This note was originally published at 8am on July 10, 2014 for Hedgeye subscribers.

“Prepare. Perform. Prevail.”

-Dave Tate, EliteFTS

In what feels like a lifetime ago now, I owned a human performance and nutritional consultation company. The work was rewarding, but not from a pecuniary perspective.

Designing transformative programs for dedicated collegiate athletes and prospective professional athletes, bodybuilders and Olympians was certainly gratifying. Rep counting for middle-aged housewives (in what invariably devolved into pseudo-therapy sessions)…not so much.

Unfortunately, only one of those demographics generally had the discretionary dollars to spend to keep us a going concern.

Because broke college kids don’t have much in the way of a food or supplement budget and certainly can’t afford high frequency, hormonal profiling, we had to resort to a little empirical “bro-science” to gauge recovery and the subsequent prescription of workout intensity.

Q: How do you know if cortisol levels are muted, the central nervous system is piqued, and the overall hormonal milieu is primed for hardcore training and positive physiological adaptation…in ~5s and at no cost?

A: Wake up and pick up something heavy.

If your grip strength is there right out of bed, it’s almost assured the body is recovered and ready for positive stress.

Another underused training technique effective at jumpstarting progress in advanced lifters is targeted use of eccentric training. The eccentric part of a lift can generally be thought of as the “down” part of the lift (think lowering the bar when bench pressing)

Muscle contraction during the eccentric portion is stronger, allowing you to use more weight – resulting in greater muscle soreness and, if employed correctly, faster strength & hypertrophy gains.

The majority of lifters and coaches only focus on the concentric portion of the lift – which, in investment speak, is analogous to simply being long beta. Learning when and how to manage the eccentric (down) part of the lift cycle is where training alpha is generated.

Back to the Global Macro Grind...

In our 3Q Macro Themes call tomorrow we’ll lay out the detailed case under our expectation for a sequential slowdown in consumption growth in 3Q. The punditry of the Early Look prose typically carries a tendency towards intentional overstatement, so it’s worth emphasizing that we’re not making a recession call or even a call for an overly protracted deceleration (yet).

As the current expansion matures, however, occasional detachment from the myopia of every market moment and consideration of where we are in the longer cycle can be a useful exercise.

Because we have a self-imposed 900 word limit on the morning missive and alliteration has yet to steer me wrong, we’ll use the 3-D’s of Duration, Demographics, & Deleveraging as the conceptual framework for contextualizing the prospects for the present cycle:

Duration (of Expansion): The mean duration of expansions over the last century is 59 months. Inclusive of July, the current expansion stands at 62 months. We continue to think the reality of the ticking expansion clock weighs into the Fed’s current policy calculus – they need to get out of QE if only to give themselves the opportunity to (credibly) get back in if need be. Stopping QE while the fundamental data is supportive implies that QE was (at least in part) effective in its objective. Perma-QE, however, is a de facto admission to the market of its ineffectivenss, leaving it largely impotent as a forward policy tool.

