TODAY’S S&P 500 SET-UP – July 14, 2014

As we look at today's setup for the S&P 500, the range is 32 points or 0.74% downside to 1953 and 0.89% upside to 1985.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.07 from 2.07

- VIX closed at 12.08 1 day percent change of -4.05%

MACRO DATA POINTS (Bloomberg Estimates):

- No major economic reports expected

- 1:30pm: ECB’s Draghi speaks to EU Parliament Committee

GOVERNMENT:

- Sen. Lisa Murkowski plans to meet Commerce Sec. Penny Pritzker this wk to discuss lifting 39-yr-old ban on crude oil exports

- U.S. Treasury Chief China Coordinator Sharon Yuan, key figure negotiating trade pacts involving banking, securities, travels to Brussels for T-TIP talks

- 8:45am: U.S. Energy Information Administration begins 2-day 2014 Energy Conf.

- 5pm: House Rules Cmte meets on H.R. 5021, highway funding bill

WHAT TO WATCH:

- Shire willing to recommend $53.7b takeover by AbbVie

- Citigroup said poised to end mortgage-bond probe for $7b

- Aecom Technology agrees to buy URS Corp. for $4b

- Whiting to purchase Kodiak for $3.8b to lead Bakken

- Lindt to buy Russell Stover to expand in N. America

- GE’s CFM gets $2.6b American Airlines A320 engines order

- Bank of China leasing unit said to near Airbus, Boeing deals

- Generali sells Swiss private bank BSI to BTG Pactual for $1.7b

- KKR is said to buy stake in BlackGold

- EBay in partnership to stream Sotheby’s sales worldwide: NYT

- Israel strikes back against fire from Gaza, northern neighbors

- T-Mobile says potential Sprint review could last 2 yrs: HSBC

- Singapore GDP unexpectedly shrinks as manufacturing declines

- U.S. gasoline falls to $3.6699 a gallon in Lundberg Survey

EARNINGS:

- Bank of Ozarks (OZRK) 5pm, $0.34

- Citigroup (C) 8am, $1.05 - Preview

- Peregrine Pharmaceuticals (PPHM) 4pm, ($0.07)

- Sirius XM Canada (XSR CN) 4:09pm, C$0.01

- Wintrust Financial (WTFC) 4:01pm, $0.72

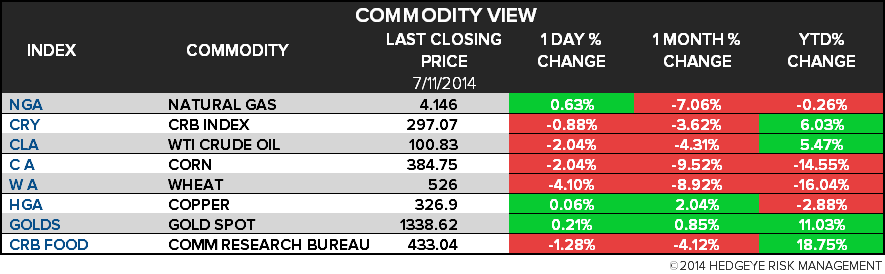

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Palm Oil Enters Bear Market as U.S. Sees Record Soybean Reserves

- Standard Chartered Sues Decheng Owner Chen for $35.6 Million

- Goldman Stays Gold Bear as Bullish Wagers Increase: Commodities

- Sugar Market Reversal Seen by Rabobank as Demand Tops Supply

- Oil Contango Close to Incentivizing Storage of Crude on Tankers

- Zinc Trades at Highest in Almost Three Years as Stocks Shrink

- East Libya Rebels Commit to Keep Open Largest Crude Export-Port

- Sugar Rises as Surpluses Seen Ending in 2014-15; Coffee Advances

- Nickel Market Seen by Citi Depleted Faster Than Expected on Ban

- Natural Gas Supply Gains Keep Driving Bulls From Market: Energy

- Gold Drops as Advance to Four-Month High Spurs Investors to Sell

- Whiting’s $3.8 Billion Kodiak Deal Crowns New Bakken Shale King

- Iron Ore Seen Rangebound This Half Before 2015 Slump, Citi Says

- Corn Extends Drop to 4-Year Low as Global Supplies Seen Climbing

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

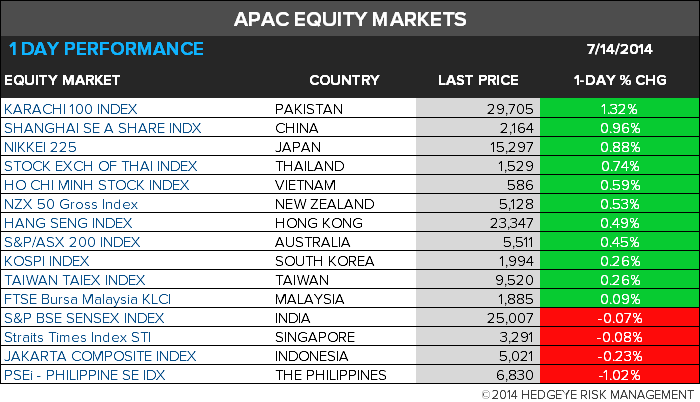

ASIAN MARKETS

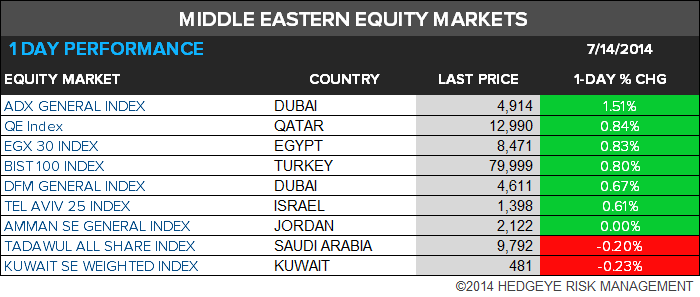

MIDDLE EAST

The Hedgeye Macro Team