“If you leave the smallest corner of your head vacant for a moment, other people’s opinions will rush in from all quarters.”

-George Bernard Shaw

Perhaps the most challenging part of the investment business is to control your own views. After all, the world today is replete with conflicting opinions and research. Some of it is very insightful, but the vast majority of these opinions are what we would characterize as the noise, versus the signal.

One point most of us can agree on is that when successful investors speak with conviction, it's worth giving them a little room in our ever so full minds. In this vein, we thought that Stan Druckenmiller of Dusquesne and Soros Capital fame, had some apropos comments at the Institutional Investor “Delivering Alpha” conference yesterday.

Here are a few of Druckenmiller’s best quotes:

“I am fearful that today our obsession with what will happen to markets and the economy in the near term is causing us to misjudge the accumulation of much greater long term risks to our economy.”

“I hope we can all agree that once-in-a-century emergency measures are no longer necessary five years into an economic recover.”

“There is a heated debate as to what a 'neutral' funds rate would be. We should be debating why we haven't moved more meaningfully toward the neutral funds rate if for no other reason so the Fed will have additional weapons available if the outlook darkens again.”

His last point is perhaps most spot on. Five years into the “recovery”, why are we still at extreme, once in a century emergency policy measures? And given that, what, if any, options do policy makers have if the economy does sour?

Inquiring and non-vacant minds want to know Dr. Yellen!

Back to the Global Macro Grind...

To her credit, even if she didn’t give us any real insight on her strategy as it relates to monetary policy, Dr. Yellen did give us some decent stock advice in her recent congressional testimony. Specifically, she said that she believed valuations for biotech and social media stocks were stretched.

While we would never recommend shorting a stock on valuation (sorry Dr. Yellen!), we absolutely agree with her call that certain social media stocks are overvalued. In fact, our top pick on the short side is and continues to be YELP.

On that front, yesterday a key risk to the short idea disappeared as Yahoo effectively indicated they would use much of their Alibaba proceeds to return cash to shareholders. While the company didn’t specifically say they wouldn’t buy YELP, buying YELP would certainly be inconsistent with returning cash to shareholders (to say the least).

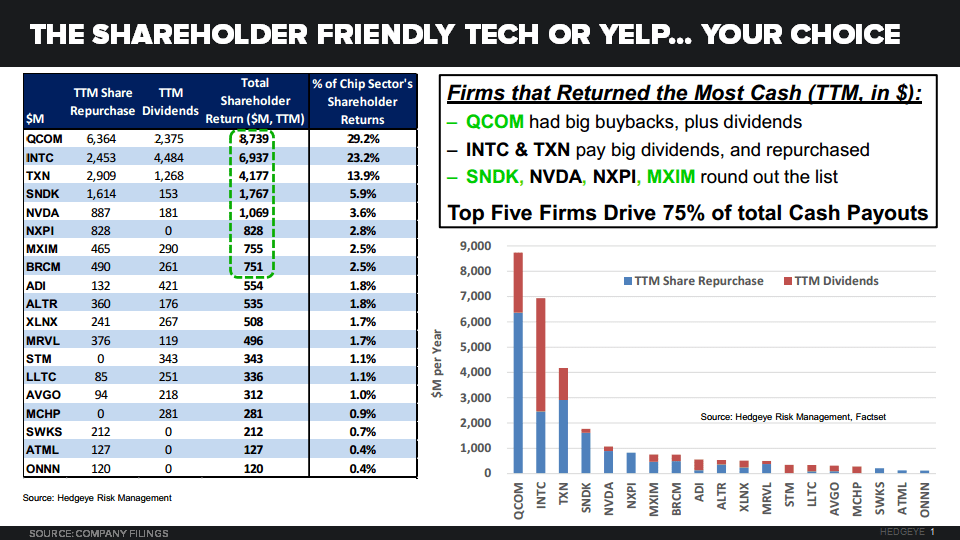

Speaking of returning cash to shareholders and technology, we recently launched our newest sector, Semiconductors, led by Craig Berger. A key theme of his launch was that there is a subset of semi-conductor stocks that have been returning cash to shareholders and will continue to aggressively do so.

Yesterday, Intel (INTC) reported strong numbers, which was capped with an additional $20 billion added to its stock buy back program. Intel, certainly, knows what to do with the Fed’s low interest rates! While Berger remains cautious on the outlook for INTC because of the PC market (in effect: can things get better from here?), he continues to like this theme of owning companies in the semiconductor space that will increase dividends.

In the Chart of the Day below, we highlight this very investable theme with a slide from our Semiconductor launch presentation, which shows the companies that historically have returned the most cash back to shareholders. If you’d like to see Craig’s proprietary analysis on which companies are going to raise dividends next, or to set up a time to chat with him, please email .

Getting back to the global macro grind, a key derivative play of semiconductors doing well is of course to be long Taiwan on a country basis. My colleague Darius wrote the following back in early June and it holds today:

“While it’s hard to argue in favor of the predictability of YTD gains, Taiwan does have idiosyncratic country risk factors that support allocating capital to this market at the current juncture. Specifically, improving GIP fundamentals support chasing Taiwanese equities up here – particularly amid heightened prospects for M&A activity in the global semiconductor space. It’s worth noting that the Tech sector accounts for a whopping 46% of TAIEX market cap, with semiconductors alone accounting for 23%.

Contrary to Brazil, it’s particularly difficult to find a meaningful economic indicator in Taiwan that isn’t accelerating on both a sequential and trending basis. While headline inflation is indeed accelerating, it’s accelerating off of extremely low levels and does not warrant any attention from the central bank – especially with WPI trends being so subdued.”

While Taiwan has been a strong market in the year-to-date, this morning might actually offer an opportunity to get in at a discount as Taiwan Semiconductor is trading down almost 6% on news that it is likely to lose some next generation chip orders in 2015 from Apple and Qualcomm.

Before you head off into the trading day and eventually the weekend, we did want to offer one last quote that goes back to the start of our note and that we hope will find a spot in your mind:

"This [Federal Reserve Act] establishes the most gigantic trust on earth. When the President [Wilson] signs this bill, the invisible government of the monetary power will be legalized....the worst legislative crime of the ages is perpetrated by this banking and currency bill."

-Charles A. Lindbergh, Sr. , 1913

Indeed Mr. Lindbergh, indeed.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research