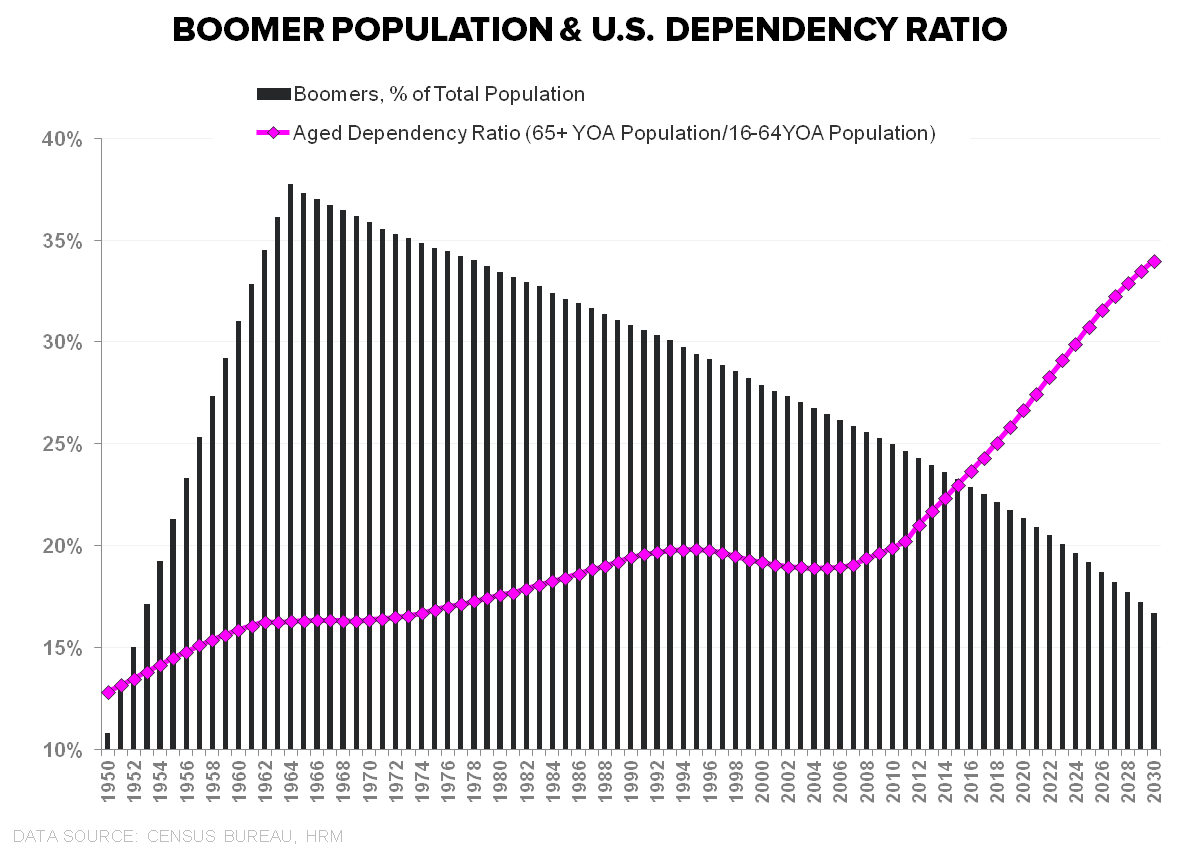

Demographics: Growth in the working age population peaked circa 2000 and won’t turn again for another ~10 years and the aged dependency ratio (the >65YOA population in relation to the 16-64YOA population) will continue to rise well beyond that. With labor supply in secular deceleration, productivity gains will have to shoulder an increasing share of the load to support trend growth in real gdp/potential gdp. Real Wage Growth may benefit from tighter labor supply and productivity driven demand for labor - but that remains an “if” and, either way, higher entitlement spending and debt service costs will likely sit as an offset to gains in real income.

Deleveraging: Household debt-to-GDP currently sits at 77.2%, down from the March 2009 peak of 95.6% according to the latest Fed Flow of Funds data. Rates remain pinned at historic lows, for now, and debt growth remains below income growth so (assuming borrowers want to borrow and creditors lend) credit could support consumption growth over intermediate term. However, given the initial debt position and zero bound rates, we certainly aren’t in position to jumpstart a repeat of the prior credit based consumption cycle.

The simple reality of the last 30+ years is that, with the Baby Boomers (born 1946-1964) entering prime working age (24 – 54) alongside the secular increase in female labor force participation, we had the largest bolus of people ‘ever’ matriculating through their peak years of discretionary income with peak leverage on that (peak) income – all of which also happened to occur on the right side of a multi-decade interest rate cycle which provided a steady tailwind to asset values (via lower discounting) and offered self-reinforcing support to the credit cycle as rising collateral values supported capacity for incremental debt.

No central bank liquidity deluge can effectively replicate that.

So, is it time to start managing the eccentric part of the macro cycle?

Probably not quite yet. Viewing economic cycles as periodic functions, balance sheet recessions are generally characterized by longer periods (slower recoveries) with lower amplitude. So, it’s probable the muddle continues for a while longer with recurrent, short-cycle oscillations in growth for the Macro Marauders of Hedgeye to continue to attempt to front run.

The “3D” style thinking above isn’t particularly new or novel, but there’s a lot of economic gravity embedded in those realities. Their recapitulation also provides an effective counterbalance to the latest Fed projections which call for GDP to grow in excess of potential output for the next 2.5 years – which is effectively a call for an accelerating recovery over the next 30 months and an implicit expectation for the 3rd longest expansionary period in a century.

Do you take their word for it or are we #PastPeak in the current cycle?

We don’t know, exactly, but our model is dynamic and data dependent… and our 4Q Macro themes are still up for grabs.

In the meantime, we’ll continue to work to evolve and fortify our process for risk managing the eccentric.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signal in brackets) are now:

UST 10yr Yield 2.49-2.59% (bearish = bullish for bonds)

RUT 1165-1189 (bearish)

USD 79.64-80.19 (bearish)

Pound 1.70-1.72 (bullish)

Brent Oil 107.23-111.37 (bullish)

Gold 1315-1346 (bullish)

Winter is Coming! Prepare. Perform. Prevail.

Christian Drake

Macro Analyst