TODAY’S S&P 500 SET-UP – July 21, 2014

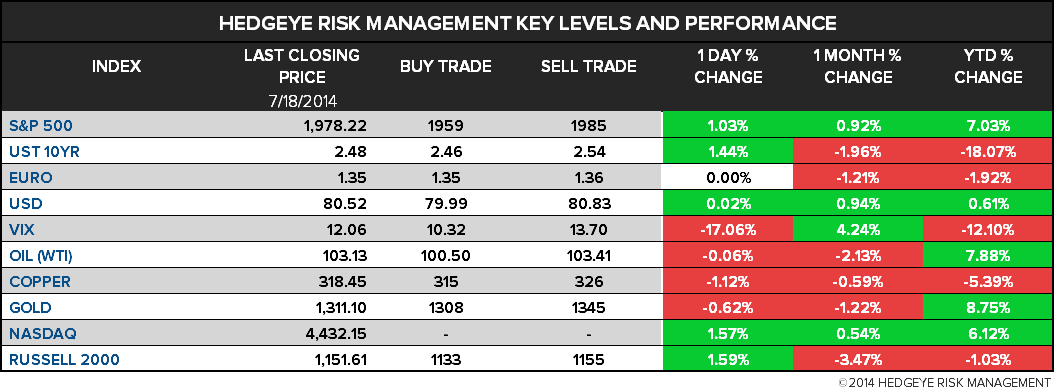

As we look at today's setup for the S&P 500, the range is 26 points or 0.97% downside to 1959 and 0.34% upside to 1985.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.00 from 2.00

- VIX closed at 12.06 1 day percent change of -17.06%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Nat Activity Index, June (prior 0.21)

- 11:30am: U.S. to sell $26b 3-mo. bills, $24b 6-mo. bills

GOVERNMENT:

- Senate in session; House schedule TBA

- President Obama meets with Hispanic Caucus on immigration

- 12:30pm: Transportation Sec. Anthony Foxx at Natl Press Club

- WASHINGTON WEEKLY AGENDA

- U.S. ELECTION WRAP: Voter Attitude Shift on Immigration; Kochs

WHAT TO WATCH:

- Russia’s Severstal sells U.S. steel plants for $2.3b

- Reynolds loss in $23b smoker verdict likely to be cut

- Murdoch said to mull Sky proceeds to boost Time Warner bid

- Elliott Management takes over $1b stake in EMC Corp.: WSJ

- McDonald’s, Yum suspend orders from Chinese meat supplier

- Capital Research sells most of Allergan stake, WSJ reports

- U.K. prosecutors said close to opening FX-rigging probe

- General Motors tells dealers to halt sales of some Cadillacs

- Air Force examines anomalies as SpaceX seeks launch work

- Trinity guardrail whistle-blower case results in mistrial

- Gilead drug combination cures Hepatitis C in HIV patients

- Perrigo, Actelion lead tax-relief targets for U.S. drugmakers

- Putin says MH17 crash shouldn’t be used for political aims

- Bloody battle spurs diplomatic efforts to end Gaza conflict

- Court bars Nokia India from Chennai unit sale without approval

- Google mulls transforming NYC payphones into Wi-Fi hot spots

- Finance industry bonus suffering in poll as rev. disappoints

- Tesco replaces Clarke as CEO as grocer warns on profit again

AM EARNS:

- BB&T (BBT) 5:45am, $0.75

- Halliburton (HAL) 7am, $0.91 - Preview

- Hasbro (HAS) 6:30am, $0.36 - Preview

- Manpowergroup (MAN) 7:30am, $1.33

- SunTrust Banks (STI) 6am, $0.77

PM EARNS:

- BancorpSouth (BXS) 5pm, $0.33

- Brookfield Canada Office Properties (BOX-U CN) 5pm, C$0.41

- Brown & Brown (BRO) 4:30pm, $0.41

- Cadence Design Systems (CDNS) 4:10pm, $0.20

- Canadian National Railway (CNR CN) 4:01pm, C$1.00 - Preview

- Chipotle Mexican Grill (CMG) 4:02pm, $3.09

- Crown (CCK) 5:03pm, $1.00

- CYS Investments (CYS) 4:05pm, $0.33

- Hexcel (HXL) 4:06pm, $0.55

- Netflix (NFLX) 4:05pm, $1.15

- Rambus (RMBS) 4:05pm, $0.15

- Rent-A-Center (RCII) 4:32pm, $0.37

- Sanmina (SANM) 4:05pm, $0.47

- Steel Dynamics (STLD) 6pm, $0.30

- Texas Instruments (TXN) 4:30pm, $0.59

- Waste Connections (WCN) 4:05pm, $0.52

- Woodward (WWD) 4pm, $0.60

- Zions Bancorp (ZION) 4:10pm, $0.45

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

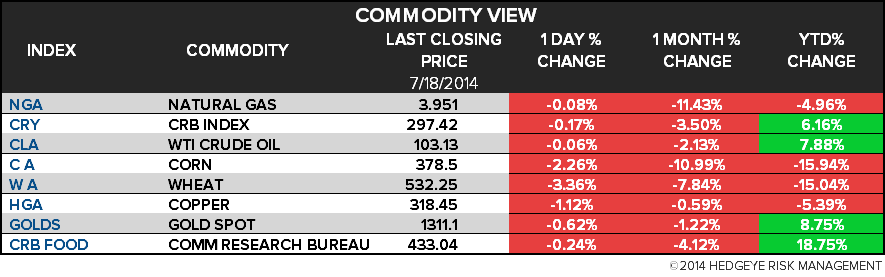

- Brent Steady as Supply Seen Safe Amid Russia Standoff; WTI Falls

- Hedge Funds Cut Bullish Gold Wagers as Rally Snaps: Commodities

- Corn Slumps to Four-Year Low as Global Supplies Seen Increasing

- Gold Gains in London as Unrest Weighed Against U.S. Outlook

- Speculators Cutting Bullish Oil Bets Miss Ukraine Rally: Energy

- Morgan Stanley Hires Former UBS Commodity Analyst Tom Price

- China’s Copper Exports Rise to 15-Month High Amid Qingdao Probe

- Two Indonesian Ore Miners Resume Concentrate Exports After Ban

- Nickel Reaches Lowest Price in Almost Four Weeks on Supply View

- McDonald’s, Yum Suspend Orders From Chinese Meat Supplier

- Gold Diggers Revive French Exploration as Prices Drive Hunt

- U.K. Gas Extends Declines as Ample Supplies Offset Ukraine Risk

- Russia Sold 300K Mt of Wheat to Indonesia Since May: Minister

- Iran Seen Keeping Oil Sales Steady as Nuclear Talks Extended

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team