Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

---

European Financial CDS - Swaps were wider across Europe's banking complex by an average of 12 bps, led by Portgugal's Espirito Santo which widened by 100 bps to 394 bps. Italian and Spanish banks also widened considerably.

Portugal's Espirito Santo Group continues to dominate news flow on the banking front. Both EU and US global bank swaps are widening sharply, and TED Spread is beginning to widen as well. For now, there appears to be no reason to assume that Espirito Santo's problems are widespread, but there is a rising level of uneasiness as investors ask how could this bank, which was under so much scrutiny for the last few years, suddenly be now having such problems? Perhaps more concerning is the fundamental macro slowdown that's taking place in much of the data across Europe.

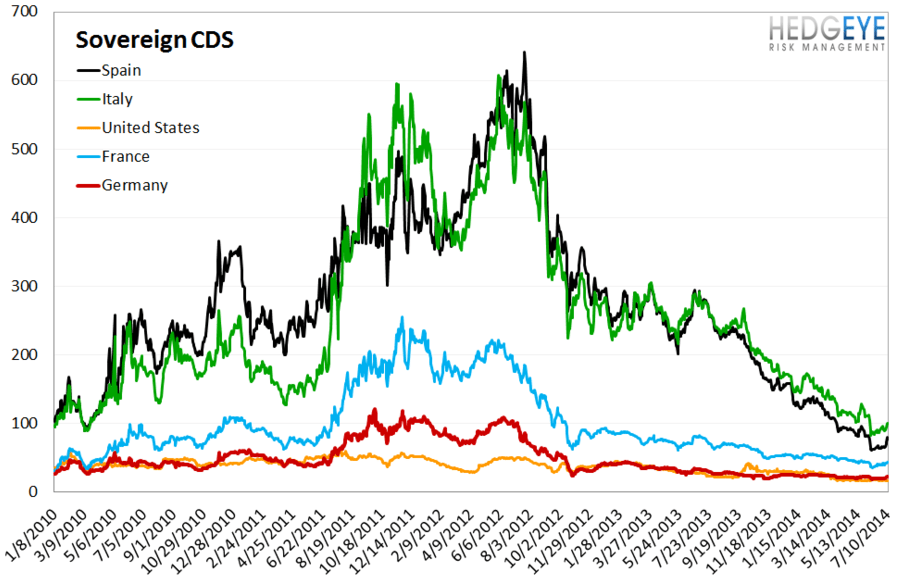

Sovereign CDS – Sovereign swaps widened sharply around the world, except for in the U.S. Leading the charge is Portugal, where CDS widened 65 bps w/w to 198 bps. Caught in Portugal's undertow were Italy and Spain, where swaps widened 10 and 12 bps, respectively. France and Germany were modestly wider at +3 and +2 bps as well. The U.S. tightened by 3 bps to 16 bps and is now 6 bps inside of Germany.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps to 14 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst