Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: May Housing Starts & Permits

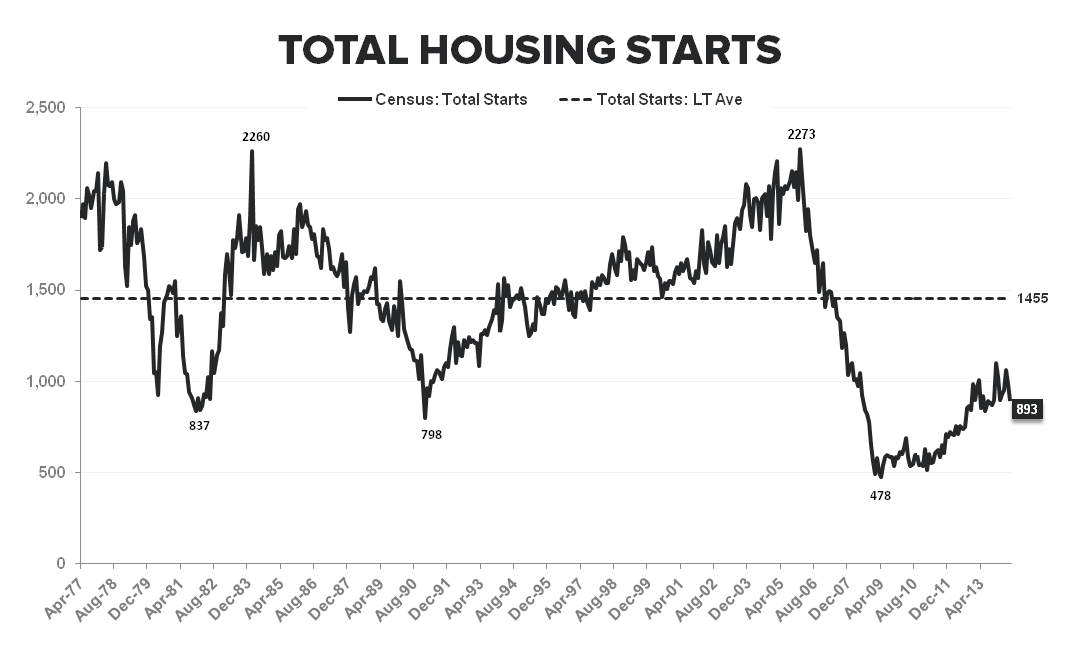

The Census Bureau released its monthly Housing Starts & Permits data for June this morning. The big takeaway is this: No Growth. Incidentally, this is the same

takeaway as last month.

This data is a splash of cold water on yesterday's improved HMI reading as the two have historically not exhibited a lead/lag relationship.

- Total Starts - Declined -92K MoM (-9.3%), back below the 900K level to 893K with both single and multi-family starts declining MoM. Total Starts for May were revised lower to 985K from 1001K.

- Single Family - Declined -57K MoM (-9.0%) to +575K while permits increased +16K (+2.6%) sequentially to +631K. The soft'ish starts number is not particularly surprising given permits have been running below starts YTD.

- Multi Family - Starts down for a 2nd straight month, declining -35K MoM (-9.9%) to 318K (from 353K in May and 414K in April). MF permits declined sequentially as well, down -58K MoM to 332K – the lowest level since August of last year.

NAHB HMI vs Starts: Builder confidence has decoupled from the reality of actual new construction activity the last few months. As we highlighted yesterday, builder optimism led the upside in the NAHB HMI gain in July with the forward expectations component registering a disproportionate increase. With permits running largely flat with starts YTD (& declining in the latest month) the upside for starts over 2H appears somewhat constrained and more likely that confidence re-couples to starts than the converse.

As a reminder, there are three factors principally responsible for the ongoing weak performance for housing. First, QM rules that took effect early this year are having a suppressing effect on credit availability. Second, institutional investor demand for properties is waning sharply. Third, affordability dynamics have swung sharply; whereas 12-18 months ago there was a strong asymmetry favoring homeownership, today renting vs owning are close to a toss-up.

About Housing Starts & Permits:

The US Census Bureau records the number of new housing units that have obtained permits for construction and those that have begun construction. This data includes new buildings intended primarily as residential units. The US Census Bureau defines a start as, “Start of construction occurs when excavation begins for the footings or foundation of a building.”

Joshua Steiner, CFA

Christian B. Drake