Positive Thinking

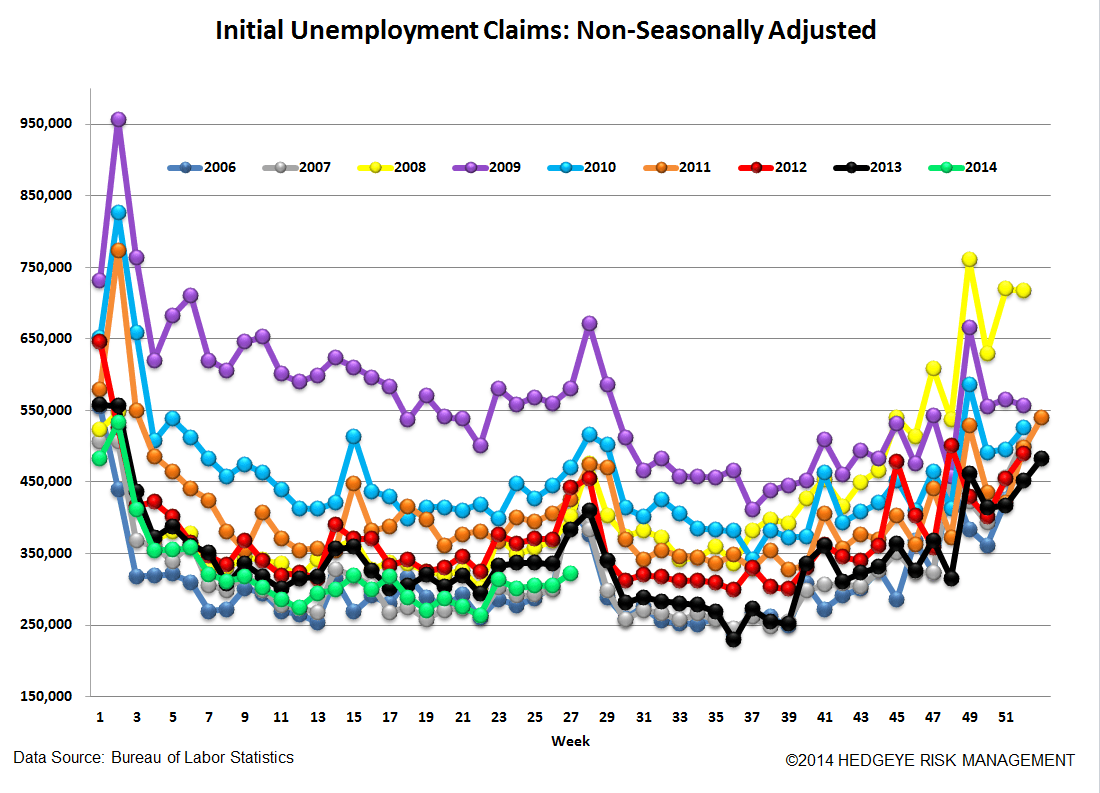

While most of us were barbecuing and reciting the Declaration of Independence last week, something else positive happened as well. Fewer people filed for initial unemployment insurance benefits.

There's been a steady stream of positive newsflow on the labor market front of late. Recent numbers from ADP, NFP, JOLTs and claims have all been pointing in the same direction. Claims numbers this morning suggest the rate of improvement may be accelerating still. The year-over-year improvement in NSA jobless claims surged to 16% in the latest week, up from 9% improvement in the previous week. Meanwhile, the 4-wk rolling average of NSA claims improved to 11% from 9%. One caveat is that the July 4th holiday last week may have created some distortion in the number. We'll see what next week brings.

The Data

Initial jobless claims fell 11k to 304k from 315k WoW. The prior week's number was unrevised.

