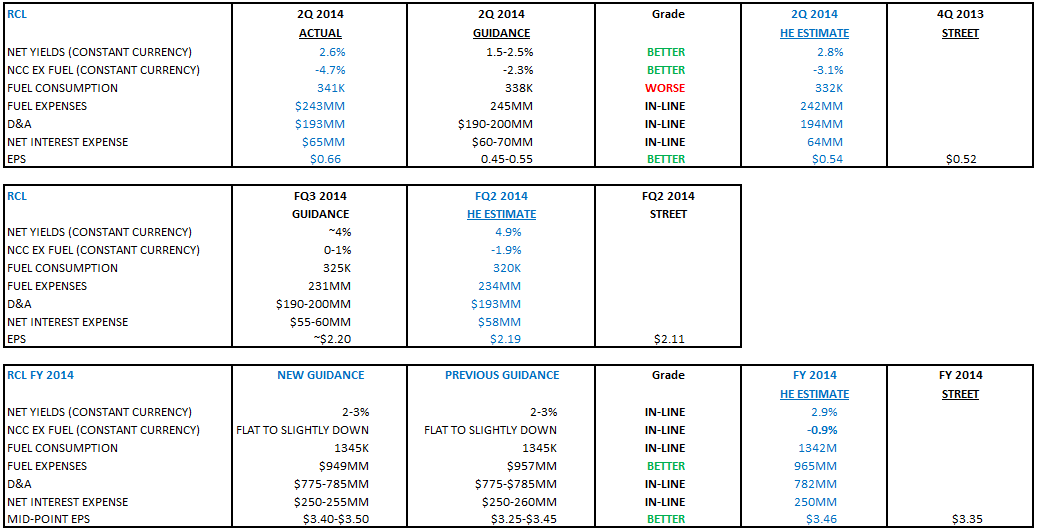

As we expected, Europe lead the Q2 beat despite lower onboard spend than we thought. 3Q net yield guidance was within expectations. Quantum will be the next catalyst in November.

CONF CALL NOTES

- Double Double program (3-yr goal):

- Optimizing revenue

- Structurally, had seen general pressure on pricing and compression on pricing

- 4 areas of revenue expansion:

- Strengthening brand

- Azamara achieving double digit yield improvements

- Enhancing global footprint

- Bringing US guests on European itineraries

- Asia

- Quantum deployment to China is very exciting

- Pullmantur

- Cusp of turning an important corner. Increased focus on Latin America.

- Controlling costs

- Moderate growth

- 3-5% average compound growth is appropriate

- Quantum of the Seas

- 2Q

- Better close-in pricing for Europe and Asia

- Caribbean- highly promotional; ticket revenue yields down YoY

- Onboard revenue yield: +3% (10th consecutive quarter of onboard growth) - beverages packages and internet service drove the gains

- NCC - better than expected, mostly timing related; balance of costs will be spent in rest of year

- Booking environment: significantly higher YoY. Booking window continue to expand. load and APD are up for rest of 2014.

- Early 2015: load and APD higher YoY

- Caribbean: very price sensitive. Have implemented various promotions. Expect Caribbean yield declines but see some improvement on Oasis ships.

- Europe:

- Guests paying 20% more (in-line with our pricing survey)

- Less supply to sell

- Black Sea sailings pressured by conflicts in region

- Med sailings doing well

- Q3 guidance

- Positive trends in Europe, China, and Alaska

Q & A

- Caribbean: closer to inflection point; more pressure on 7 night and shorter itineraries.

- Caribbean got quite a bit worse from 1Q to 2Q but has stabilized since.

- Caribbean: 1Q 2015 comps will be harder than rest of quarters

- Either higher dividends or stock repurchases in future

- China: proven to be a successful market but it is fairly young; but investments have been costly, as with all new markets. Still in the 1st inning.

- 2015 NCC: general commitment to cost cutting but there will be inflation pressures

- Net Yield outlook: +4% on average is a little on the high side

- Q4 yield growth: relatively consistent on bookings environment.

- New onboard planning tool: too soon to see how CruisePlanner will perform but doing well on Quantum

- FY yield target unchanged due to rounding

- China vs Caribbean: economically, Quantum should perform as well in China as in Caribbean (more costs but also more onboard revenues)

- Demand will drive the profitability change. Capacity has been set for the next 3 yrs.

- Onboard revenue: all categories up. Doubled efforts on shore excursions.