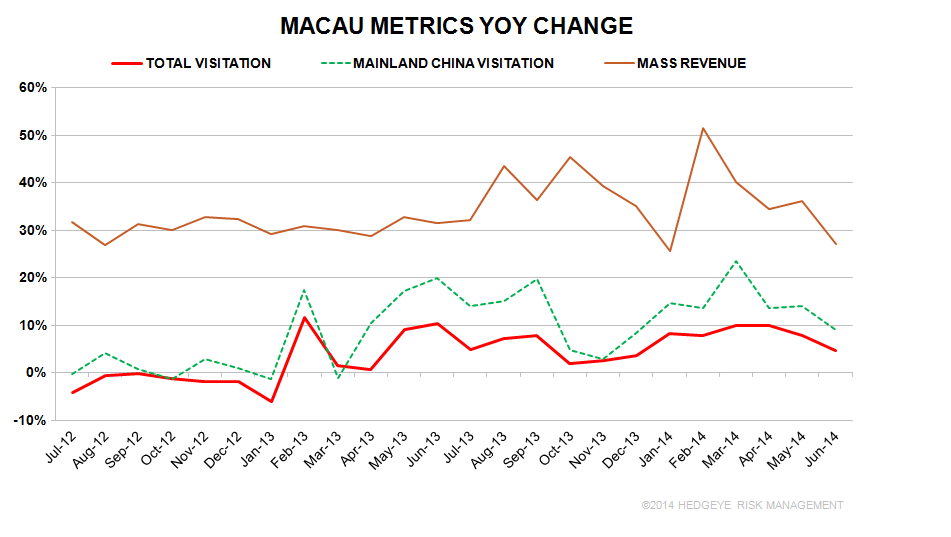

Chart Du Jour: June mass revenue growth and visitation seem to have begun their descent – in-line with our mass deceleration Macau thesis.

- June Mass growth was below expectations at +27% and with the release of the Macau visitation figures today, we can say the same about visitation

- As analysts continue to eschew VIP in favor of mass – emphasizing 30% growth rates in 2H 2014 – we take the other side. Relative to sentiment, VIP is starting to look more stable while mass appears in deceleration mode.

- We outlined our mass deceleration thesis in our 06/13/2014 note “MACAU: HANDICAPPING MASS DECELERATION”. We reiterate our positive long term outlook for Macau but caution investors that YoY mass revenue growth could decelerate into the mid to high teens by year end. Indeed, the deceleration appears to have already begun.