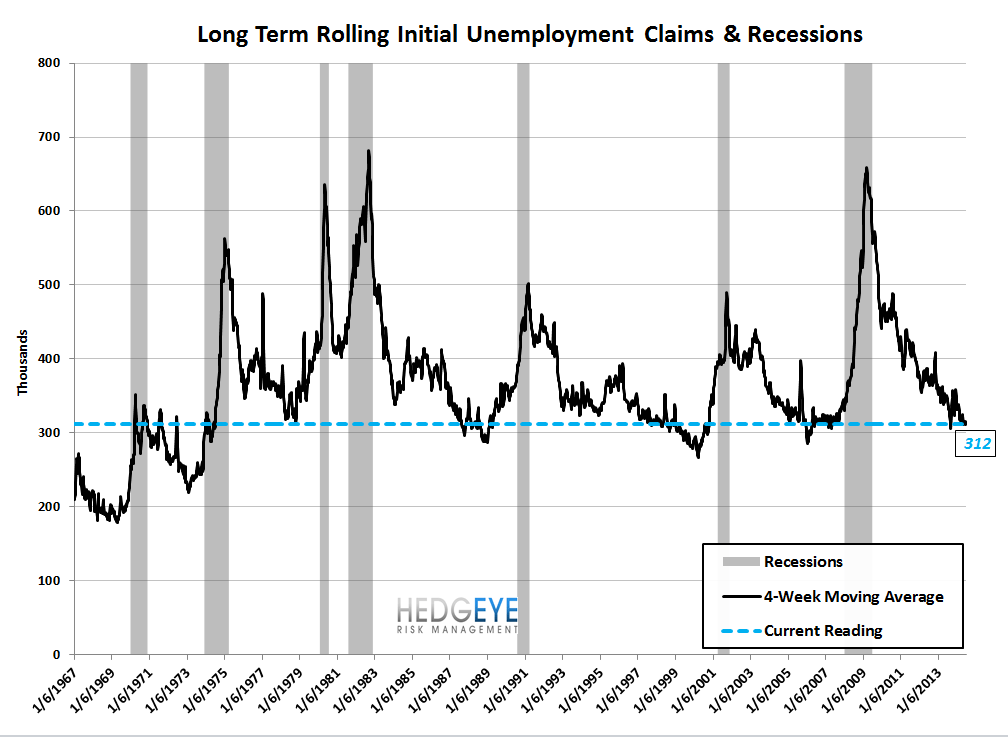

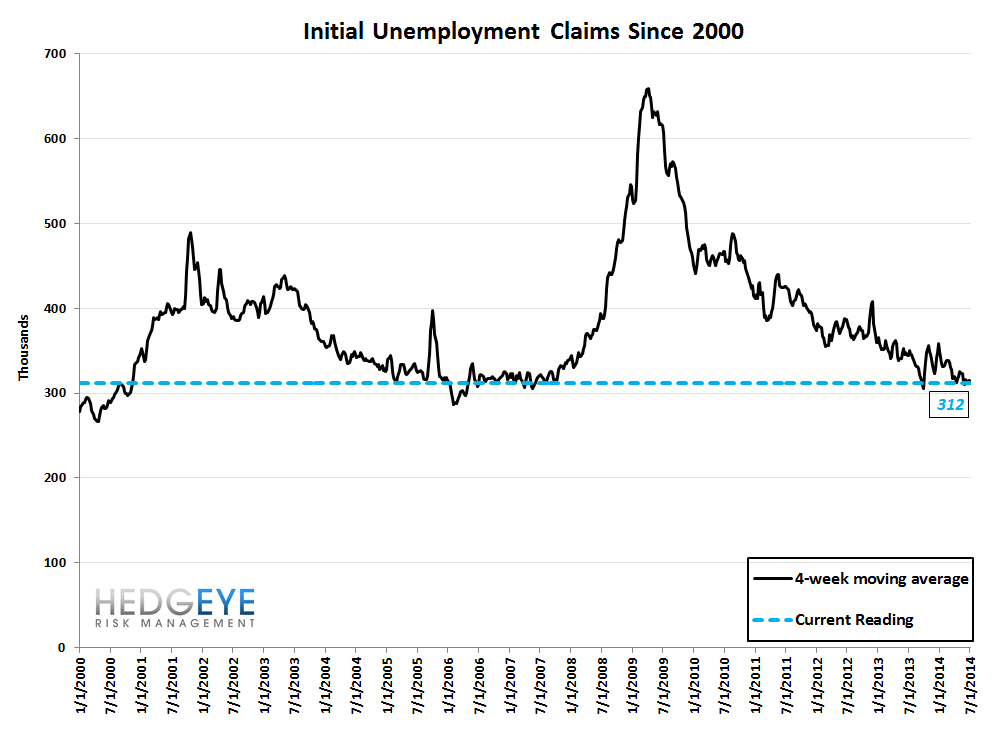

The headline (unrevised) number shows claims were lower by 11k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -3.5k WoW to 311.5k.

