THE HEDGEYE EDGE

BOBE is a stodgy, old company that has flown under the radar for far too long.

For those unfamiliar, Bob Evans was founded in 1948, when the company’s namesake began making sausages on his farm in southeastern Ohio. The business was incorporated in Ohio in 1957 and became publicly traded in 1963. Bob Evans Farms operates in two primary businesses: Bob Evans Restaurants and Bob Evans Farms Foods. Bob Evans Restaurants owns and operates 562 full-service restaurants in 19 states across the U.S., primarily in the Midwest, mid-Atlantic and Southeast. BEF Foods produces and distributes a variety of refrigerated and frozen food items to more than 30,000 retail locations across the U.S. and Mexico.

We’ve followed BOBE on and off over the years, but have never really gotten behind the story – until now. The level of activism in the restaurant industry has never been more rampant. In the past year alone, we’ve seen CBRL, DAVE, DRI, BJRI and BOBE attract largely uninvited attention from these investors. In the case of BOBE, we believe Sandell Asset Management’s attention was warranted. All told, BOBE has a long history of mismanagement, evidenced by flawed strategic rationale, an excessively bloated cost structure and severe underperformance relative to peers. Fortunately, its poor operating performance presents a tremendous opportunity.

We believe Sandell has identified significant, largely feasible, opportunities to enhance shareholder value. Particularly, we see tremendous upside value in selling the foods business, transitioning to an asset light model and refocusing capital allocation.

TIMESPAN

INTERMEDIATE TERM (TREND) (the next 3 months or more)

Don’t get us wrong – it was a disastrous year for Bob Evans Farms and its management team, but that precisely the point. We don’t like the company for what it is, we like it for what it could be. Sandell has been working tirelessly to unlock significant value and if BOBE reports another quarter similar to the one it just did, we won’t have to wait much longer. We believe BOBE’s inherent value and the upcoming proxy fight should keep the stock afloat over an intermediate-term duration. BOBE holds its Annual General Meeting on August 20th. This will be a monumental moment for the company and its shareholders.

LONG-TERM (TAIL) (the next 3 years or less)

We have a ton of respect for Sandell and the work they’ve done. In fact, we believe that, over time, they have uncovered far more than they originally set out to. As a result, there is now an opportunity for them to capture bountiful, low hanging fruit that will immediately change the business for the better. We believe in Sandell’s resolve and while the street is seemingly betting against them, we’ll gladly take the other side of the trade. If Sandell is successful in their efforts to effect change, we see at least 65% upside to BOBE shares over the next two years.

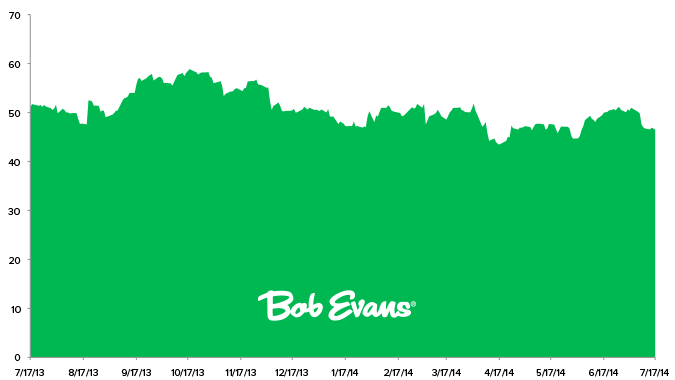

ONE-YEAR TRAILING CHART