At best, higher housing prices helped stabilize locals gaming revenue. In the face of potentially lower prices going forward, gaming demand could dry up – not good for BYD and Station Casinos.

CALL TO ACTION: DRY DEMAND IN THE DESERT

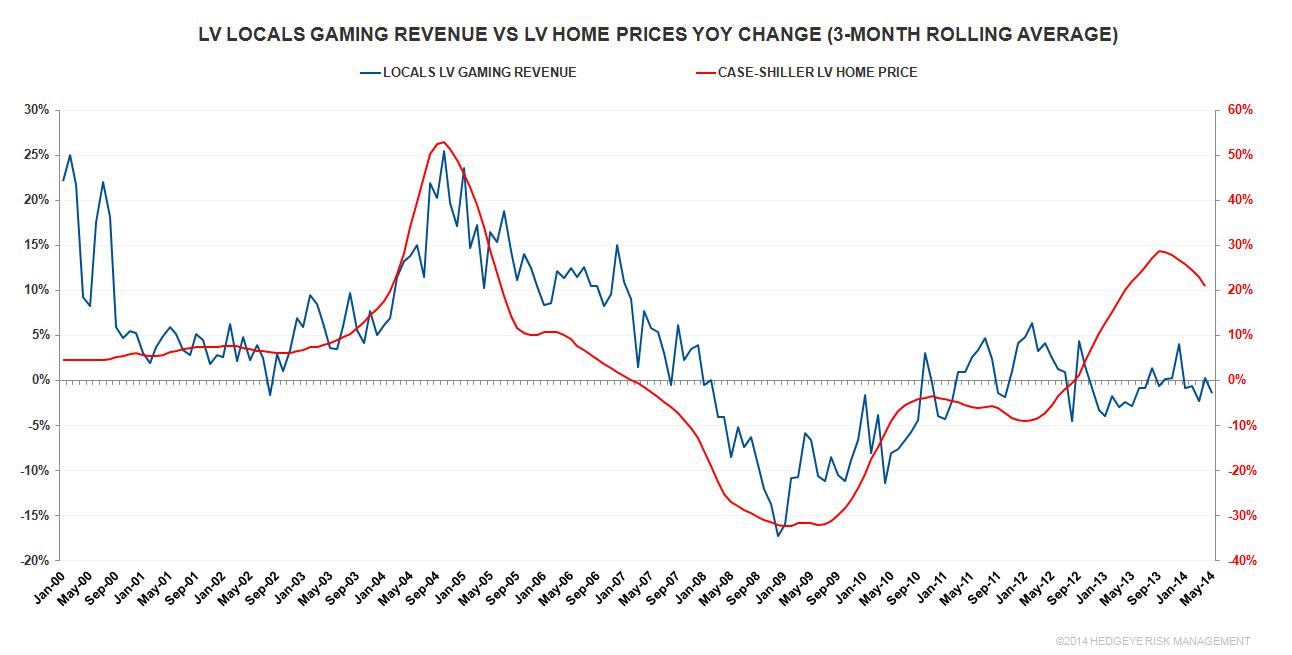

Las Vegas Locals gaming revenue have been stagnant for a while despite a pickup in home prices, but at least had stabilized. It seemed attributable to a delayed wealth effect – housing prices proved to be the most statistically important driver of Locals gaming revenues during the boom. However, falling sales volume – a demand indicator – since July may have been indicative of a weak overall housing environment despite higher prices. Indeed, Q1 locals gaming revenues were disappointing after months of stability and the first 2 months of Q2 deteriorated further.

Our Hedgeye Financials Team sees downward pressure on home prices as they usually lag demand by 12-18 months. The recent gaming revenue performance and declining prices would not be good for BYD and Station Casinos. Historically, Vegas home prices have a 70% correlation with Locals gaming revenues. At the very best, the upcoming housing environment should prevent any Locals casino recovery. At worst, the already fragile Local customer will tighten her purse strings even more.

EVIDENCE:

The Phoenix and Vegas housing markets have mirrored each other in the recent housing bubble and recovery. While Phoenix home prices have remained relatively robust, home sales have declined since last July. A number of comments from an ASU report on the Phoenix home market in May were quite disturbing:

- Total single family homes sold fell 19% YoY with those under $150k plunging 37% YoY

- The percentage of residential properties purchased by investors continued to decline from 16.3% in April to 16.1% in May.

- Weak demand from 1st time home buyers

- Outlook:

- Some home sellers appear to be cancelling their listings and waiting for another time when buyers have a greater sense of urgency.

- Many families are choosing to stay in their homes longer than they used to 10 to 15 years ago.

- The mix of homes that are selling has changed a lot in the past 12 months. There are fewer distressed homes and far fewer homes priced under $150,000. This tends to push the averages and medians upward even if prices are stable.

Las Vegas home demand is not much better. According to GLVAR, Southern Nevada total home sales (single family, condos, townhomes) declined double digits every month since January 2014. Furthermore, in June, short sales – when lenders allow borrowers to sell a home for less than their mortgage obligation – spiked to 10.8% of all existing local home sales – up from 7.9% in May.

CONCLUSION:

Housing is a critical component of the health of the Las Vegas Locals gaming market. With sluggish top-line gaming revenues thus far in 2014, more weakness may lie ahead for the Locals market as any support from rapidly rising home prices is taken out. Of the publicly traded gaming operators, BYD is most sensitive to the Locals environment.