RETAIL FIRST LOOK: WMT, KSS, GIL QUICK TAKE

AUGUST 13, 2009

TODAY’S CALL OUT

Here are some key call outs from this morning’s flurry of EPS releases.

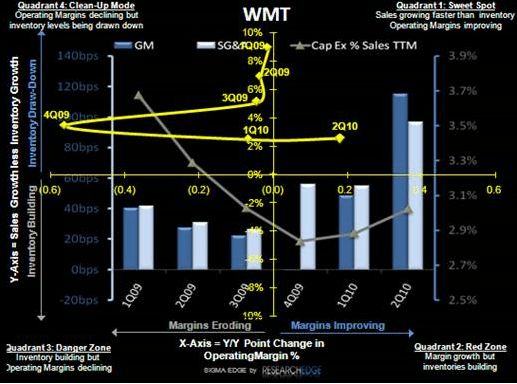

Wal*Mart: Key surprise here is same store sales which came in at -1.2% for the US without fuel and -1.9% with fuel while the street was generally expecting a +1% - 1.5% comp. One of the few details in the press release alludes to deflation (a trend that has been consistently negative for all consumables retailers in the qtr). Offsetting a slightly weaker sales number was a slightly better operating margin performance. Inventories were also very well controlled, declining by 4.3% vs. a sales decline of 1.4%. Check out the visual in the SIGMA chart below. Overall, results were very much inline with the high end of the guidance. This is the consistency that people pay for. After beating the street's EPS estimate by $0.03 and earning at the high end of it's guidance, WMT guided Q3 to $0.78-0.82 vs. Reuters $0.80 and full year $3.50-3.60 vs Reuters $3.53, tightened from previous $3.45-3.60.

One of the financials that bugged me initially is capex, which is showing a pick up from the bottom. Almost all the growth is coming outside of the US which is the only place left to expand. Also some step up in a worldwide systems initiative to create common platforms. In the end, it’s probably not worth getting bent out of shape about – as the best companies should be increasing investment levels during recessionary periods. In the end, a net positive report from WMT.

Kohl's: Q2 release and Q3 guidance may be perceived as a mess, but only if you want to really believe their guidance. This is basically what Macy's did yesterday. Lowball, raise, raise again, beat, and then guide below the Street. If we use M as a proxy then the Street will look right through the guidance. Kohl's comp guidance at -3 to -5% is a bit laughable if you consider they just reported a positive comp in July (which is the month with the negative hit from BTS). Sales up 2%, inventories flat. The SIGMA trajectory here is one of the best out of the major retailers. This path is usually tough to reverse.

GIL: While the clean EPS of $0.32 is a bit lighter than the headline of $0.37, the company still beat consensus by $0.03. Sales missed by 10% but gross margins beat meaningfully, which was due to Cotton cost benefits being realized a quarter earlier than we thought and GIL pumping its volume through tighter capacity. We expected this in 2H09 – though it is showing up a quarter early. I still question why this company needs to exist beyond its core US screenprinting business. But consistent with our quality vs. junk theme for 2010, this is one you can’t bet against until the stats start to visibly align in another 2 quarters.

LEVINE’S LOW DOWN

Some Notable Call Outs

- Bloomingdales’ sales are still lagging the overall Macy’s corporate average, but management indicated trends did improve during the second quarter. Additionally, Bloomingdales is said to be outperforming its peer group of higher-end department stores. Most interestingly, markets with tourist exposure (i.e NYC) performed a little better in the 2nd quarter. Macy’s flagship store in Herald Square was called out as having a “great trend” over the past couple of weeks.

- Based on comments from the CEO, it does not look like LIZ is looking to shed any additional assets at this time. When asked point blank on the company’s 2Q conference call if there were any brands that could be potentially shelved or sold, the answer was a definite “no”. CEO McComb reminded everyone that the company’s strategic reviews have been completed and there will be no further changes to the brand portfolio at this time.

- Perhaps this is the beginning of a trend. On August 18th, Seattle residents will vote on a 20 cent plastic bag tax, which would impact grocery, drug, and convenience stores. The tax, which is generally driven by environmental motives, was originally passed last year but was put on hold after an opposition group (backed by Dow, ExxonMobil, and bag manufacturers) collected enough signatures to put the measure to a ballot. Interestingly, IKEA began phasing out plastic bags in the U.S. by instituting a 5 cent charge per bag and immediately saw a drop in usage by 92%. Eventually, the furniture/home retailer phased out plastic bags completely by the end of 2008.

MORNING NEWS

-Apparel and Textile Imports fall 10.3% in June - Imports of apparel and textiles to the U.S. declined 10.3% in June, but still represented the highest monthly volume gain for the combined import categories so far this year. Vietnam, Pakistan and Bangladesh were the only countries that showed overall growth in apparel and textile imports in June. Vietnam increased shipments 29% driven by a sizable growth in textiles. Shipments from Pakistan increased 8.5% and imports from Bangladesh were up 2.2%. Shipments of textiles and apparel from China fell 4.2%. The figure was held down by declining textile import levels. Apparel shipments from China, however, increased 16.2%. Honduras had the largest textile and apparel import declines (affected by the military coup at the end of June that created political turmoil) posting a decrease of 29.3%. The top five apparel suppliers to the U.S. in June were China, Vietnam, Bangladesh, Honduras and Indonesia. China was also the top textile supplier, followed by Pakistan, India, South Korea and Mexico. The nation’s trade deficit widened to $27 billion in June from $26 billion in May, as oil import volume and prices increased. <wwd.com/retail-news>