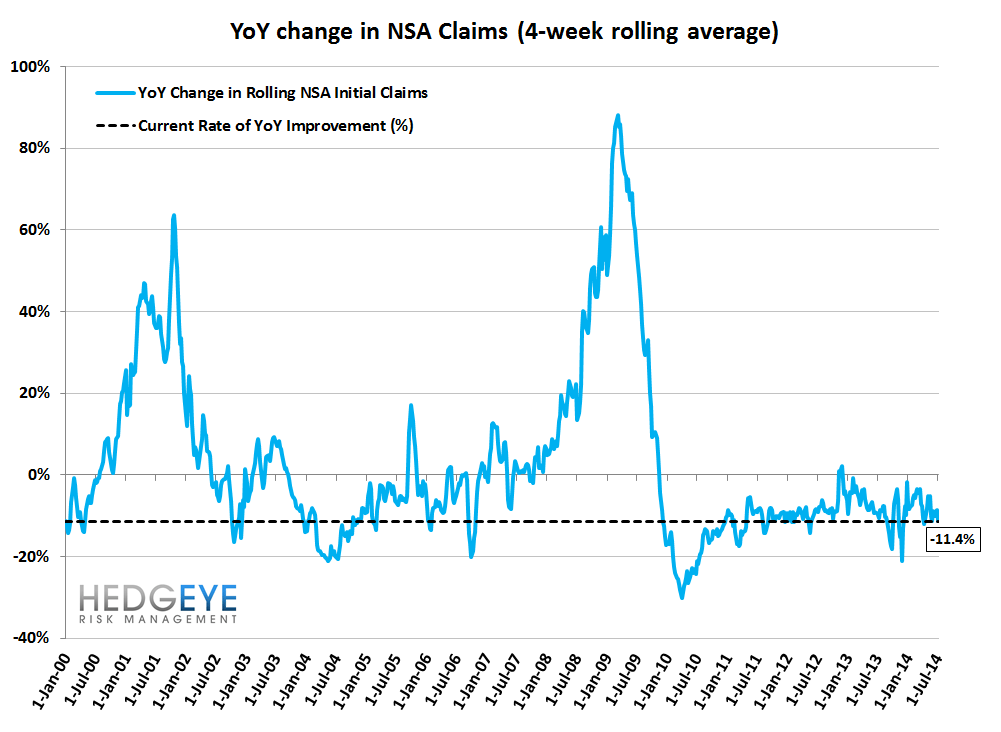

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -11.4% lower YoY, which is a sequential improvement versus the previous week's YoY change of -8.7%

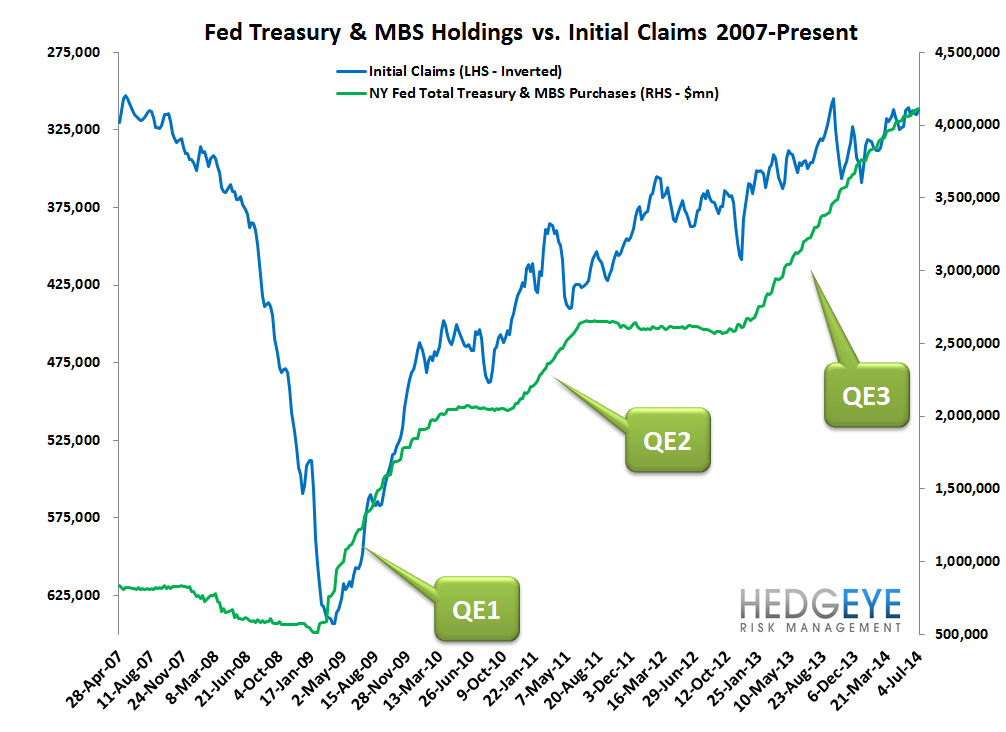

<chart13>

<chart14>

Yield Spreads

The 2-10 spread fell -3 basis points WoW to 207 bps. 3Q14TD, the 2-10 spread is averaging 210 bps, which is lower by -11 bps relative to 2Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT