Takeaway: YUM has been one of the best performers in the restaurant space over the past 6 months (+6.1%) and is a name we continue to prefer on the long side. Look for strength in China to dispel any remaining fears and the company to solidify its runway for +20% EPS growth in 2014.

Investment Thesis Overview

Despite being a strong performer to-date in 2014, YUM shares have room to run. We see fair value between $90-100/share.

YUM continues to be one of our favorite longs in the big cap QSR landscape as we believe the company is well positioned to capitalize on a substantial long-term growth opportunity in China and other emerging markets. Looking near term, we expect easy comps, notable margin expansion and positive earnings momentum to drive performance throughout 2014. As we’ve stated before, the magnitude of this performance will depend heavily upon the trajectory of the recovery in China. While management’s guidance of 40% operating profit growth in China may be aggressive, we believe they have multiple levers at their disposal to reach greater than +20% EPS growth in 2014.

Domestically, Taco Bell continues to take share from competitors and drive incremental sales through innovation. The chain recently launched its national breakfast rollout, supported by a strong advertising campaign. Early signs indicate that breakfast has been selling well and franchisees are supportive of the move. We believe breakfast represents a material opportunity for Taco Bell, even if they are only able to capture a small piece of the market. Taco Bell has significant brand momentum and continues to carry the domestic business. We expect to see a renewed level of focus at both the KFC and Pizza Hut brands throughout the year, but don’t expect to see any material improvement as they continue to lose share to competitors.

In addition to its strong positioning in emerging markets, YUM has three main levers (growth investments, growing dividend, share repurchases) to continually support the stock and drive shareholder value.

Earnings Expectations

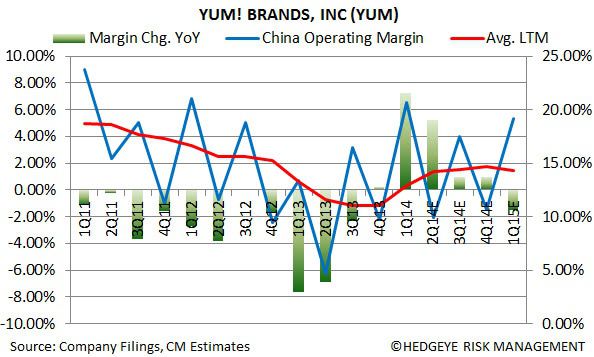

For 2Q14, the street expects revenues of $3.23 billion (+11% YoY), adjusted EPS of $0.72 (+29% YoY), and system-wide same-store sales of +3.3% (led by +11.2% growth in China). We see upside to earnings driven by strong same-store sales and operating leverage in China as productivity initiatives continue to materialize.

Same-Store Sales Trends

System-wide two-year same-store sales look to have bottomed in 1Q14 and we anticipate a recovery from these lows. A recovery in China and momentum at Taco Bell following its breakfast rollout should support meaningful system-wide comp growth throughout the year.

Margins

Strong comp growth and other efficiency initiatives in China should enable the company to improve restaurant level margins and operating margins in the quarter to an extent comparable to 1Q14.

Valuation

YUM is currently trading at 22.00x P/E and 12.03 EV/EBITDA on a NTM basis.

Risks

The quarter, and really the year, relies heavily upon the performance of the China segment. Therefore, the main risk to our thesis is any setback or weakness in this market which would likely be driven by disappointing same-store sales. Over 90% of stores outside China are franchised. As such, the domestic KFC and Pizza Hut businesses are largely irrelevant when looking at the grand scheme of things. A continuation of the underperformance we saw at the Taco Bell brand in 1Q14 would be concerning, though to a much lesser extent than any underperformance in China.

Howard Penney

Managing Director

Fred Masotta

Analyst