-WTO finds China guilty of trade violations again - A World Trade Organization panel said Wednesday that China disobeyed trade rules by creating barriers to imports of U.S. books, music, videos and movies, a warning to Beijing over its handling of intellectual property and distribution requirements. It is the second recent ruling in which the WTO has sided largely with the U.S. and criticized China for inadequate intellectual property rights enforcement and protection. <wwd.com/retail-news>

-Charming Shoppes sells credit card operations - ADS and Charming Shoppes (CHRS) announced a long-term agreement where Alliance Data will assume operation of Charming Shoppes' private label credit card programs on an ongoing basis as well as acquire the credit card files and service center operations associated with Charming Shoppes' branded card programs. Alliance Data expects the transaction to close by the end of the year, subject to attaining certain customary regulatory approvals. Under terms of the agreements, Alliance Data will assume the operation of the Lane Bryant, Fashion Bug and Catherines credit card program, portfolio and securitization master trust, which combined represents 4.5M active accounts generating $680M in annual credit sales and $500M in account receivables. <streetaccount.com>

-Liz Claiborne Inc. has promoted Chris Kolbe to the position of president, chief merchant officer of Lucky Brand Jeans - Liz Munoz remains president, creative director of Lucky Brand Jeans. Kolbe will be responsible for all product design concepts, merchandising, manufacturing and planning. He begins in this new role on Sept. 1 and will be based at the brand’s Los Angeles headquarters. Most recently, Kolbe was based in Amsterdam as part of Mexx Europe’s transition management team. There since January, he worked to secure product and merchandising strategies while Claiborne sought a permanent Europe-based team for the Mexx brand. <wwd.com/retail-news>

-The UK Government has unveiled a £3m fund to help regenerate high streets which have been hit by the recession - The fund will be shared between some of England’s hardest-hit areas to allow councils to replace boarded up shops with projects such as art galleries or community learning centres. 57 local authorities have been given grants worth more than £50,000 each to help prevent their high streets becoming ghost towns. <drapersonline.com>

-The top 8 Green Companies according to consumers - 77% of consumers said it’s “somewhat or very important” for companies to be eco-friendly, according to a new study conducted in seven countries, including the U.S. and the U.K. Respondents said although sustainable items cost more than comparable nongreen products, they indicated they would spend more for merchandise that is environmentally friendly in the next 12 months. The “findings reinforce consumers’ desires to be green,” said Russ Meyer, chief strategy officer of Landor Associates, a firm involved in the study, which questioned more than 1,000 participants in each country to rate a predetermined set of brands. Top 8 US brands: Clorox Green Works, Burt's Bees, Tom's of Maine, S.C. Johnson & Son, Toyota, Proctor and Gamble, Wal-Mart, and IKEA. <wwd.com/retail-news>

-Wal-Mart Supplier Li & Fung Net Rises 13% on Cost Cuts, Beating Estimates - Li & Fung Ltd., which supplies retailers including Wal-Mart Stores Inc. and Target Corp., said first-half profit rose 13%, beating estimates, after cutting operating costs. Sales shed 2% as weak consumer demand and some customer insolvencies bit into business. The company said cost cutting helped lift core operating profit 11%. The company also said it has entered into a buying agency agreement with Talbots Inc. Li & Fung said the deal is expected to be completed in September. The companies acknowledged earlier this year that they were in negotiations. <wwd.com/retail-news>

-Maidenform Brands Inc. reported a less-than-expected decline in second-quarter profits and raised full-year guidance Wednesday - Net sales rose 5.9% aided by a 9.2% increase in shapewear sales. Sales at department stores decreased 1.7%, while mass market revenues declined 7.4%. Retail sales remained unchanged although same-store sales slid 6.4%. The company said increased promotional activity and strong sales from its lower-margin mass merchant and other channels pulled gross margins down to 270 bps. Quarterly expenses rose 2.5 % as Maidenform launched licensed programs under the Donna Karan and DKNY brands. <wwd.com/retail-news>

-Coty Inc. and Guess? Inc. Announce Collaboration to Develop and Market New Fragrance Lines - Coty, Inc. announced that it has entered into a license agreement with Guess? Inc, to develop and market new GUESS fragrance lines. As part of the new partnership, Coty will also distribute existing GUESS fragrances, effective January 2010. GUESS is on the pulse of edgy style and flirtatious fashion, and GUESS' ground breaking approach and reputation lends itself perfectly to the passionate and innovative spirit of Coty. With this partnership, Coty is inheriting a notable fragrance house. This collaboration with Coty will provide the perfect platform for GUESS to create innovative, highly desirable and luxurious fragrances that reflect company's image and legacy. <capitaliq.com/news>

-Bakers Shoes steps up efforts to attract global shoppers with new service - Bakers Shoes is taking steps abroad—at least when it comes to its e-commerce site. The online retailer can now sell to consumers in more than 200 countries through a new program from a vendor specializing in international e-commerce for U.S. retailers. <internetretailer.com>

-Designer Robert Geller has created a cobranded denim collection with Levi’s that will hit stores next month - The 11-piece capsule range will be sold in 12 Bloomingdale’s units, on bloomingdales.com and in seven Levi’s stores in New York, San Francisco, Miami Beach, Beverly Hills and Bucktown, Ill., beginning Sept. 10. The collection will be celebrated with a party at Bloomingdale’s Manhattan flagship on Sept. 9, and is featured in the September issue of GQ. The project comes after Geller’s win in GQ’s Best New Menswear Designer in America competition in February. <wwd.com/retail-news>